William Mills Agency and Beyond the Arc will be live blogging at FinovateFall. Check back for new updates throughout the day. If you missed our commentary yesterday, you can catch up on Day 1 of Finovate.

William Mills III, Chief Executive Officer of William Mills Agency is live blogging today at FinovateFall 2014. He has more than 30 years of experience in financial technology and is a recognized leader in financial and technology marketing. He has personally advised more than 300 chief executives on marketing strategy, business development, mergers and acquisitions, company branding and public relations. You can contact him via email at william@williammills.com or on Twitter @williamemills.

William Mills III, Chief Executive Officer of William Mills Agency is live blogging today at FinovateFall 2014. He has more than 30 years of experience in financial technology and is a recognized leader in financial and technology marketing. He has personally advised more than 300 chief executives on marketing strategy, business development, mergers and acquisitions, company branding and public relations. You can contact him via email at william@williammills.com or on Twitter @williamemills.

Steven J. Ramirez is CEO of Beyond the Arc, Inc. The company helps clients to strengthen customer experience and to deploy data science and Big Data analytics to make marketing and operations more effective. Their social media data mining helps clients improve customer experience across products, channels and touchpoints. For more information about Beyond the Arc visit beyondthearc.com, call 1-877-676-3743, or email web@beyondthearc.net. Insights on social media, financial services and more are shared on their blog, or follow them on Twitter at @beyondthearc or on Google+.

06:02 pm

Best in Show at FinovateFall 2014

05:52 pm

FinovateFall Video Interview: Jim Breune, Owner of The Finovate Group

Steven Ramirez speaks with Jim Breune, one of the founders of Finovate to get his thoughts on themes from this year’s show as well as his vision of Finovate from the beginning.

05:43 pm

Best in Show getting ready to start. Standby.

03:52 pm

It’s the end of today’s demo. Voting for the Best in Show winners is going on right now, as well as the exhibits. Look out for Steven’s video of his conversation with Finovate’s co-founder.

Thank you! It has been two long days, over 70 companies, and a ton of insights about financial technology! We’ll post later when we learn the Best of Show winners! ^SR

03:50 pm

EyeLock – Anthony Antolino (Chief Marketing & Business Development Officer)and Jeff Carter (CTO) – This is an iris based authentication company. They are now showing a video that highlights their television and press coverage, much I think came from the CES show. There’s a log about facial recognition and Walt Mossberg seems to like it.

My thoughts: Guys, I think what you have created is great, BUT your corporate video was more about how much press coverage you have received, than a demo of your system. I would rather have seen more examples of your product in use, than how much press coverage you have received. All the same, kudos to you and your PR team.

There are 2 minutes left and NOW we are just starting to see the demo; this is what we came here to see!

I hope to see EyeLock here next year. william@williammills.com

It is an iris-scanner that unlocks all of your passwords. “Scans over 240 points on the iris of each eye.” It seems to me this would work well with Google Glass, if you had a front-facing camera. “We are privacy advocates.” They see themselves as a player in the internet of things (IoT). ^SR

03:43 pm

Backbase – Peter Chapman (Fintech Strategist) and Jelmer de Jong (Global Head of Marketing) Digital Banking Solutions. I’m sure I’ve seen them before, perhaps at Finovate. I’ve noticed a lot of folks are no longer saying mobile banking; it’s “digital banking.” They are now showing a web browser view of their platform, which is widget-based. Having the platform based on widgets makes a lot of sense; it almost looks like an application.

Backbase – Peter Chapman (Fintech Strategist) and Jelmer de Jong (Global Head of Marketing) Digital Banking Solutions. I’m sure I’ve seen them before, perhaps at Finovate. I’ve noticed a lot of folks are no longer saying mobile banking; it’s “digital banking.” They are now showing a web browser view of their platform, which is widget-based. Having the platform based on widgets makes a lot of sense; it almost looks like an application.

From their web site: ABN AMRO uses Backbase CXP as their enterprise portal, both employee and customer facing…

It would not surprise me if it was originally developed for ABN AMRO. Summary: Backbase is a software company, founded in the Netherlands in 2003, which has offices in Amsterdam, the Netherlands, New York, United States, Moscow, Russia and Singapore.

