William Mills Agency and Beyond the Arc will be live blogging at FinovateSpring. Check back for new updates throughout the day.

William Mills III, Chief Executive Officer of William Mills Agency is live blogging today at Finovate Fall 2016. He has more than 30 years of experience in financial technology and is a recognized leader in financial and technology marketing. He has personally advised more than 300 chief executives on marketing strategy, business development, mergers and acquisitions, company branding and public relations. You can contact him via email at william@williammills.com or on Twitter @williamemills .

William Mills III, Chief Executive Officer of William Mills Agency is live blogging today at Finovate Fall 2016. He has more than 30 years of experience in financial technology and is a recognized leader in financial and technology marketing. He has personally advised more than 300 chief executives on marketing strategy, business development, mergers and acquisitions, company branding and public relations. You can contact him via email at william@williammills.com or on Twitter @williamemills .

Steven J. Ramirez is CEO of Beyond the Arc, Inc. The company helps clients to strengthen customer experience and to deploy data science and Big Data analytics to make marketing and operations more effective. Their social media data mining helps clients improve customer experience across products, channels and touchpoints. For more information about Beyond the Arc visit beyondthearc.com, call 1-877-676-3743, or email web@beyondthearc.net. Insights on social media, financial services and more are shared on their blog, or follow them on Twitter at @beyondthearc or on Google+.

Best Practices for Marketing to Banks

04:19 pm

BREAK – Still need to shoot, edit and publish more video updates (thank you KT).

========================================================

VIDEO RECAPS FOR TODAY can be found at: http://hubs.ly/y0NFT90

Please check back for our live blogs as well as the video updates. Feel free to share today’s live blog summary hosted by myself a with Steven Ramirez.

Day one: https://www.williammills.com/blog/finovate1/

Day two: https://www.williammills.com/blog/finovate2/

Or feel to call my direct/mobile: 678-694-7213

William Mills, CEO

William Mills Agency

www.williammills.com

04:13 pm

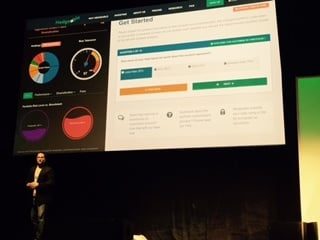

Hedgeable

Twin brothers leading tech company. Reminds you of the movie “The Social Network”, right?

Twin brothers leading tech company. Reminds you of the movie “The Social Network”, right?

From the web: Hedgeable automates sophisticated, low cost, risk managed investing for busy professionals with as little as 00 in 5 minutes. I think they could make investing “sexy” for millennials as a global investing firm. Minimum investment is ,000.

New York-based company with a really great dashboard. Back in the old days of Finovate dashboards like Hedgeable never looked this good.

From www.observer.com:

Hedgeable, an online investment management service, has declared it will be “the only platform that will charge nothing for companies to list, nothing for buyers to buy, and will make no money on transactions, regardless of how SEC defines the role of similar platforms, beginning in 2013.” Count chickens much?

Full story here: http://observer.com/2012/06/as-equity-crowdfunding-nears-platforms-race-to-be-the-first/

Matthew and Mike Kane @Hedgeable https://www.hedgeable.com/

^WM william@williammills.com

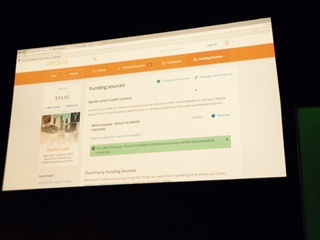

The company focuses on digital investment, with appropriate risk management. The wealth management firm of the past is being reinvented online. The digital firm creates tailored portfolios for customers. Coinbase and CircleUp are other fintech partners. No 3rd-party funds or managers are used. Minimum investment is k, and accounts are opened online. This robo-advisor allows people to invest in bitcoin. They are working with financial advisors and broker-dealers as partners. ^SR

04:06 pm

Dwolla

Talking about a new protocol – FiSync – to cut ACH transactions. As was noted at Money2020 several years ago ACH is a bit “Long in the tooth” and that quote was from the folks at NACHA.

Talking about a new protocol – FiSync – to cut ACH transactions. As was noted at Money2020 several years ago ACH is a bit “Long in the tooth” and that quote was from the folks at NACHA.

You might want to check out the specific FiSync page on Dwolla’s site: https://www.dwolla.com/fisync

It seems to be pretty cool and important but not as exciting as other presentations. It’s hard to make ACH exciting and you guys did a good job.

Jordan Lampe and Ben Milne @dwolla https://www.dwolla.com/

^WM william@williammills.com

Dwolla is one of the companies leading innovation in the payments space. Today’s presentation is about secure authentication. The payment information stays with the bank, unlike ApplePay. One of the primary benefits is real-time transfer of funds. ^SR

03:58 pm

SayPay

Launching today; a simple way to authenticate and get things done through a white label bank app – bill pay, etc. It looks like mobile banking, bill pay, and other stuff COMBINED with authentication. I don’t think I’ve seen something like this. Looks like voice authentication. I met an Israel-based firm that had something like this (but not as developed) several years ago at BAI Retail Delivery Systems Conference. These folks are based close by; Pleasanton, California, a beautiful community that my wife and I visited earlier this week.

Launching today; a simple way to authenticate and get things done through a white label bank app – bill pay, etc. It looks like mobile banking, bill pay, and other stuff COMBINED with authentication. I don’t think I’ve seen something like this. Looks like voice authentication. I met an Israel-based firm that had something like this (but not as developed) several years ago at BAI Retail Delivery Systems Conference. These folks are based close by; Pleasanton, California, a beautiful community that my wife and I visited earlier this week.

Boy, I’d really appreciate any FI provider to authenticate me by speaking easily. It takes me about 5 minutes to get my AMEX travel agent on the phone with the buttons on the phone tree and more.

