07:27 pm

Congratulations to the winners of Best of Show at FinovateFall 2018! Banzai, Bond.AI, Bumped, Golden, and Meniga #Finovate

-2.jpg?width=297&name=Banzai%20(1)-2.jpg)

04:50 pm

Folks, we wrap up the demos now and wait for best of show which will be announced tonight.

This is my 23rd Finovate event and it has been a pleasure to be a part of Finovate Fall 2018. I’m sorry I will miss tomorrow’s conference sessions due to a commitment but look forward to attending either Finovate London or Finovate San Francisco next year.

Congratulations to the entire Finovate team.

William Mills, CEO

William Mills Agency

william@williammills.com

04:47 pm

Charlie India

Charlie India  Charlie-India: Charlie-India’s white-label platform resolves the integration of e-invoicing and payments for banks as backbone of a globally interoperable e-invoicing network.

Charlie-India: Charlie-India’s white-label platform resolves the integration of e-invoicing and payments for banks as backbone of a globally interoperable e-invoicing network.

www.charlie-india.com | Katalin Kauzli, Peter Malaczko & Janos Tőberling

“Create your own invoice solution for SMB’s without significant IT development” Solutions for banks and large corporates that want to provide their own invoicing services. Man, these folks are REALLY into invoices. ^WM

Their web site list banks as their primary tab so I suspect they have a some international banks using the technology – it looks fine but doesn’t look like a platform that a U.S. bank would use to me. From the web site: Invoice – Is a generally used data exchange document, which precedes each legal B2B payment. It is a multi-functional document: it stores several additional information. These data fields are not required by law, but support administration processes of the buyer or supplier: contain messages to other departments or the business partner (e.g PO numbers, item-level data).

eInvoice Solution. Servs banks and large corporates. They offer a web based solution for their clients. Why are they at Finovate? They built a solution to keep the payments at the banks, keeping the banks at the center. Open banking will allow outsiders to come in. Payments can be made directly from these e-invoices. ^DG

CharlieIndia wants to be a hub for invoicing activity. ^SR

04:40 pm

Sitehands

Sitehands combines the right skills, tools, instructions, and material to deliver IT field services for its customers, partners, and technicians.

www.sitehands.com | @GoSitehands | JP Rosato & Kelly Kamm

“Remaking IT field services.” “Field services are responsible for all those devices around us that make our technology work.” I like what these folks are saying. Showing a sample 1,000 site equipment refresh assignment, their platform and the I suspect the mobile interface for the IT field service workers. Based in Charlotte, NC these folks have raised .7 million in funding. Since they are based in Charlotte I bet they do a bunch of work for Bank of America and other large FI’s on the East Coast. JP, the CEO is based in New York so perhaps much of their work may be in the Northeast s well. ^WM

They bill themselves as IT Field Services 2.0. Demoed a mobile app. They work with some of the largest banks. ^DG

Field service technicians for large-scale technology roll-outs have very specialized support needs. Imagine deploying a teller platform that gets installed locally at 1000 sites. Sitehands helps to orchestrate this, sort of a project management platform on steroids. Many large projects are still trying to manage based on ticket-based service systems. ^SR

04:32 pm

Ballooning Nest Eggs

Ballooning Nest Eggs’ gifting platform allows parents to share their kids’ slew of celebrations and subtly prompt and easily enable their network to gift directly into the kids’ (pregnancy to age 13) investment accounts.

www.ballooningnesteggs.com | Amy Moses | Kent Wallgren

This is early stage company, New York-based with 0,000 in funding. “App is about parents sharing events and encourage gifting with our Sharing Celebration.” I applaud entrepreneurship and innovation and the fact that these folks are here. However, this is making me uncomfortable.

They are showing that a parent might post that their child lost a tooth, share it and connected it with a child’s investment account. Perhaps it’s me, but this much social sharing and connected to money just doesn’t resonate with me. I didn’t grow up with Facebook, Instagram, Twitter, et al. and I’m not a Millennial so perhaps it would appeal to a younger target segment. ^WM

A web based tool for parents to gift their kids or add funds to a kids investment account. Uses the old school ecard motif for the ecash gifts. Can track events too. Incremental marketing for FIs. Targeting millennial parents. Socially enabled. ^DG

The app is about celebrating kid’s major events, and promoting cash gifting that gets converted into stock investments. The app relies heavily on social sharing, with a focus on close family connections.