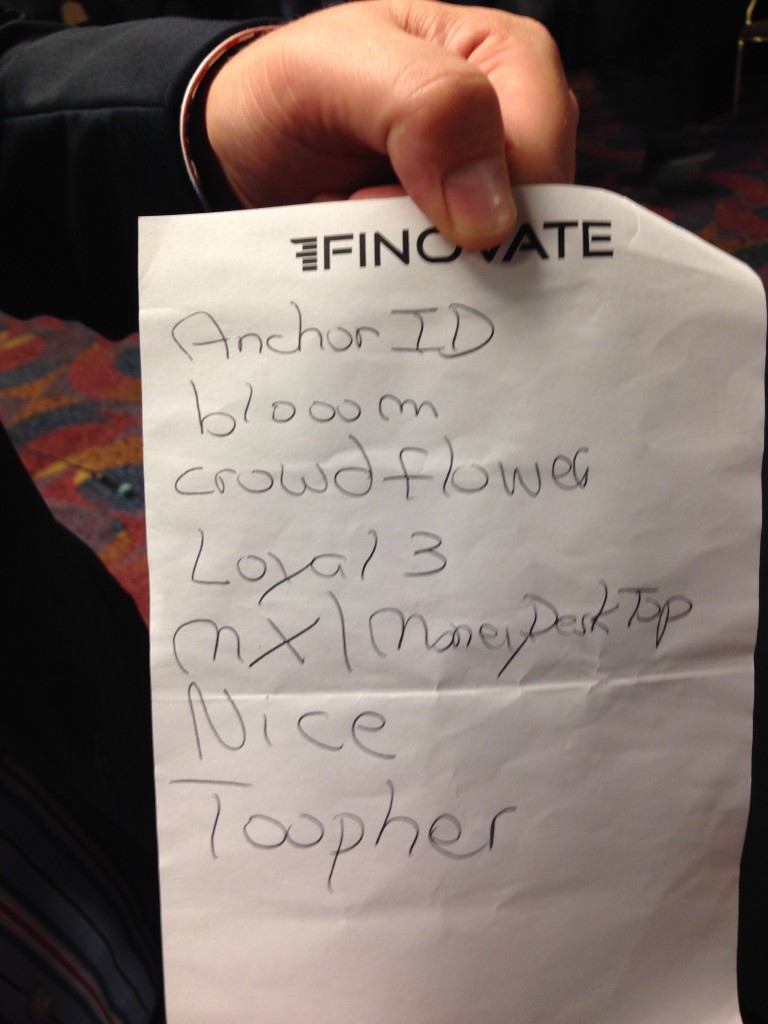

Now, this is interesting: they are showing tech partner logos like MoneyDesktop (now MX), Ensenta, Geezeo and Payveris (where my friend Mickey Goldwasser works). I’m interested in knowing how many US FI’s use Backbse.

They are now presenting an IOS version. This is very cool.william@williammills.com

Today, they are launching the mobile banking marketplace with widgets. They include several companies from Finovate: MoneyDesktop, Geezo, and others. Their strategy seems to be mixing-and-matching the best of breed of bank functionality. The marketplace allows you to easily implement technologies from fintech leaders, without having to work with each on a one-off basis. They offer one unified customer experience across a number of different providers. Backbase is known for their strong web design, including very simple, elegant mobile UIs. On Apple iOS, they can use native Apple device functionality. The Widgets run on any screen, any device. ^SR

03:35 pm

e-SignLive by Silanis – Tommy Petrogiannis (CEO & Co-Founder) and TJ Witte (Sr. Technical Consultant) From BIC: Silanis Technology is the leading provider of electronic signature process management solutions. The world’s largest insurance providers, financial services companies and government agencies depend on Silanis to reduce the time, cost and risks of getting signatures in critical business documents. Silanis enterprise platform solutions and cloud services enable organizations to replace their manual, pen and paper processes with an all-electronic web-based process for e-commerce and e-government transactions.

I think I’ve seen these folks at mortgage industry events or perhaps at ESRA. They have a very nice e-sign capture platform. They are a big player in this space and this is their first Finovate conference. I believe their HQ is in Montreal. william@williammills.com

03:27 pm

Linqto – Dune Thomas (VP Mobile Banking Solutions) and Bill Sarris (CEO). Their tagline is “50% of all banking customers do not want to bank online.” I’m not sure I’ve heard that, but I believe it. They are now showing a video about banking, BUT here is the twist; it’s on his phone, not at a self-service terminal. The call center person knew the customer is in NYC due to geo location. They are showing a check capture and now the CSR is showing the teller screen. This is all very cool. william@williammills.com

They’re demoing a remote capture of a check, during a live video call with a banker. The location information is delivered to the banker. I can imagine that video chat with the customer represents a huge potential for improving customer experience. You can see the banker, and both people can communicate non-verbally as well. PersonalBanker+ Linqto powers online video seminars that can be delivered over mobile. It also integrates text chat. “Remote banking, done fact-to-face.” ^SR

03:20 pm

MoneyStream – Mike Bertrand (CEO) and Gillian Verga (VP Product) From BIC: MoneyStream is the first, all-in-one smart money management service that links, coordinates and consolidates the fragmented tasks associated with banking, bill paying, record keeping, payment scheduling and cash flow management into a single online service.

Here is an excerpt from their blog:“PFM’s just didn’t work for me and my family. That’s why I started MoneyStream.”

It was a big surprise to hear last Friday that Manilla is closing its doors, effective July 1st. Since we’re very familiar with the pain consumers have trying to get their money organized, we’re deeply sympathetic to the frustration Manilla users must feel, after working to get their bills and accounts set up only to have Manilla go under. It seems like it was only a year ago Manilla was presenting at Finovate; times change.

william@williammills.com

A personal financial assistant to make managing your money easier. The platform creates the budget for the customer, based on advanced data analysis. With the system, it is very easy to swap bill payments between credit cards, really at the click of a button. In addition to reporting and analysis, it has integrated bill presentment and payment. ^SR

03:12 pm

LOYAL3 – Barry Schneider (CEO & Chairman) – Easy, affordable and FEE free for capital markets. It looks like they are getting ready to show an IOS app, which should be App Store next month. This is very easy to view. My question: how can folks invest without fees? They are showing brands (like Kraft) and people can invest as little as . I really like their concept. I want to know how they make money with their app/platform. They claim their mission is “not about buying stock, but becoming an owner of a company.” I like it. They are getting ready to show their social IPO i.e. GoPro. Man, I wish I had invested with GoPro when they went public and I had the chance (I’m glad I did not invest in Vonage many years ago). The have done six IPO’s, which I Believe were social media-based. This is very cool. They raised .6 million in 32 minutes for one IPO. Now, they are showing a video testimonial on LOYAL3 from GoPro’s CEO. I think this is very cool; they raised million within days with GoPro. They might be a Best of Show winner.

From our friends at BIC: LOYAL3 Holdings, Inc. and its subsidiary provide a Web and social media platform for public companies to sell their customer stock ownership plans directly to customers. LOYAL3 Holdings, Inc. was founded in 2008 and is based in San Francisco, California. LOYAL3 uses social technologies to democratize the capital markets, making stock ownership easy and affordable for everyone. LOYAL3 offers a technology platform where people can buy stock in their favorite brands, right from those companies’ Facebook pages and websites in 3 easy steps, invest as little as and zero fees.

william@williammills.com

Most Americans don’t have brokerage accounts. As an alternative, Loyal3 is a crowdfunding platform for capital markets. People can invest as little as in the brands they love. One of their offerings is a “social IPO” and they helped raise .3 mil in 32 minutes. This enables very small investors to invest in companies. They are a platform that is fully-scalable. The website has a video testimonial from CEO of GoPro. A lot of people got a chance to participate in the IPO. ^SR

03:10 pm

Video Recap: FinovateFall 2014 Day 2 Morning

William Mills, CEO of William Mills Agency, and Steven Ramirez, CEO of Beyond the Arc, review the standouts of FinovateFall Day 2 including Kabbage, Yodlee and CrowdFlower.