Steve Hoffman and Julia Webb @saypaytech http://saypaytechnologies.com/

^WM william@williammills.com

Are customer experience and online security at odds? SayPay wants to make security more seamless for consumers. On the payment front, bills are pushed out to users via an alert. Voice biometrics are a key part of the solution, with a “3-D model” of the user’s voice. The company seems to be in early stage, actively raising funds. ^SR

03:51 pm

I THINK there are three more presentations for today. Don’t forget about tomorrow.

03:50 pm

Digital Insight, an NCR company

“What’s the common thread between three events that units the events? All are using Beacons for their customers. This is a trend here, I think Finovate is putting similar companies together (see earlier posting). I’ve followed DI since Paul Fiore started it back in the 1990’s, then public, then to Intuit,then LBO now with NCR (now and Atlanta-based company). I’m very interested in seeing what they have been under NCR’s leadership. Interesting UI but I can’t tell who is supposed to use this (tellers?) and on what kind of hardware (iPads?). A CU is testing it now. DI’s DNA is in the CU space but has a strong footprint in the bank space. I THINK they are going to show an “offers” app with Bluetooth beacon technology at a business.

“What’s the common thread between three events that units the events? All are using Beacons for their customers. This is a trend here, I think Finovate is putting similar companies together (see earlier posting). I’ve followed DI since Paul Fiore started it back in the 1990’s, then public, then to Intuit,then LBO now with NCR (now and Atlanta-based company). I’m very interested in seeing what they have been under NCR’s leadership. Interesting UI but I can’t tell who is supposed to use this (tellers?) and on what kind of hardware (iPads?). A CU is testing it now. DI’s DNA is in the CU space but has a strong footprint in the bank space. I THINK they are going to show an “offers” app with Bluetooth beacon technology at a business.

Marshall Yuan and Ronald Leung @Digital_Insight http://www.digitalinsight.com/news.html

^WM william@williammills.com

Location-based offerings for customers are enabled by beacons. Digital Insights has a platform for managing these beacons. Banks can customize the in-branch customer experience. No doubt that this technology will one day take the world by storm. Not sure if that day is anytime soon, at least not for banks. ^SR

03:42 pm

Someone With Group (Some1WithGroup)

Ok, they have my attention with the words “medical only crowdfunding”. Man, this is a big deal. If you can help the healthcare industry you can do anything. Fraud is a problem in medical. Vetted for hospital systems. License their program to hospitals, perhaps others. HIPPA compliant with several patents pending. B2B play. Keep an eye on this company. Based in Maryland.

Ok, they have my attention with the words “medical only crowdfunding”. Man, this is a big deal. If you can help the healthcare industry you can do anything. Fraud is a problem in medical. Vetted for hospital systems. License their program to hospitals, perhaps others. HIPPA compliant with several patents pending. B2B play. Keep an eye on this company. Based in Maryland.

Paula Jagemann-Bane and Matt Pomrink @Some1WithGroup http://www.someonewithgroup.com/

^WM william@williammills.com

This is a very interesting product that enables crowdfunding for medical/HIPAA needs. The platform is licensed to medical providers. Consumers have to opt-out of HIPAA to set-up a funding page. The offering helps to reduce fraud for this type of crowd-funded campaign. The contribution is made on the hospital’s website. “We are ready for revenue”, the product is ready to be sold to hospitals across the country. ^SR

03:35 pm

Kabbage

Kabbage

Atlanta-based Kabbage has a great reputation. They presented at Finovate NYC last Fall and perhaps earlier. Last Fall they launched their “Carrot” product. Showing tablet-based solution with their partner Sage (software?). Showing Kabbage “Card” with MasterCard which I have not seen before.

Jason Dell and Michelle Sirpak @KabbageInc https://www.kabbage.com/

^WM william@williammills.com

Kabbage has been providing capital to small business for last few years. Last fall, they rolled out personal lending for consumers. Today, they are announcing “powered by Kabbage” with first customer Sage Software.

According to Finovate: @KabbageInc has 170 employees and has raised 6M in equity #Finovate.

The other announcement today is for the Kabbage Card, issued as a MasterCard debit card. At point of sale, the transaction reduces the available credit on the customer’s Kabbage business line of credit. ^SR

03:28 pm

Whodini

Whodini

Show mobile app(?) that shows customer data instantly as the customer walks up. Interesting. I haven’t seen anything like this. I don’t know any FI’s that do a great job at this (I’m sorry). NOW I GET IT. It’s a Bluetooth-based beacon coupled with an app which has an incentive for the customer to download the app. Very good idea. Full disclosure, I serve on the advisory board for Sionic Mobile so I could see how Whodini could partner with Sionic and all types of companies. Five minute setup and POS system agnostic. They are open to Angel and VC investments.

Brian Lawe and David Schachne http://www.whodini.net/ ^WM william@williammills.com

The company provides a CRM offering to help you create very robust customer profiles. Banks can solicit, and act on, customer preferences. Gamification provides an incentive for customers to answer questions about themselves, making the profile more extensive. The app includes social media, so users can become brand advocates. The product is both for the bank, and the bank’s merchant customers. ^SR

03:22 pm

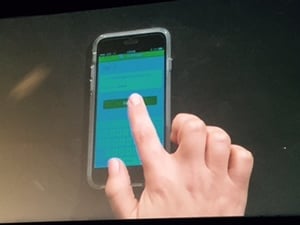

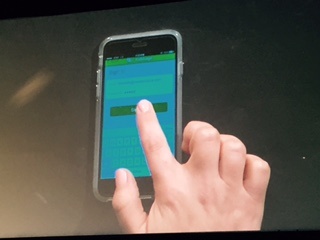

StockViews

London-based StockViews seems to be a crowd-sourcing platforms so people know how well their stock analysts are, or how how successful their planner is doing. I seem to think I’ve seen something like this at Finovate NYC. It looks good but I need to understand how they are better than alternatives. Launching today the STOCKVIEWS SIGNAL: showing ratings in the group on IBM (and their stock).