04:25 pm

James Finance

James Finance is a one-stop shop for credit risk management allowing lenders to easily create, validate, deploy, and monitor regulation-ready, high-performing predictive models. (Formerly known as Crowd Process)

www.james.finance | Pedro Fonseca | Gonçalo Garcia

“Helping lenders to adopt AI for the last four years.” “James – The AI for Credit Risk.” New York-based and have raised about million in funding to date. Showing a sample model on the platform and the feature dependency of a particular model. “We are a credit risk company that uses AI.” I’m pretty sure I saw them present last year.

From Crunchbase: James is a data science company, in the credit risk space. We started in 2013, and have been working on helping banks fight credit defaults using machine learning. The company’s flagship product is called James, and is a narrow AI for risk departments. It allows risk officers to build, test and validate credit scoring models.

Credit Risk AI Solution. Has both traditional risk dashboards and AI based models. The machine learning models and be reviewed by a human analyst, tweaked and then rebuilt. Risk officers remain in control. ^DG

Predictive anaytics and machine learning can be helpful in a number of scenarios. James uses these tools for better risk management. ^SR

04:17 pm

04:17 pm

StealthSecurity

OFX is a major attack vector  targeted by bad bots to gain access to confidential data your customers trust you to keep safe.

targeted by bad bots to gain access to confidential data your customers trust you to keep safe.

www.stealthsec.com | @StealthSecInc | Shreyans Mehta & Will Glazier

“We do bot detection on your application to protect apps from account takeover activity.” Based in Mountain View, California they have raised more than million in funding. From Crunchbase: Stealth Security defends over 100 million user accounts on some of the world’s largest online properties, from automated attacks. Stealth’s groundbreaking web security platform enables companies to protect their web, mobile, and API channels from automated attacks, bots and unwanted traffic that evade traditional security solutions, mitigating a wide variety of attacks such as credential stuffing and account takeover fraud, content scraping and theft, and application DDoS.

I wonder how much of their business is in the financial industry. TechCrunch did a story on their latest funding earlier this year which included this info: The company’s founding team came from PayPal, Cisco and Symantec, where they saw a problem for companies eradicating bots with off-the-shelf products. They decided to start a company to solve it. “We have an extensive background in network security, and we applied this and machine learning to solve this problem of handling bots,” company co-founder and CEO Ameya Talwalkar told TechCrunch.

They are showing a very comprehensive dashboard of their platform that protects data centers, sites and applications from attacks. I would imagine these folks will be very successful. ^WM

Security platform to identify account take over of bank systems. They actually serve all industry verticals. Demo included a live attack. ^DG

04:10 pm

Open Bank Project

Open Bank Project

Open Bank Project’s developer friendly and modern APIs move banks into the digital age.

Open Bank Project’s developer friendly and modern APIs move banks into the digital age.

www.openbankproject.com | @OpenBankProject | Simon Redfern & Ismail Chaib

I’m liking what I’m hearing. They are working with banks around the world including Citizens Bank in the U.S. so that banks and FinTech companies can explore API’s and SDK’s that are open source. “Developers like this. “ Brings innovation faster. Now showing the Citizens Bank Sandbox and their developer challenge. 10,000 developers working on the Open Bank Project. 40 customer banks so far. I LOVE THIS. Great job. Now showing a PFM Chatbot solution that was created and shared in the Open Bank Project. If I worked at an FI I’d be on this today. ^WM

They built the Citizens Bank API Sandbox. They have code on GitHub. The project also has administrative controls and monitoring tools for Citizens to control and monitor the users of their APIs. They showed an app built using their API. The app built also had voice UI. ^DG

Open source API to connect banks to a wide range of fintech providers. Citizens Bank in the U.S. has already rolled out a sandbox based on this API. I think banking as a platform will become the dominant way financial services is done. For a community bank or credit union, this becomes a very credible way to get in the game. For those not familiar with using APIs, not sure they’ve emphasized their unique advantages. ^SR

04:03 pm

04:03 pm

Vymo.jpg?width=300&name=vymo%20(1).jpg)

Vymo’s intelligent personal assistant uses automation and AI to increase sales productivity for enterprise teams. www.getvymo.com | @getvymo | Yamini Bhat, CEO

Founded three years ago, it looks like they are early stage and have raised million in VC some of it from a Sequoia Capital. From Business Insider: Vymo’s AI enabled personal assistant is used by some of the largest global financial institutions including AXA, Allianz, HDFC Bank, SBI, Liberty Mutual.