03:05 pm

Sr. Pago – Pablo Gonzalez Vargas (CEO & Co-Founder) From BIC: The solutions is aimed at the unbanked market. It allows users to accept credit card payments using their smartphone or tablet.

They have raised more than million in VC (they are based in Mexico City), but are looking for other partners and investors. william@williammills.com

Currently, they are addressing 78 million unbanked in Mexico, including small business owners. This is a debit card, without a bank account or tax ID. It isn’t immediately clear what makes this offering unique. They offer a bundled card, card reader, and mobile app for card system. ^SR

03:00 pm

FamDoo “The Modern Allowance” – is a mobile app/platform for savings. US BANK and their customers are their first loyalty partners. Users can convert FamDoo points to real cents for savings. The idea is to “reward work.” The app assigns tasks to kids/family members, then they can gain points that can be converted to currency (I would imagine). Now, they are showing an iPad version. I think this is a very cool concept. william@williammills.com

Mark’s experience is in creating and managing loyalty programs. This is a family-focused product, with an under-10 year old co-founder. This rewards program replaces the typical kid allowance, with the goal of promoting saving behaviors. They are calling it “the modern allowance”. ^SR

02:19 pm

We’re taking a short break. I’ll be back soon for the final round of presentations. Later today is the networking event, where they will announce this year’s Best in Show winners.

william@williammills.com

02:15 pm

Algomi – Stu Taylor (CEO) and Usman Khan (CTO) From BIC: Algomi collaborates with various communities, including stock exchanges, banks and trading firms, to connect users and provide real-time data required to make trade-related (buy and sell) decisions.

Algomi – Stu Taylor (CEO) and Usman Khan (CTO) From BIC: Algomi collaborates with various communities, including stock exchanges, banks and trading firms, to connect users and provide real-time data required to make trade-related (buy and sell) decisions.

They have 95 FTE’s, with offices in London and New York. Their concept is a social networking “take” for investment trading. JPMC is even a client. Their claim is that “we run the Honeycomb Network.” Now, they are showing a screen of bonds in the shape of a honeycomb. Their interface is nice and it has a different kind of look and feel. It reminds me of the periodic table in Chemistry class at FSU.

They note, “bonds only trade a few times a year.”

I like that Finovate Fall is in New York City, so we see a lot more international and investment-based technologies. I don’t usually find as many international companies in the Finovate Spring event in California. william@williammills.com

They use social networks for investment managers and insurance companies. They connect bond buyers and sellers, because many bonds don’t trade very frequently. They aim to answer the question: “which global bank can connect me to the right bond seller, without telegraphing this info to the entire market?” Their Honeycomb platform mines bond trading data to identify likely sellers (or buyers, depending on which end of the deal you’re on). They can handle billions of dollars of transactions on their platform. ^SR

02:08 pm

Powerlytics – Kevin Sheetz (CEO & Co-Founder) and Pat Brown (Sr. Director, Stategic Sales) “Powerful data, smarter decisions.” From BIC: Powerlytics’ market intelligence platform provides the most comprehensive, accurate and granular consumer and business financial data available. Underpinned by the financial statements of 27 million business and 144 million households, Powerlytics’ platform and products allow for unprecedented insights to understand risk, identify market opportunities and conduct predicative analytics, analysis and research with a degree of precession that turns insights into action.

Powerlytics – Kevin Sheetz (CEO & Co-Founder) and Pat Brown (Sr. Director, Stategic Sales) “Powerful data, smarter decisions.” From BIC: Powerlytics’ market intelligence platform provides the most comprehensive, accurate and granular consumer and business financial data available. Underpinned by the financial statements of 27 million business and 144 million households, Powerlytics’ platform and products allow for unprecedented insights to understand risk, identify market opportunities and conduct predicative analytics, analysis and research with a degree of precession that turns insights into action.

Powerlytics is launching a new product that resembles a lending workbench. This is a small business lending strategy platform. It looks pretty powerful; I’m not sure where they get their data.

Kevin was at KPMG for 17 years and was a partner and later had successful stints at Unisys and other tech companies, before starting Powerlytics. william@williammills.com

They use Big Data for better investment strategy. They allow FIs to use their data, and combine it with the organization’s own. The benchmark and other interactive reports help you to explore the data. They also have products for consumers and are looking for strategic partners. ^SR

02:01 pm

Anchor ID – David Schropfer (CEO) From BIC: Anchor ID, Inc. is a digital identity company that allows consumers to use one universal login, combined with smartphone authentication, to access sites across the web. From social networks to entertainment sites, online banking to ecommerce, using Anchor ID, consumers no longer have to remember multiple logins and passwords to securely transact on the web. Headquartered in New York, Anchor ID raised seed capital in January 2014 and will launch in the fall of 2014

They are announcing: “We have been live for two days.” It is authentication technology and gives at least five different choices for authentication: voice, PIN, AppleTouchID, location, etc. I think this is a pretty cool development, which looks flexible. william@williammills.com

01:55 pm

Geezeo – Shawn Ward (CEO) and Peter Glyman (President) “Engagement Banking.” They are proud to announce, “I was the first presenter at the first Finovate.”

I was there; I think I remember their presentation. That was a LONG time ago.

Now they are showing an IOS app. I think it is a new, SMB cash flow management system. From BIC: Geezeo helps organizations engage their base, reach new markets, and increase wallet share. More than 300 financial institutions leverage Geezeo’s PFM platform. Geezeo’s primary focus is to provide services and technologies that enable clients to engage their target audiences to make sound financial decisions around products your financial institution offers. william@williammills.com

01:48 pm

Minetta Brook – Deepak Bharadwaj (CEO & Founder) and Viplav Nigam (VP Engineering) “Big data Intelligence” Realtime Computational Linguistics Technology. Today, they are announcing knewsapp is live for the first 100 users. They have an interesting use of news analysis. They are going into a detailed explanation on how they value the coverage for investors. Now, they are showing the stocks Soros has invested in, and checking to see if any are getting more coverage in news, Twitter or blogs. I think this is pretty cool and have asked to be a beta tester of their product KnewsApp. It is Web-based and I think mobile versions are available. william@williammills.com

01:40 pm

Kapitall – Gaspard De Dreuzy (Co-Founder), Antonio Reyes (Head of Development) This is the third time they have presented at Finovate. From BIC: The platform fuses a traditional investment tool with gaming to make it more user-friendly and also aims to attract younger users.