London-based StockViews seems to be a crowd-sourcing platforms so people know how well their stock analysts are, or how how successful their planner is doing. I seem to think I’ve seen something like this at Finovate NYC. It looks good but I need to understand how they are better than alternatives. Launching today the STOCKVIEWS SIGNAL: showing ratings in the group on IBM (and their stock).

From their web site: Search for stocks that interest you

As investors ourselves, we believe that debate should be focused around individual stocks. Search for stocks that interest you to find relevant opinions and research. There are thousands of discussions to explore that are going on right now. – See more at: http://www.stockviews.com/howitworks#sthash.1eeWq0h9.dpuf

Tom Beevers and Tara Hyland @StockViewsNews http://www.stockviews.com/ ^WM william@williammills.com

Fund managers need research, and StockViews sees an opportunity to disrupt this space. There are thousands of analysts, how does a fund manager know which ones to follow? This is the question the company addresses. They collect information about the analysts and the stock research they create. The platform helps to democratize research, introducing new analysts to fund managers. ^SR

03:12 pm

Currency Cloud

Currency Cloud

From their site: Powering Global Payments

Develop and automate your product with our Payment Engine to benefit from real time wholesale rates and a fast, secure payment network. Tailor to your business using our next generation API.

Based in London, these folks do a TON of payment processing. 125 platform customers in 212 countries and deliver 95% of the payments in 24 hours. “We are an API company.” Showing browser-based solution on a MacBook. I’m a bit annoyed that I don’t know these folks as they are clearly a “Player” in our industry. Showing the ability to build an API live on stage at Finovate.

From their web site: Currency Cloud is excited to announce that we have passed a significant milestone! We have now processed billion, sending money to every corner of the earth; from Botswana to Brazil.

Todd is doing a great job; eloquent speaker easily explaining very complicated technology processes. Todd Latham and Rachel Nienaber @currency_cloud https://www.currencycloud.com/

^WM william@williammills.com

This offering allows companies to easily make international payments, sending cash around the world. Customers are banks, payment providers, and companies needing an international payment platform. The company provides an API to developers. ^SR

03:05 pm

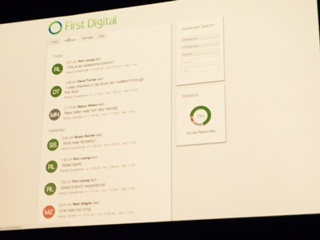

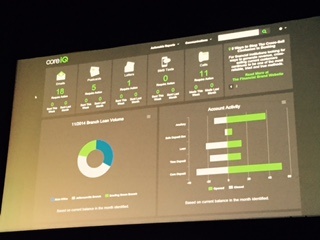

Onovative

Onovative

CoreIQ looks to be a really cool community FI dashboard for marketing and other services. I have GOT to research this company. Not many folks are tackling this issue for community banks and credit unions. The core vendors have some good products but this looks like a good “out of the box” view of the data.From their web site: SIMPLY POWERFUL

MARKETING FOR BANKS AND CREDIT UNIONS Emails, SMS Texts, Letters, Postcards, and Call Reminders sent automatically from your core banking system. Customer Onboarding and cross-selling have never been so simple.

I’m interested in finding out their “back story” – how they got into this business and who they are serving now. Good job.

Michael Browning and Clay Turner @Onovative http://www.onovativebanking.com/

^WM william@williammills.com

CoreIQ provides an easy-to-use marketing automation platform for community banks and small institutions. For any email campaign, you can also use the content to send the communication a a direct mail letter. The platform keeps your data on-premise, to send tailored outbound marketing. ^SR

02:22 pm

Morning Video Recap

William Mills, CEO of William Mills Agency and Steven Ramirez, CEO of Beyond the Arc discuss Finovate’s morning recap highlighting Stratos and Yodlee.

02:15 pm

Short break, back for final series of demos for the day and another video recap. Stay tuned…..

02:15 pm

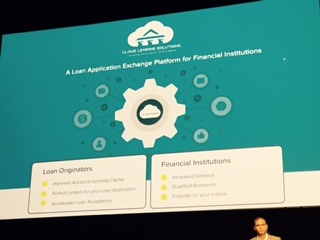

Cloud Lending Solutions

Cloud Lending Solutions

A Loan Application Exchange Platform for financial Institutions. Speaking about the “fall out” of loan applications. “Mismatch of borrower needs and products lenders offer. This is an online platform that enables the sharing of products and criteria with other lenders.”

Snehal Fulzele @cloudlending http://cloudlendinginc.com/

^WM william@williammills.com

The company provides a virtual meeting place for applicants and lenders. Both parties set their preferences. This is not just about leads, applicants can submit an application online and it is matched with the lender. What happens when the application matches more than 1 lender? The lenders can bid for the application (they bid based on interest rate that they offer to the borrower). They are currently in private beta. ^SR

02:07 pm

WealthForge

WealthForge

THE PROCESS OF RAISING PRIVATE CAPITAL DOESNT HAVE TO BE COMPLICATED. Can’t agree you more on that. Private placements are a pain and I think they have found a better way. Based in Virginia. I THINK it’s white labeled to the organization that is raising the money. Showing an example of “ABC Company” – web-based but offer API for real time information. I like it.

Arthur Weissman and Matt Dellorso @WealthForge http://www.wealthforge.com/

^WM william@williammills.com

The company simplifies the process of raising capital for Reg D investments, the typical structure for most startups. Allows the issuer to add an “Invest” button to its website. The system is compliant, and audited annually, according to WealthForge. The platform enforces compliance requirements, including a review of suitability for qualified private investors.

Note to presenters: speaking really fast is not the way to “streamline” your demo. If you have to speak that fast, you’re providing too much content for your 7 minutes on stage. ^SR

01:59 pm

Dealstruck

Dealstruck

Easy access to money for SMB’s. Showing example of dark chocolate retailer. This sounds like a Capital Access Network, OnDeck, perhaps Kabbage or Business Financial Services. With new compliance regulations for banks I see this as a HUGE growth sector. Here is a paragraph referencing Dealstruck from the New York Times:

Then he heard about Dealstruck, a year-old company based in San Diego. In October 2013, Mr. Rincon shared his financials with Dealstruck, and a few days later, he came away with a 0,000 loan that featured a three-year term, a 10 percent annual interest rate, and flexible terms that allow him to make bigger payments in busy months. “The terms are clear and include a set monthly fee and a reasonable payback time frame,” Mr. Rincon said.