Showing iPhone app on a sample SMB customer. It’s like a beautiful CRM UI for an iPhone with customer, business, trend, appointments and more.

One of the developers was on the google Assistant team. Demo shows a mobile app screen (uses Google’s Material Design). The dashboard shows data from the CRM platform and publically available data. The tool helps identify ^DG

The demo is really more of a stand-up presentation. At least there is no powerpoint.

Ah, finally the demo! The app seems to add some interesting insights on top of a CRM platform. With algorithms they have developed, you can segment your customer population to pursue opportunities. I think there are some great ideas here, but not enough visibility provided by the demo. Looks like standard CRM functionality, so hard to spot the “secret sauce.” ^SR

03:58 pm

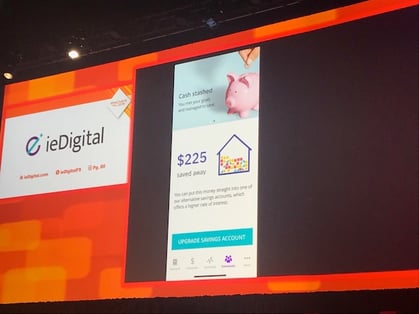

ieDigital

ieDigital’s financial health tool gives credit unions an opportunity to deepen their connection with customers by offering them a solution to manage their day-to-day cash flow.

www.iedigital.com | @ieDigitalFS | Simon Cadbury & Tom Stinton

UK-based Credit union solution: “Money Fitness” (also community banks). “The shape of money has changed. We’re shaping its digital future with smarter solutions for financial services.” There have been a number of saving tools for FI’s to offer their customers (or direct to consumer) I’m interested finding out what these folks are doing DIFFERENT than existing offerings. This company has been in business for decades and seems to have solutions to several types of industries. This is just a guess, but I’d surmise they developed an app/platform for a credit union and now is selling the platform to FI’s around the world. They clearly are good at create great user experiences. ^WM

A UK based Credit Union tool. Money Fitness reminds me of Moven. Some of the terms in the app are even the same. There are many differences like real time notifications to advise you. For example, a notification to suggest you ”stash” money on payday (triggered by your paycheck). ^DG

We’ve seen that people have a hard time managing their money on a day to day basis. That Starbucks habit gets expensive, fast. This app helps to better understand what you’re spending, and gives you an incentive to stay on track. ^SR

03:49 pm

CrediVia ![]()

CrediVia’s online lending marketplace optimizes loan financing for hospitality lenders and borrowers. Full disclosure: CrediVia is a William Mills Agency client.

www.credivia.com | @CrediVia | Anuj Mittal & Ajay Jain

CrediVia is a new startup having launched a marketplace that makes hotel financing “as easy as it is in Monopoly.” Platform does more than matching lenders to loans. CEO Anuj has been both a borrower and banker. Designed to give lenders precise targeting of leads – they only receive loan requests that fit their criteria. Most of the loan analysis is already done when leads come in, making it easier and faster to underwrite and close the loan.

Borrowers can publish a single loan request to multiple lenders at the same time. They just review the offers to get best loan terms. The application is adaptive for any loan type. Borrowers can also keep application data in CrediVia and retain it for future projects.