More information from their web site: About Kapitall, Inc.

With an intuitive and playful user experience, Kapitall is the next generation investing platform where modern investors can learn about the market, research stocks and funds, share investing ideas, and build virtual and real brokerage portfolios. Interacting with company stocks is as easy as drag, drop and trade?. Founded in 2008 by video game entrepreneur Gaspard de Dreuzy and financial technologist Serge Kreiker, Kapitall uses the gaming experience to break the established online trading mold, as the leading investing platform for emerging investors. Jarrett Lilien, former E*TRADE President and COO, joined the team as CEO in 2012.

This is the “gamefication” of trading/investing. I suspected they are well-capitalized and I also found out that they have raised more than million in VC. william@williammills.com

This is an online platform for an investment-based tournament, sort of like fantasy football meets Wall Street. Investors can find and trade stocks in the DJ Index. This is an interesting idea, but not sure I understand the audience. ^SR

01:34 pm

NopSec – Steven Leonard (CMO) and Michelangelo Sidagni (CTO) From BIC: NopSec helps businesses to reduce the risk of cyber-attacks by managing the IT security vulnerabilities that matter most. We holistically manage IT security vulnerabilities for applications and infrastructure, on premises and in the cloud. NopSec’s software-as-a-service, Unified VRM, aggregates the results of vulnerability scanners, proactively prioritizes vulnerabilities based on business risk, and expedites remediation by automating the ticketing process and reports. I’m struggling to ascertain exactly what they do. I’m thinking it’s a platform for machine management to prevent fraud/malware. Perhaps this is something that Home Depot or Target should have used. I will have to learn more about these folks. URL: www.nopsec.com. NopSec: vulnerability risk management, vulnerability scanning, and penetration testing solutions. william@williammills.com

They use data science and analytics for vulnerability to intercept hacks and attacks. They also have a platform for managing remediation, identifying what you need to fix on the website. Has a built-in collaboration tool to fix problems that cross silos. They also use predictive analytics. ^SR

01:24 pm

SAS Games – Siobhan Mullen (CEO) and Stephen Scully (President) “Game-A-Thon” for college savings. Marketing tool for commercial and personal banking. I don’t recall seeing this company before. From BIC: Fully automated, easy-to-use, market-disrupting, patent-pending, activity-based fundraising tool for children’s college savings.

I have the pleasure of serving on Florida State’s College of Communication & Information Leadership Board and every year the total cost of higher education continues to skyrocket. In many cases it’s not the tuition; it’s the housing and other costs.

In Atlanta, the AVERAGE cost for an underclassman to attend Emory University is almost ,000 PER YEAR. I applaud what these folks are doing. It’s a game engine connected to social/mobile networks. “The best indicator whether someone will attend college is the amount of money saved in the student’s name, not the wealth of the student’s family”. Interesting information. It’s kind of like Kickstarter within a family network to help children attend higher education. william@williammills.com

It is a game-a-thon for college savings; it helps families to focus on saving for college. Saving is done in the name of the youth. They have a game engine and a number of kids-focused marketing promotions. Game-a-thon is like a walk-a-thon, and the games are educational, kids make progress in the game and get sponsored by friends and family. FIs can partner with SAS Games and the game can be named after the bank that sponsors a particular game. They are looking for a bank to sponsor the money transfers, into the savings accounts. Hmmm, that might be an issue if they are still looking for an official bank. ^SR

01:18 pm

CR2 – Kieran Kilcullen (Director, Sales & Marketing) and Patrick Simons (Principal Consultant) – I’ve seen these folks before and believe they have a pretty good offering. Now showing a “Dublin Bank” mobile banking app that LOOKS like a Windows Mobile app, but I’m pretty sure it’s on IOS. Lots of “tiles”, which I think will be more popular as Windows 8 comes into wider use.

From BIC: Enables customers to send instant cash using the banks’ network, from a mobile app that can be dispensed from an ATM without the use of the plastic card.Showing live video demo from Europe. Great use of live video and creative presentation. Now showing a function that lets users view through their phone camera with locations of banks. Pretty cool. The live video is working and they are showing a user at an ATM in Ireland. william@williammills.com

CR2 has an omni-channel platform for self-service banking and have now added mobile. The channels include ATM, mobile, online — all for a fairly seamless experience. It works with the bank’s existing channels. You can also send money, that a friend can retrieve from an ATM. Cool! ^SR

01:04 pm

Getting ready to start the afternoon sessions. Standby……

12:02 pm

BREAK – Be on the lookout for video updates one or two more times later today. William

12:00 pm

Based in Austin, Texas, Malauzai is one of the rare companies I know that have clear, concise vision coupled with smart, experienced talent with one of the best work environments. I believe this is the FIRST time the company is presenting here, but Malauzai technology has been a major part of at least TWO other Finovate demos over the years. “We serve over 300 FI’s around the United States. We create smart apps and end users have a much better experience. Internet banking as you know it is DEAD!” Lots of users are demanding a better experience, especially for tablets and desktops. “Smart phones are where we started.” They are now showing their smart web browser experience.