Full NY TIMES story: http://www.nytimes.com/2014/03/06/business/smallbusiness/cant-get-a-bank-loan-the-alternatives-are-expanding.html?_r=0

Ethan Senturia and Russell McLoughlin @dealstruck https://www.dealstruck.com/

^WM

william@williammills.com

One of the biggest issues for small business is managing cash flow, and access to working capital. This offering provides an end-to-end solution that encompasses borrowing, managing accounts receivable, and vendor invoices and payments. The platform integrates with Quickbooks, and the company’s bank accounts. Small businesses can also obtain credit reports on B2B customers. ^SR

01:51 pm

Trulioo

Trulioo

“Like Uber (which owns no cars) , we are the largest consumer data company in the world without owning any data.” Showing example of verification process for sending money to China. Trulioo is based in Vancouver, Canada and I understand there is a huge population in Vancouver that formerly resided in Hong Kong, Taiwan or China so this example makes sense.

From their web site: Trulioo is a leading global ID verification company providing advanced analytics based on traditional information such as public records, credit files and government data as well as alternative sources including social login providers, ad networks, mobile applications, e-commerce websites and social networks. Trulioo specializes in scoring online identities as authentic, machine generated or fraudulent with our identity bureau covering 3 billion people in over 40 countries, including coverage for the most challenging demographics from emerging markets such as China, Russia, and Brazil.

Stephen Ufford @trulioo https://www.trulioo.com/

^WM william@williammills.com

The company is pronounced “truly you” and they are a consumer data company. They match consumer data from over 140 sources, but they don’t own the data. The company seems to have a really diversified business model, they are not reliant on just one use case. A bank can use them any time they want to validate prospects or customers. ^SR

01:46 pm

Finicity

Launched last year at other Finovate eventFinDev. Showing on a mobile device but I believe this is an API aggregation play. From their web site: Build Powerful Financial Apps with a Rock Solid API

14 Years Agg Experience

16,000+ Developed Data Sources

2 Billion+ Aggregations

70 Billion+ Transactions Aggregated

“We are in Alpha with a new product/API.” Showing VENMO integration. I didn’t realize this company was started in 1999. I’m sure I’ve seen them before; not sure where, perhaps at Finovate. While their HQ is in Utah they have Coaching and Scheduling Center (training) offices in Buford, Georgia (REALLY).

Nick Thomas and Steve Smith @finicity https://www.finicity.com/ william@williammills.com

^WM

They provide an account aggregation API with services for consumer lending and personal financial management. ^SR

01:45 pm

INETCO Systems

Another fake ATM in a box but at least it has humor with Dallas as a walking faux ATM. VirtualBox ATM. Shift is HOW people use the financial devices using data. Seven patents on bringing in data in “the box”. Interesting, I need to stop by their stand and learn more.

Marc Borbas and Dallas Pretty @INETCOInsight https://www.inetco.com/

^WM William Mills

The platform provides management tools for ATM networks. The dashboard helps with transaction volumes, customer analytics, geo-location and more. The technology helps banks to use data to make their ATM channel better for customers. The challenge is that the dashboards are cluttered and not intuitive, doesn’t hit the mark from a UI perspective. ^SR

01:39 pm

Avoka

Avoka

HTML5 solution NOT an app. I’ve been a big fan of HTML5 for a long time and am glad more folks are embracing it. Mobile apps are great and preferred by many folks but there IS an advantage to have full function on any device, whether it’s on Apple, Android, Microsoft, Linux and more. I think their web site says it well:

Vision: Frictionless Digital Business

Mission: Create Frictionless Experiences for all Digital Transactions

Avoka has created a digital sales enablement platform to create frictionless sales & service transactions. We solve the “buy” problem for Banks, Insurers, Health Care, Education, Government and many other industries – where the traditional “shopping cart” eCommerce is not a good fit.

Solutions include account opening, applying for a credit card or loan, submitting an insurance claim or enrolling for a government product or service.

Partner with Top Image Systems. Link to press release on their announcement today:

http://www.avoka.com/credit-card-application-speed-record-at-finovatespring

Derek Corcoran and Jeff Kalicki @avokatech

http://www.avoka.com/

william@williammills.com

^WM

Can your bank open a new account in 90 seconds or less? Maybe with Avoka, now you can. Their goal is to make account opening easy and frictionless. Uses social media, scan of docs, to make entering data easy and pre-populated. Partners with Yodlee to grab data from existing accounts. Banks can create customer experiences with drag-and-drop functionality. ^SR

01:25 pm

Dynamics

Dynamics

I’ve known this company for many years and Jeff is a visionary in the card industry. He won at least one, if not several, “Best in Show” at Finovate and other events. You know the company is on to something when MasterCard (with others) invests million in Dynamics last December in Series C funding.

They have raised at least one-hundred and ten million in VC so far.

Now Jeff is showing a new card for online purchases. With EMV requirements hitting the U.S. I can see the interest in what they are doing. Keep an eye on these folks.

Jeff Mullen and Pete Kaulbach https://www.dynamicsinc.com/

william@williammills.com

^WM

The company is partnering with MasterCard to offer time-based security features for payments. Card security is a critical issue for this industry. The demo is a little too jargon-prone. Would like to hear the benefits conveyed in plain English (BTA can help them with that!) This is one I’ll need to do some follow-up research on. ^SR

01:18 pm

TrueAccord

Fully automated debt recovery for businesses of all sizes. This looks like a new type of the collection process for all parties. Very nice browser-based dashboard. I’m seeing continuous improvement in the customer experience and UI’s. “TrueAccord is a seamless, automated platform through which businesses can boost recovery rates and preserve client relationships by empowering those in debt to easily and responsibly address their obligations.”