Now Robb is showing their iPad app, and it’s REALLY slick with a “carousel” view. What they are showing, which I have NOT seen from other folks (yet), is the mobile experience in a browser environment. “Smart Web Apps driven by same mobile user experience (because it is easy, people know how to use mobile apps intuitively) (paraphrase). One of their really cool functions is the ability to turn debit cards on and off manually using the Malauzai mobile app. It looks like it will be very popular on tablets and web browsers on a computer. MOX, Convergence and superior economics. I bet they will be a best of show winner if not a strong contender. william@williammills.com

They build custom apps for community banks, with an emphasis on next generation of mobile. “Apps running on the desktop.” I like this — really starts to bring a “mobile, first” philosophy to market. Large banks are far along this road, Malauzai Software looks like they are helping community banks with this challenge. Nice drag-and-drop functionality for the desktop. ^SR

11:50 am

Thinknum – Justin Zhen (Co-Founder) From our friends at BIC: Thinknum is a powerful web platform to value companies. Investors and financial analysts use Thinknum’s intuitive tools for research, data analysis, and collaboration enabling them to generate unique insights. Thinknum has aggregated over five million data series from thousands of sources and enables analysts to create and host financial models on the cloud. Users can share models and build off the expertise of others. Showing Thinknum’s technology creating Excel data. I’m not quite sure of the Unique Value Proposition, so I will have to do more research on the company. From their web site: A powerful web platform for financial analysis. Our Cashflow Model engine helps you value companies like a genius. I think it’s interesting technology and a fine company, but I’m noticing a trend. It seems like 1/2 of all FINTECH companies use the same template for the home pages of their web sites. Perhaps it’s a WordPress template. Again, I think this is pretty powerful technology for those who need this kind of data and presentation. william@williammills.com

This is a web platform for financial analysis; most financial analysts are not computer programmers. The UI looks like Google Docs, with a web-based spreadsheet. They’ve added functions that make it easier to do financial analysis, like grabbing data automatically from 10K reports. Also moves the computing power off your desktop, and over to the compute power of their cloud servers. ^SR

11:40 am

Knox Payments – Thomas Nicholas (President & Co-Founder) (secure.easy.payments). From our friends at BIC: Knox adds an additional layer of security on top of users’ online banking, and allows merchants and other users to make payments to and from bank accounts online for $CONTENT.18/ transaction, without the “middlemen’ of Visa or MasterCard. Now showing web app for a new account setup. New account opening technology is HOT. uMonitor sold to Harland FS (now D+H) and Andera recently sold for a TON of money (Kudo’s to Charlie on that). Knox Payments is now showing how fast to set up the account and then trade on a platform such as FOREX. “We are the only alternative to the credit card networks to underwrite transactions at a much lower cost.” william@williammills.com

Easy to sign up for a merchant account, online and in minutes. Funding accounts is also very straightforward. ^SR

11:36 am

Rippleshot – Randal Cox (Co-Founder & Chief Scientist) and Lucas Ward (CTO & Co-Founder) – I’ve heard that this company has good “buzz”. Their motto is stopping fraud at the speed of data. “We’ve known about the Home Depot data breach for four months.” Now showing dashboard of fraud transactions here in New York City. “Most of these breaches have never been announced – the dark matter of data breaches.” Very cool. Now showing a very local merchant here in NYC that has a TON of fraudulent transactions. From their web site: Rippleshot monitors millions of transactions daily and billions historically to identify where compromised cards visited a common merchant – the breached location. The remaining cards that had visited the breached location have not yet been identified by the issuer as compromised. They are at high risk for future fraudulent activity and need to be addressed.

I can really see this helps FI’s and merchants. I don’t know how much it costs but I would imagine it would really help FI’s and merchants. They are PCI compliant. I remember visiting First National Bank of Atlanta’s Credit Card Operations 35+ years ago (since acquired) and could not believe how much they had budgeted to charge off for fraud. I THINK it was about 20% of all of their transactions. william@williammills.com

They offer enhanced detection for fraud and data breaches. Interactive dashboards help to pinpoint vulnerable merchants, compromised cards, and more. They offer their service via PCI-compliant cloud, can provide time/location of every breach, and can quickly identify both large and emerging breaches. This is an important service given increasing exposure to merchants for data breaches. ^SR

11:29 am

Behalf – Benjy Feinberg (CEO) Andrew Abshere (Director, Product) (New company name). Again, another company that provides small business financing. Like I wrote earlier, this category is HOT. There must be a huge need as so many folks are here showing solutions in this area. Again, I it is my belief that Behalf and other organizations like it leverage 21st century technology to get cash to SMB’s in a way that is just not practical for traditional FI’s. Now showing web-based front end for the borrower. william@williammills.com

Financing for small busines customers – they pay the vendors on behalf of the company. This helps SMBs to manage their cash flow; Behalf pays the vendor, and provides repayment terms. I see the appeal of this offering and it takes some of the hassle out of vendor management. ^SR

11:21 am

WingCash – Bradley Wilkes (CEO & President)and Steve Curtis (VP & Director, Sales) and Vilash Poovala (CTO). “Revolutionizing the mobile wallet” Now showing IOS app. Speaking to the challenge of carrying all our credit/debit/loyalty/gift cards and frustration at the register. Their motto is “Life is Better With Cash”. WingCash carries payment cards, loyalty cards and more. I’m interested in how they make their money and their go-to-market strategy. Focused on processors and the merchant business. william@williammills.com

Cloud-based wallet for gift cards, currency, and “brand cash”. They include US$ currency, waiting to see how that gets funded. Brand Cash is a loyalty currency. The offering is focused on processors and acquirers of merchant accounts.^SR

11:13 am

Larky – Andrew Bank (Co-Founder) and Gregg Hammerman (Co-Founder) – Larky helps merchants build loyalty programs through their platform. From their web site: “Solutions for Credit unions, banks and health insurers.” Now speaking that most financial products (or at least 1/2) are not from a consumer’s primary FI. Now showing their IOS app, but I believe they are launching their Android app today. I know I’m sounding like a broken record, but once again, it’s a beautiful interface showing consumers location-based services and I assume banking/purchase behavior.

Larky – Andrew Bank (Co-Founder) and Gregg Hammerman (Co-Founder) – Larky helps merchants build loyalty programs through their platform. From their web site: “Solutions for Credit unions, banks and health insurers.” Now speaking that most financial products (or at least 1/2) are not from a consumer’s primary FI. Now showing their IOS app, but I believe they are launching their Android app today. I know I’m sounding like a broken record, but once again, it’s a beautiful interface showing consumers location-based services and I assume banking/purchase behavior.

From their company’s blog: Infographic: How Are Millennials Transforming the Banking Industry?

With over 86 million people in the generation known as Millennials (born early 1980’s to early 2000’s), the banking industry is poised to see a major shift in how people want to interact with their financial institutions. LARKY INTELLIGENCE has uncovered some amazing statistics to give you a glimpse into the future.

Now speaking to engaging millennials. This is the FIRST company this event that I can recall that is addressing millenials. william@williammills.com

Andrew Bank (Co-Founder) and Gregg Hammerman (Co-Founder) White-label, merchant- funded, point-of-sale (POS) discounts for consumers. Their aim: drive loyalty and card revenue. The answer is “contextual engagement” with set-it-and-forget-it functionality. My question is if the customer is going to make the purchase anyway, do you really want to offer them a discount? Perfect use case for predictive analyitcs: let’s just serve up discounts for customers not likely to buy without receiving a discount. ^SR

11:06 am

Hoyos Labs – Hector Hoyos (Founder, Chairman & CEO) Hector is showing the IOS app and the BofA credit card web site and now how it is linked to the mobile app. Using facial recognition for authentication. No user names, passwords, no tokens. “This is the consumer app launching next month for IOS and Android”. Now showing business application/implementation. “BANK OF AMERICAN IS USING THIS”. This is a big deal. B of A doesn’t like to let their vendors publicly speak about how B of A uses apps from bank vendors.

From our friends at BIC: Hoyos Labs is a Digital Infrastructure Security Company devoted to developing highly secured Identity Assertion Platforms capable of authenticating and assuring identities quickly yet accurately. Headquartered in New York City, Hoyos Labs Research and Development Division operates at the various geographies.

Now Hector is trying to “spoof” his own system using a video of himself. As expected, the app rejected the session. Pretty cool. william@williammills.com

From your mobile phone, they provide facial recognition and retina scan, and logs you in automatically to your account. No usernames, no passwords, no tokens. Launches for consumer use in October. And yes, they do have anti-hack technology (like asking you to raise your eyebrows to make sure you are not a fake picture.) System can tell the difference between live shot of you, and a recorded video. ^SR

10:59 am

Cachet Financial Solutions – Youri Bebic (SVP Mobile Innovations) and Kimberly Timmons (Relationship Manager). I’m sure I’ve see these foks before. Now showing very nice IOS app demo of Cachet’s client MoneyGram. Again, very nice UI. Showing Navy Federal CU app. From our friends at BIC: Cachet Financial Solutions is a leading financial services technology company, specializing in commercial and consumer remote deposit capture (RDC) solutions for financial institutions, credit unions, and financial service organizations. Cachet’s merchant capture solution (for both PC and Mac) and mobile applications provide greater freedom and flexibility for financial institutions and their customers.

What’s kind of interesting to me is that I’ve always thought of these folks as more of a remote deposit technology company. Everything I’m seeing now seems to be mobile app payments. Now showing analytics dashboard based on user data. From their web site:

Cachet Financial Solutions is a leading provider of cloud-based Saas remote deposit capture (RDC) solutions for banks, credit unions and other financial institutions. Remote and mobile deposit technologies are changing business and personal banking forever. And thanks to our leading industry platform, Cachet has simplified the process for delivering, implementing and servicing these remote solutions. william@williammills.com

Cachet describes themselves as “mobile for the prepaid world.” They aggregate best-in-class services (bill pay, remittance, rewards) and offer it as software as a service (SAAS). They are the first virtual agent of Moneygram. ^SR

10:06 am

Yodlee John Bird (Product Marketing, Yodlee), Jon Petz (Product Evangelist, Yodlee) and Avi Lele (CEO, Stockpile). Very creative conversation with a “banker”. Now showing an app using Yodlee’s API.

I’ve known Yodlee since the “dot com” days; besides being a survivor, they now seem to dominate as the personal finance data provider in this part of of the financial industry. I bet 50+ companies use Yodlee’s data to drive the front end screens of their apps. I believe they are on a “road show” and I expect an IPO from Yodlee some time this year. From BIC: Financial management platform that uses data analytics to provide financial insights to users. Platform components include data aggregation, Money Movement.

william@williammills.com

Yodleee presenting the frequent tension between developers and bankers; Yodlee helps to bridge the gap by aggregating bank data and exposing it to developers via robust APIs. Yodlee is uniquely positioned to serve both developers and banks. The developer panel makes working with the platform simple. Yodlee is having fun with their demo, I like the “Jekyll and Hyde”-inspired character who melds the hoodie-wearing coder and the straight-laced banker. Where’d you guys get that costume? ^SR

10:01 am

FinanceIT & FIS – Michael Garrity (CEO), Katie Robinson (SVP Strategic Innovation) and Paul Sehr (CTO) I was meeting with one of FinanceIT’s investors last week and I am really looking forward to their demo today. Katie from FIS is speaking today. FIS is led by a great guy, Frank Martire and they have acquired a TON of financial technology companies.

Launching FinanceIT product to US market today. Four years of operation in Canada. “POS Financing Platform”: We Offer Financing Everywhere.” Showing a demo of a merchant that uses FinanceIT. About FinanceIT from the TTC Capital web site: Financeit is a platform that makes it easy for businesses to boost sales by offering consumer financing to their customers from any device. The company brings point of sale financing tools to main street merchants to increase close rates and transaction size – a proven strategy previously reserved for big box retailers. Since launching in 2011, Financeit has signed up over 2,800 retail, vehicle, home improvement and healthcare businesses who have processed more than 0 million in loans.