Named a Top 10 companies to watch by AMERICAN BANKER but I’m not sure which year. Perhaps 2013. From TECHCRUNCH: TrueAccord Looks To Fix Debt Collection With Million From Khosla Ventures, Max Levchin And More

http://techcrunch.com/2014/09/16/trueaccord-looks-to-fix-debt-collection-with-5-million-from-khosla-ventures-max-levchin-and-more/

“Ohad Samet and Nadav Samet” @trueaccord https://www.trueaccord.com/

william@williammills.com

^WM

The technology is aimed at improving debt collection for institutions. This is a high-risk area for the CFPB. I’ll be interested to see if they address the compliance issues.

The system allows use to upload files, or use the data API. The product helps you to manage collections on a customer level. Payment plans, discounts, and collection policies can be included as global settings. Uses machine learning for automated processes. Company states increase in collections up to 20% ^SR

01:12 pm

SmartAsset

Showing browser-based solution on a Windows PC with Chrome. “Home Buying, refinance, Retirement, Life Insurance and more.”

“We drive 5 to 10 times the user engagement than others through our white label solution with your FI.”

Michael Carvin @smartasset https://smartasset.com/

^WM William Mills

The company provides information to help people make better retirement decisions. They note that even financial advisors like the tools, using them with their own clients. All of the tools can be used by an FI, white labeled to be integrated into the firm’s website. This is one of the better examples of robo-advisor technology. ^SR

12:12 pm

Lunch break – now it gets REALLY busy. Steven and I are shooting video updates each day. Check back often and if you are here at Finovate please stop by the front row when you can.

Congratulations to the entire Finovate team on another great event. This is going very well everything is running great. Keep up the great work!

William Mills, CEO

William Mills Agency

william@williammills.com

@williamemills

william@williammills.com

678-694-7213

12:05 pm

DoubleNet Pay

DoubleNet Pay

“Consumers are living paycheck to paycheck. Innovation to financial management.” Showing cool Apple app. “People are overloaded with info for budgeting and savings; integrate with payroll processors and bill pay companies to automate the process for consumers. We reorient how consumers think of how the payment process works.”

I THINK I’ve seen these folks before if now I’ve met or seen them over the past year. “Most financial apps are too complicated. We are trying to keep it as simple as Uber.” Their relationship with ADP I think is the “secret sauce” to their success. EVERYONE is in the PFM space but if DoubleNet Pay can automate the whole thing for consumers, on their smart phones, this could be big.

Brian Cosgray and Cody Laird https://www.doublenetpay.com/

^WM William Mills

Partners with ADP to make it easier for underserved consumers improve their cashflow. It helps consumers to organize their bills and pay them. The app enables people to save for certain financial goals. App looks very easy to use. I’m not entirely sure of their differentiators. ^SR

11:55 am

Prairie Cloudware

Prairie Cloudware

Full disclosure: William Mills Agency is the public relations agency for Prairie Cloudware.

Showing a new solution, white label to the financial institution with complete security. Showing an Internet banking demo where the customer is adding a payment option (i.e. VISA card) and verified with a customer’s mobile phone for a digital wallet, now adding a personal computer a verified payment source. If a device/account is compromised the bank customer can deactivate the device/card/account in question. Now showing using on a retail site – Crate&Barrel. Simple and secure with tokenization. Can create custom offers from the bank using the technology.

Doug Parr and Mike Carter” @PrairieClouds http://www.prairiecloudware.com/

^WM William Mills

Digital Payment Guardian (DPG) is a secure way for consumers to make payments. The bank can offer this on their platform, and get “top of wallet” status in the virtual wallet. The product provides centralized access and storage of payment options, essentially a “universal wallet” enabling tokenized payment transactions. Information from your wallet pre-populates web forms on e-commerce sites. ^SR

11:43 am

SizeUp

SizeUp

“We enable your FI to be a source of solutions for your customers.” Showing web-based platform for SMB through their bank (I assume white label). Showing data integration of SMB data with other data (from bank and other sources) showing a dashboard of the SMB business health. Interesting demo. I don’t recall a SMB platform/solution that had this specific benefit.

From their web site: Business Intelligence for All. In 3 steps you will learn how your business stacks up to your competition.

This is not a knock on this company or other presentations but I swear I think many of these companies use the same WordPress templates for their web site. It looks VERY nice, clean, probably mobile ready; many of these sites look similar. Very good demo.

Anatalio Ubalde and Thomas Barron @SizeUpBusiness https://www.sizeup.com/

^WM William Mills

The company provides competitive intelligence for small businesses. The demo is using the live tool from the Wells Fargo website. As both a small business owner, I’m extremely interested in this offering. Each bank can have a custom version on their site. The tool helps small businesses make better decisions with data. Big Data meets small business with SizeUp. ^SR

11:37 am

Yodlee

Yodlee

I’ve known Yodlee since the “Dot Com Days” when S1 had an ownership stake. They are a survivor and has continued to grow and went public last year (I believe it was last year). I wonder if they have lost folks since the six month lock up period. They really have the data that drives so many financial tech applications. Launching Yodlee “Sense” sounds like a PFM but let’s see what’s unqiue. Showing on IOS device. Personalizes your financial decisions based on data. Looks cool, sounds a little bit like LendingTree’s presentation.

Katy Gibson, John Bird and David Lee @Yodlee http://www.yodlee.com/

^WM William Mills

The Yodlee team announces the premiere of Yodlee Sense. This is a great tool with proactive account management. The demo shows a glimpse of the consumer’s future: advance warning of a low balance, before it happens. This would be an excellent way to avoid overdraft fees. The app also has tips and challenges to motivate consumers to use it to manage their financial needs. Yodlee Sense is an alternative to the traditional budget tool, with predictive features and a high degree of personalization. Yodlee gets personal and predictive. Very interesting to see this consumer-facing offering from Yodlee, seems to indicate a new expansion of their business. ^SR

11:35 am

LendingTree

LendingTree

“You know us from the mortgage space but what could we offer that would predict what someone would need before they did?” Offering free score for life at their site. Using credit and purchase data to help consumers find ways to save money via mortgage, auto loan, credit card and more. “Our software will find the best deal for consumers.”