Now showing the browser-based merchant dashboard and a customer is now at the merchant making the transaction and showing monthly payment and schedule and loan documentation. It looks like it is on-the-fly loan agreement, based on geography and regulations using an e-signature. Very slick. william@williammills.com

10:01 am

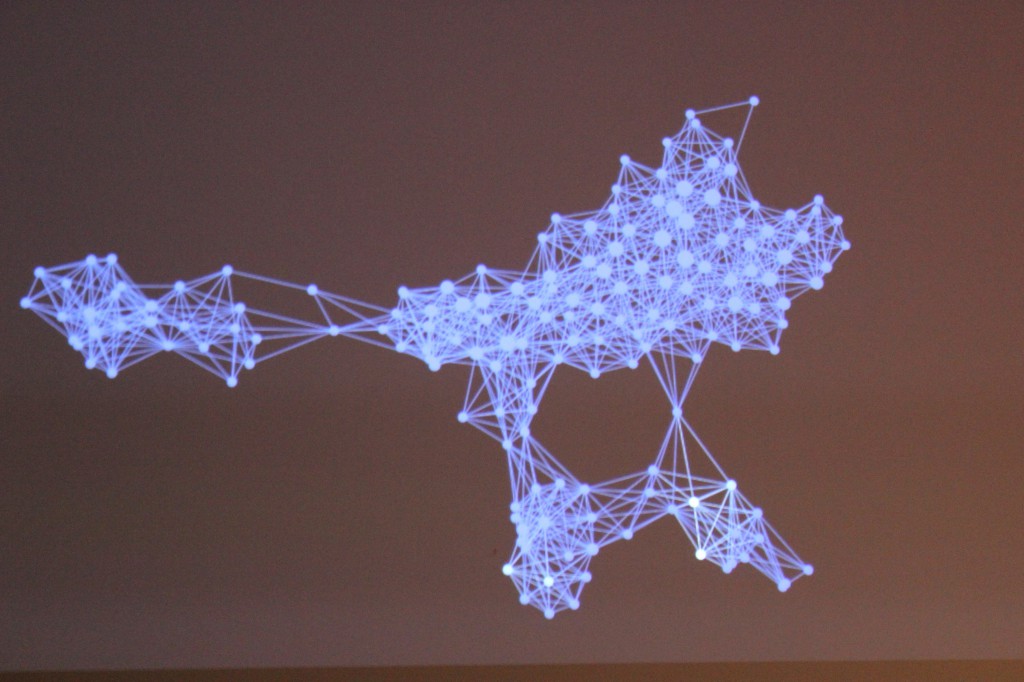

AYASDI screen capture

09:50 am

AYASDI – Michael Woods (Principal Data Strategist)and Max Song (Data Scientist). They work with 3 of the top 7. Ayasdi utilizes and works with some large FI’s on business models and customer intelligence. Good conversation, but I haven’t seen the demo yet. From BIC: Software that uses a combination of machine learning algorithms with topological data analysis that helps uncover intelligence from data.

Now showing very cool data helix, much like human DNA. Boy, this is VERY cool but way over my head. Color coded by FICO score. These are smart folks. It almost looks like like something out of “The Matrix”. Now showing how an FI would use the helix. I’ll try to upload a photo. Very interesting. william@williammills.com

This is a data science company that has commercialized techniques developed by DARPA. In financial services, they are looking at predictive models and customer intelligence. They have a data visualization platform, but it is not ready for primetime. This sounds like a data science lecture, not a discussion of innovation. (Not that I’m complaining! But they’ve completely lost the audience.) The finding: low FICO scores had higher risk of bankruptcy. Wow, hope the client didn’t have to pay for that! ^SR

09:45 am

BioCatch – Uri Rivner (Co-Founder & VP, Business Development & Cyber Strategy) From our friends at BIC: BioCatch is a leading provider of Cognitive Biometrics solutions for Mobile and Web applications. Available as a cloud-based solution, BioCatch collects and analyzes more than 400 bio-behavioral, cognitive and physiological parameters to generate a unique user profile. Banks and eCommerce websites and mobile apps use BioCatch to significantly reduce friction associated with risky transactions and protect users against cyber threats.

BioCatch – Uri Rivner (Co-Founder & VP, Business Development & Cyber Strategy) From our friends at BIC: BioCatch is a leading provider of Cognitive Biometrics solutions for Mobile and Web applications. Available as a cloud-based solution, BioCatch collects and analyzes more than 400 bio-behavioral, cognitive and physiological parameters to generate a unique user profile. Banks and eCommerce websites and mobile apps use BioCatch to significantly reduce friction associated with risky transactions and protect users against cyber threats.

Showing an iPad based application. Studies show how a user is interacting with a mobile banking application, I’m assuming for authentication. Perhaps the platform might provide an ability to cross-sell or create offers based on the movement of a smart phone. I heard a presentation from an ex-RSA last month on authentication via a person’s movement, so I think this is very cutting edge. Even is you have someone’s mobile phone, their email, bank account information and all passwords it is impossible (for now) to mimic someone’s unique movements: how they walk, hold their mobile phones, height and more. Very complex and interesting. william@williammills.com

Uri Rivner (Co-Founder & VP, Business Development & Cyber Strategy) They are trying to reduce customer “friction” from cumbersome fraud and authentication, by use of biometrics. Their example shows the onscreen pattern when you swipe your device. It tracks how you respond to the application. People actually are consistent, and the way they physically handle the device is unique. You can establish a baseline based on these user behaviors, and use this to detect fraudulent users. They also look at how you use the mouse, do you use the tab keys, do you click or hit “submit” to enter, do you use cut/paste, etc. Biometrics are really taking on a new character, with very different ways to analyze customer behavior. ^SR

09:38 am

CrowdFlower – Tatiana Josephy (VP Product) and Seth Teicher (Head of Content & Business Development) “We collect, clean and label data.” “Rich data, clean and easy to use.” Skybox/Google is a current client and they are showing a demo using Skybox. This is pretty cool. Skybox is a satellite imaging company that collects photos and has scientists to mark/input data based on satellite photos. For example, it can count the number of cars in a parking lot to determine how much traffic/business may have. Another client utilizes Crowdflower to collect data from SEC PDF documents. Their online workforce combs through SEC filings to collect the data. I’m guessing that CrowdFlower utilizes a paid crowdsourcing work force, so people can work when they want, for as long as they work (as opposed to outsourcing). I REALLY like what these folks are doing. Last example, one customer used Twitter data to predict stock prices. CrowdFlower helped this company analyze Twitter data on whether the Apple Watch will be successful. In 24 hours 1,400 people in their workforce studied thousands of Tweets for a cost of 0. That is amazing to me. I can see big things for these folks. It’s a fast, easy, low-cost solution that takes big data to rich (usable) data. I’m impressed and think they might be a “Best of Show” winner. william@williammills.com