Nikul Patel and Gabe Dalporto @LendingTree https://www.lendingtree.com/

^WM William

The company is “a 16-year old start-up“ in the consumer lending space, serving millions of customers. The latest offering provides credit score to consumer, interprets the report, and then serves up customized credit promotions. Gives you advice and recommendations, like “time to refinance your mortgage and save 0”, and this is provided in real time. The products now include all lending products from mortgage, credit card, student loan, and more. Sit back, and let software shop on your behalf 24/7. ^SR

11:31 am

Karmic Labs

Karmic Labs

Showing “dash” mobile able – BizNOW. I have to admit we are having some tech issues so I’m going to have to visit their stand and get a better understanding on what they are doing.

Ryan Weidenmiller, Chris Agerton and Troy Land https://karmiclabs.com/

^WM William Mills

This company is trying to make it easier to issue a payment card for small businesses, or employees in a larger company, that don’t otherwise qualify for a corporate credit card. Petty cash is a thing of the past with this offering, and it works both on desktop and via mobile app. ^SR

11:25 am

INETCO Systems

Another fake ATM in a box but at least it has humor with Dallas as a walking faux ATM. VirtualBox ATM. Shift is HOW people use the financial devices using data. Seven patents on bringing in data in “the box”. Interesting, I need to stop by their stand and learn more.

Marc Borbas and Dallas Pretty @INETCOInsight https://www.inetco.com/

^WM William Mills

11:15 am

Stratos

Stratos

VC company with million raised to-date. Showing a Stratos card – “think of it like a wearable device” (but looks like a credit card and has a mag stripe). Very interesting card and mobile combination; kind of turn on card for a specific activity. I THINK it connects to mobile phone via bluetooth.

I’m a big TILE bluetooth user (I have five of them) because I’m always using stuff. If possible I’d like to get one of their cards to test. They are coming out with an EMV version which I am sure will be needed. Now showing B2B version.

Thiago Olson and Henry Balanon @StratosCard https://stratoscard.com/

^WM William Mills

The team is presenting the Stratos Connected Card at Finovate. According to the company, this transforms your credit card into a wearable device. I’m impressed by the technology, and this is one of the few fintech companies that are really building an effective consumer brand.

They are now rolling out a new platform for digital issuance of credit cards– get rid of the plastic! Stratos is also providing this service on a “white label” basis for banks and other issuers. When an issuer offers Stratos, their card is placed top-of-wallet as the default. ^SR

11:05 am

Ondot Systems

Ondot Systems

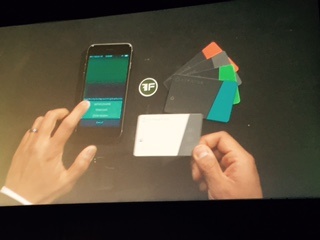

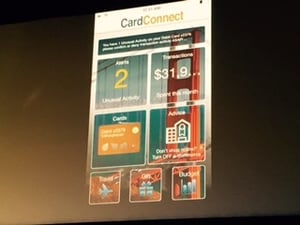

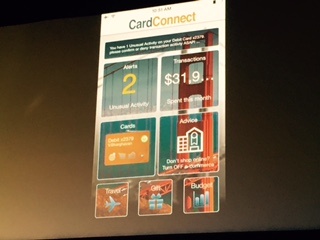

“Over 100 million cards have be hacked due to data breaches. It’s getting harder to outwit the bad guys.” San Jose, CA-based. CarConnect is a white-label platform for card security and engagement. “130 FI’s are now using our application.” Last year launched CardControl for consumers to control payment controls from their mobile apps.

Second phase of implementation is CardConnect. I’m trying to figure what is different from this new app from their current app. It appears to have alerts, transaction preferences and more. Showing mobile app that with fraudulent transactions. These folks look well-backed financially. From Inc.: Ondot Skips VCs in Favor of Million Angel Round – Ondot, a financial technology startup, tries to get to breakeven using only angel money.

From their web site: Ondot’s white label solutions enable Financial Institutions to give consumers the security they want with the convenience they need. Ondot serves its customers via direct relationships as well as channel partnerships with several of the largest card processors in the United States, who serve over 10,000 Financial Institutions.

http://www.inc.com/kimberly-weisul/startup-skips-vcs-in-favor-of-eighteen-million-angel-round.html

Vaduvur Bharghavan @ondotsys http://www.ondotsystems.com/

^WM William Mills

11:03 am

TickerTags

TickerTags

TickerTag Body Camera? – I’m not sure what these folks do but it looks totally different than other demos. It looks like some kind of Twitter analytics to monitor trends. Showing chatter in the Twitter stream. I’m guessing they are going to show how their tech can predict either stock changes based on social media. “These social media data points have never been available to the financial industry.” I’m going to have to defer to my friend Steven on this one; he’s a pro on this issue. Launching platform in about three weeks. Public company tags of ticker symbols are locked and loaded with social data. This could be BIG. Platform is free so how do they make money?

Closed beta but for the next few hours you can sign up.

Chris Camillo and Jordan McLain” @tickertags http://www.tickertags.com/

^WM William Mills

Twitter activity and news: can social chatter make you a more effective investor? There is a new generation of “social data points” that the financial industry has never been able to analyze and use for trading. They use natural language processing, machine learning, and human tagging. This company is doing some great work in text analytics, I’m interested in learning more! ^SR

10:13 am

Folks, it’s time for a short break. I hope you will return soon. If you would like to visit you will find me on the front-row here at Finovate on the right side.

William Mills, CEO

William Mills Agency

william@williammills.com

10:09 am

Mitek

Mitek

“3,500 banks and 50 million consumers use Mitek applications.” Showing new product, PhotoFill to pre-fill application and Photo Vertify to Authenticate a U.S. Drivers License. Now showing a mobile account opening using a phone and IOS Safari browser. Instead of filling out mobile form they use camera to capture image of back of DL. Enhanced and transformed image for data extraction. These folks are well-known for OCR/ICR. Showing instant approval for bank credit card. Cool. And fast. But what about fraud with a stolen driver’s license? I imagine they will address this issue; perhaps geo-location.

Michael Nelson and Sarah Clark @miteksystems http://www.miteksystems.com

^WM

Two products are being demoed today: Photo Fill and Photo Verify. With Photo Fill, you take a picture of a document (like a driver’s license), and it is scanned to pre-fill an online application. I really like this technology. It seems to me that some of this technology is native to my iPhone. I’m wondering if Mitek is building on that device capability, or are they substituting it? With the Photo Verify product, the credit issuer can obtain more complete validation of the customer (beyond typical authentication). Not only is the license scanned, the product is able to detect and interpret the invisible security features on state-issued IDs. ^SR

10:02 am

MoneyAmigo

MoneyAmigo

Christian Serrato. REALLY cool UI mobile app that is focused on the unbanked with an emphasis on the Hispanic population. Now showing international P2P payment system. It looks like they have not YET launched (stealth mode). Again, the user interfaces looks great; all of the demos are getting better and better. Patent Pending. “Want to partner”

Is this compliant? I would imagine but not sure.

@MyMoneyAmigo

http://www.moneyamigo.com/en_US/

From their web site:

much more than a bank

Free Money Amigo Account

- Fast sign-up

- No minimum balance

Free card

- Free debit card

- Free direct deposit

Free ATM

- Over 50,000 ATM’s

Instant low-cost $ transfers

- National and international

- Done in 3 clicks, 3 seconds

No hidden fees

- Never. Ever.

- You get what you see

Always mobile – never closed

- 24/7 service

- Spanish or English

Save even more

- Discounts while you shop

- Other money saving services ^WM

The product helps provide financial services for the underbanked, particularly Hispanic consumers. Helps users to find free or low-cost services, like a no-fee ATM. You can use the app to send money via SMS text message. Recipients can be in the US, or across the border to other countries (in the demo, they are sending money to Mexico). No forms for fund remittance, as easy as a text message. ^SR

09:49 am

HipPocket

HipPocket

Showing a white label app for banks; right now showing a kind of marketing message, PFM-type screen asking for demographic data. Showing a user that they are paying a higher mortgage rate than 71% of their peer group. I don’t think I’ve seen these folks before. I’m really glad so many demos today are mobile-based.

From their web site: Drive Quality Leads and Save Customers Money

Hip Pocket engages your mobile and website visitors by using social influence and personalized consultation to generate new, qualified mortgage or retirement leads. We help banks and credit unions provide an engaging, intuitive user experience that marries the emotional and logical purchase decisions.

Mark Zmarzly and Todd Cramer @BankMarketing http://hippocket.net/

^WM

“How does your bank rebuild trust and generate engagement online?” The tool drives mortgage and retirement leads. The app helps the user to create a peer group, to see if they would pay the same as people like them. There are rates presented to the customer, based on a bank’s specific offering. As the app provides rates, I’m wondering how they provide link to the required regulatory disclosures? With UDAAP, there are clear compliance requirements on rate-based advertising for consumer lending. ^SR

09:45 am

Encap Security

Encap Security

The product allows you to approve your wire transfer, without a call-back. With fingerprint scanner from your iPhone, you can approve your wire. The technology enables you to use the security that is native to your device. Encap offers “Omni-channel customer authentication platform”. This is the first company to discuss the customer experience, and viewing authentication from that customer perspective. Doesn’t just authenticate the user, the service also looks at the context of the transaction. ^SR

Showing Encap’s SDK which is integrated to a bank URL: West Springfield Bank; not sure if a real bank. They are showing two tablets and one phone showing authentication that are paired. Designed to integrated with a bank’s risk engine(s). It looks pretty slick. I’ve seen Encap present in the past. I believe the company’s HQ is in Norway.

From their web site: Encap Security provides the best way to secure access to applications and services using any platform – PC, mobile or tablet. Our patented multi-factor authentication technology enables smartphones and tablets to be used as transparent, banking-grade ID credentials .

^WM https://https://www.encapsecurity.com @Encapsecurity

– See more at: http://beyondthearc.com/blog/2015/fintech/the-latest-in-financial-services-innovation-from-finovate#sthash.zDZiq8HA.dpuf

09:43 am

3E Software

3E Software

These folks are based in Fayetteville, Arkansas and have been in business at least six year. They are showing a lending dashboard called TESLAR. It’s slick. It looks like a very good UI for lending. I don’t think I know these folks but I BET they developed this app/platform for a bank and then took it out to market but I think they were self-funded. This is true bank technology as opposed technology from FI’s push out to consumers which makes it unique. Integrates with core and other bank technology.

Joe Ehrhardt and David Ankeny @3esoftware http://www.3esoftware.com/

^WM

Their product is Teslar, a platform to help lenders operate more efficiently. The management dashboard is dense with information. Maybe a bit overwhelming? Given the high bar for user interfaces, this team may need to invest more on the front end. It looks like Teslar is a customized BI tool and dashboard for lenders. ^SR

09:27 am

DarcMatter

DarcMatter

Alternative investment platform. Interesting demo but it’s a bit complex. It’s a browser-based platform for alternative investing. Might this be a replacement for costly, time-consuming private placements? Let’s find out. Here is some info from their web site:

DarcMatter is a transparent platform for Alternative Investment Opportunities

Access pre-screened investment opportunities

Utilize fully integrated compliance and verification tools

Invest in diversified offerings with low minimums

RAISE CAPITAL

Technology-enabled private offering process

Compliant logistics and investor management

Secure dissemination of information and documents

Showing demo of a sample investment and investors reviewing the offers. I think this could be a good way for SMB’s to get funding. Sort of like Kickstarter for multi-million investments. “0 million in investor capital is using to source alternatives right now.”