Tatiana Josephy (VP Product) Product to clean and complete your Big Data. Data scientists spend 80% of their time cleaning up the data. They provide the person-power to help train machine learning algorithms. Their example is spotting cars in a parking lot, to help train an image recognition application. CrowdFlower can extract data from PDF, manual process to identify the key information. CrowdFlower is vetting who is working on your tasks. This is another competitor to Amazon Mechanical Turk. CrowdFlower’s online workforce analyzes sentiment and purchase intent from social media. For AppleWatch, they analyzed 27,000 tweets for 0. It isn’t about Big Data, it is more about Rich Data (annotated by people). ^SR

09:29 am

Vantiv – Coy Christensen (VP Product Management) with Jesse Kunicki (Development Manager). I met with folks from Vantiv last year at Money2020 and have been tracking them for the past year. In this demo they are showing triPOS (“try pos”), which I think is a merchant solution, perhaps like Square. We will find out. It uses the existing PIN device (like VeriFone). I’m not sure what the difference is between triPOS and existing merchant point-of-sale systems. Perhaps it’s an easy way for merchants to be able to EMV certified easily, as it only requires one EMV certification.

Vantiv, Inc. is a U.S.-based payment processing and technology solutions provider headquartered in the greater Cincinnati, Ohio area. william@williammills.com

Demostrating their TriPOS system. Vantiv has a tough challenge here. This is more of an infrastructure and pipes play, and I think they haven’t articulated their real value. The demo requires too much knowledge of payment processing. They are talking features, but not really benefits to the bank, to the merchant, or to the consumer. However, EMV is the story of the day in the card industry. They have technology to help companies make the transition to EMV. This is a product for payments developers. ^SR

09:22 am

Sender & PrivatBank – Egor Avetisov (Creative Director) and Maria Gurina (Deputy Head of E-Commerce) with Kristina Chaykovskaya (Head of E-Commerce)

Sender & PrivatBank – Egor Avetisov (Creative Director) and Maria Gurina (Deputy Head of E-Commerce) with Kristina Chaykovskaya (Head of E-Commerce)

Sender.mobi “MC has only one product, a credit card. Each bank needs to create their own online bank.” I’m quite sure what their app does but hopefully we will get to that. I think it’s awesome that they have one of their customers, a large bank, with them doing the presentation. They are now showing a chat-based IOS app where the person doing the demo is sending an invoice via the app and the recipient gets the invoice and pays via the app.

From Bank Innnovators Council (BIC): Messenger for businesses, enabling direct chat communication with customers. Sender – like Google’s Search Bar with endless possibilities. Sender – the last and only app.

william@williammills.com

Egor Avetisov (Creative Director) and Maria Gurina (Deputy Head of E-Commerce) Sender has their client, PrivatBank, up on stage with them. PrivatBank is one of the largest banks in Eastern Europe, and had a great presentation themselves at the last Finovate. Sender offers a chat-based peer-to-peer payment system. Very simple setup on the bank side, as well as easy to use by the customer. Sender is a platform for customer communications and payments. ^SR

09:15 am

Kabbage – Rob Frohwein (CEO & Co-Founder) and Kathryn Petralia (COO & Co-Founder) This Atlanta-based company has a great reputation. I believe I first saw them at a Finovate several years ago. Loans to SMB market. They put out more than 0 million last year (I believe in lending to SMB’s). They did launch in May 2010 at Finovate (San Francisco). Announcing “Karrot” “least expensive, fastest loan for consumers.” I’m interested in who will be doing the funding for Karrot. I think of Kabbage as a technology company as opposed to a lender, but technology is changing that. Capitol Access Network, OnDeck, Kabbage seemed to have unlocked the code on better financing using technology. What are FI’s role with Carrot? Now discussing the problems with ACH (24 -72 hour turnaround) and their solution using payment through debit card exchange for faster funds movement.

Kabbage – Rob Frohwein (CEO & Co-Founder) and Kathryn Petralia (COO & Co-Founder) This Atlanta-based company has a great reputation. I believe I first saw them at a Finovate several years ago. Loans to SMB market. They put out more than 0 million last year (I believe in lending to SMB’s). They did launch in May 2010 at Finovate (San Francisco). Announcing “Karrot” “least expensive, fastest loan for consumers.” I’m interested in who will be doing the funding for Karrot. I think of Kabbage as a technology company as opposed to a lender, but technology is changing that. Capitol Access Network, OnDeck, Kabbage seemed to have unlocked the code on better financing using technology. What are FI’s role with Carrot? Now discussing the problems with ACH (24 -72 hour turnaround) and their solution using payment through debit card exchange for faster funds movement.

One smart thing Kabbage has done is that they announced this PRIOR to today, so there is some press coverage of the new product during their presentation. Great kudos to Kabbage and their PR team.

william@williammills.com

Rob Frohwein (CEO & Co-Founder) and Kathryn Petralia (COO & Co-Founder) Kabbage provides working capital to small business, with over 0 million in loans. Their new offering is Karrot, a consumer loan product. They note it is the lowest cost loan option on the market. Their demo focuses on debt consolidation. You only need to submit last-4 of social security. It isn’t even a hard inquiry to the credit bureaus until/unless you accept the loan. Your financial information is pulled from your accounts automatically. Approval is within seconds, provided online. They don’t use ACH for money transfer, you link your debit card to your Karrot account for funding. Origination fee is deducted from the accepted loan. Institutional investors are funding the loans on the platform. This service can be provided white-label to banks and FIs. ^SR

09:03 am

Getting ready to start! Looking forward to a great day today with a super group of companies. william@williammills.com