Sang Lee and Stan Solodkyy @DarcMatterHQ https://www.darcmatter.com/

^WM

The site provides a platform for alternative investments, for qualified investors. The site operates under appropriate compliance requirements. For an investor, you’ll be able to do due diligence online. As the issuer, I can track investor behavior on the website. DarcMatter helps to connect highly specialized, niche, investments with investors who are qualified to participate. .5B in investments now on the platform. This is an interesting offering, I’m curious if it lowers the cost of offering. ^SR

09:19 am

FIS Mobile

Showing a demo with a mock ATM. Showing using mobile app to speed an ATM transaction. I understand the problem being solved. It’s such a pain to use an ATM in an airport or another card. Using QR code on mobile phone app to get his cash quickly at an ATM.

I had MY credit card cancelled traveling this week and my bank didn’t tell me; they just mailed me a new card but didn’t tell me. I had to call and have them FEDEX it to me at the hotel. This is a big problem and I’m glad FIS and other folks are working on this problem. I mean it; it’s a BIG problem for anyone who travels. “Commercially available across the U.S. with Diebold and NCR (I think)

Doug Brown @FISMobile http://www.fisglobal.com/

^WM

Cardless cash from FIS allows you to “preorder” your cash before you arrive at the ATM. The system uses QR codes, and you scan the code when you arrive at the machine. “The accounts are tokenized and protected.” They are currently in the field with NCR and Diebold machines. Their tech will enable the issuance of instant ATM/Debit cards at the ATM. ^SR @FISMobile http://www.fisglobal.com/

09:18 am

PayActiv

Well, it looks like our second presentation has three folks and I know at least one of them. Safwan Shah is brilliant . I learned a lot when I worked with him. I’m looking forward to hear what they have to say. Safwan sold his company to TSYS several years ago. “PayActiv.MyMo” Showing mobile app. Showing a mobile-based app for a wide variety of transactions, P2P, cash, bill pay and more. It’s like a “Swiss Army Knife” of mobile financial applications; it sounds like it does everything from mobile banking, P2P, PFM and more. “Developing tools for employers and over 10,000 users so far.” Great job. ^WM

Safwan Shah @PayActiv https://www.payactiv.com/ ^WM

Many people are living paycheck to paycheck, waiting every two weeks to get paid. PayActiv works to accelerate the payment of compensation to employees. Through a mobile app, it looks like individuals are able to enroll. Company rep Safwan Shah notes that there is a flat fee of .00. You can pick up cash from an ATM machine, or can use the service to pay bills. The offering seems to require both the company, and the individual, to enroll. ^SR

09:14 am

Top Image Systems

Top Image Systems

Making document requirements easy. I know and like these folks for a couple of reasons. One, I believe I’ve seen them present at Finovate in the past and like what I saw. Second, my friend Lynn Boggs, CEO of TransCentra uses their technology.

Showing mobile app to capture loan docs and data (using OCR/ICR?) which lets users view, edit and annotate any document on a loan. Notifications when docs are missing which is REAL important. My associate Steven thinks it’s an app but I THINK it’s a browser-based solution which is mobile optimized. “Powerful web client as well.” It looks slick.

The lending technology industry got CRUNCHED in 2008 and in general the industry is five years behind other sectors. I’m glad they have developed this (which a mobile app or browser-based) and am sure it will work as advertised.

Taylor Adkins & Alayne Pregeant @TopImageSystems http://www.topimagesystems.com/

^WM

This offering helps to support the lending process by providing a platform for managing documents. “Provides access from any mobile device.” The eFlow Lending tool can apply compliance requirements, at the document level. The app has a built-in web client that includes more functionality from TIS. The platform can identify the types of documents that have been uploaded. ^SR

09:05 am

Vouch First Presenter

Yee Lee @Vouch https://vouch.com/

“Community Built on Financial Trust” Showing mobile able. Is this a new type of credit reporting network? Just an idea. “A different style network.”

From their web site: The first social network for credit. When people vouch for you they can help you borrow more money and lower your rate, costing you less. Money for your loan comes from Vouch at rates from 5%–30%. To get a loan offer, you need to meet our credit criteria and get one vouch.

I’m not sure what they bring that is not available. I will have to visit their booth for more info later.

The first presenter of the day is Vouch, and their rep Yee Lee. Their product is about “creating the first social network for credit.” The network helps you to build up creditworthiness. People in your social circle are able to provide an opinion of your ability to manage money. This is not like twitter or facebook, a much higher level of trust is required. You pull together a group of “sponsors” who are willing to speak on your behalf. The power of the social network reduces interest rates for the borrower, on average by 6% according to Vouch. The app is on Apple and Google platforms. ^SR – See more at: http://beyondthearc.com/blog/2015/fintech/the-latest-in-financial-services-innovation-from-finovate#sthash.cMPkkbzY.dpuf

08:58 am

This is the 8th Finovate in the San Francisco/Silicon Valley area. I’m happy to say that I’ve been to most of them. ^SR

08:54 am

Welcome to Day 1 of the Spring Finovate show, live from San Jose, California. Beyond the Arc and the William Mills Agency will be blogging live. For the next two days you can tune in to learn more about the latest in technology and innovation in financial services.

It is now 5 minutes to show time. In two short days we’ll hear from almost 70 companies. In a series of 7 minute presentations, they’ll be discussing the innovations that their companies are bringing to market. I’ll be joined today by William Mills and KT Mills. Tomorrow Corina Jordan from the Beyond the Arc team will be joining us. ^SR

08:46 am

I’m here in San Jose, California at Finovate Spring 2015 with my friend Steven Ramirez, CEO of Beyond the Arc and William Mills Agency lead Digital Marketing Consultant K.T. Mills. It’s a great turnout here today and we will be live blogging this event over the next two days so check back often. Thanks!

^WM