Starting off the demo Anuj and Ajay are showing the CrediVia dashboard starting at Loan Request first. It’s showing hotel properties that are looking for financing and the three interested lenders in the properties. Now showing the portal from the lending side where lenders can decide on the type of loans they are looking for. This will be a big help for those in the lodging industry and the lenders that provide financing for the industry. I’ve never seen anyone else doing anything like this. Great job! ^WM

Commercial real estate is often based on a manual underwriting process. CrediVia has portals for both borrower and lender, to aggregate information. The portfolio view shows all of your loans. And as a borrower, your application can be shared with multiple lenders. Loan offers are presented in a clear side-by-side presentation. Based on your selection criteria, the loans are evaluated for you. This is both a matchmaking platform, plus a loan analysis tool. ^SR

Commercial Real Estate / CRE: CrediVia is a portal for both lenders and borrowers. This is an efficient platform for both lenders and borrowers. Lenders can choose CRE projects based on their credit criteria and bid on only those projects. ^DG

03:43 pm

03:43 pm

Saylent Technologies -1.jpg?width=300&name=saylent%20(1)-1.jpg)

Saylent Technologies’ customer engagement platform translates data into actionable insights using experience, data science and machine learning.

www.saylent.com | @saylenttech | Damien Hayes & Russell Prettitore

Saylent was founded in 2006 and is based in Boston, Massachusetts. The company has raised million in VC. “Revolutionize customer engagement”

FI’s are spending a ton of money on big data. The challenge is monetizing the data.

They are showing a dashboard of at least eight areas of bank and data on a segment (like debit cards) where the banker can click through to the card to drill down to actionable data based on predictive analytics. For example, what might happen if the bank does NOTHING with this product/service? Showing results of segmentation of channel communication segmentation preferences. Now showing how you can use this data to create direct marketing materials. Based on my research it looks like they work mainly with community banks and credit unions.

Interesting demo. It looks real and working well at select FI’s. Good job.

^WM

An actionable data dashboard for banks. A self service analytics and insights platform. Includes predictive analytics and revenue projections on potential actions. It auto segments data and can even allow you to drill down to an actual campaign. It can allow for efficient deployment of multiple campaigns. Imagine being able to multiply your revenue generating marketing output with your existing staff. ^DG

How do you translate data and analytics into action? Saylent has an interactive dashboard that serves up actions, and potential options. The platform also helps you to identify and manage customer segments. You can also customize marketing materials to execute a campaign. ^SR

02:44 pm

Time for our LAST break. Be sure to be back at 3:25pm for the final session. Finovate often saves the best for last. See you soon.

02:41 pm

Alpharank .jpg?width=300&name=Alpharank%20(1).jpg)

Banks and credit unions acquire new deposits at lower cost using Alpharank’s Marketing Cloud – powered by the graph.

www.alpharank.io | @Alpharank | Brian Ley, Yoela Palkin

Facebook and LinkedIn have been collecting customer graphs for years. If you have credit and debit card information on your customers for 2-3 years, you can build your own customer graph. Alpharank takes your customer data and creates a customer graph to analyze deposit behavior. From there you can select the opportunity and determine the best channel for your segment. Alpharank recommends what product and content would perform the best. You can run campaigns that close the loop on your marketing and determine the ROI for your CFO such as new deposits. Combines marketing data and core data. Customer graph show how your customers are connected to each other and the groups that the most interact in. Example today is of PTA parents with a large deposit volume. Alpharank optimizes content over time and A/B tests the content for you. ^KT

Alpharank has been a prior presenter and winner at Finovate. They bring the customer graph to the world of banking. The idea is to work through personal networks to acquire new consumer accounts and promote cross-sell. From a modeling perspective, they use a “look-alike” approach. Presumably the bank can identify patterns of existing behavior, and then find more people with those characteristics. Looks like they have made their backend system into a platform that bank marketers could use. Alpharank tries to “measure the metrics that matter.” In addition to identifying the people, Alphrarank says they can identify the right channel and marketing content. ^SR

.jpg?width=502&name=alpharank%20(2).jpg)

02:35 pm

ebankIT.jpg?width=300&name=ebankIT%20(1).jpg)

ebankIT uses out-of-the-box digital channels for bank and credit union digital transformation.

@e_bank_it | www.ebankit.com | Vitor Barros, Pete Atkinson

Used the last 4:51 seconds of their demo time to create, build and deploy their baking solution. It can connect to some of the core providers out there. They used Mambu core for their demo. ^DG

Virtualization has taken the IT world by storm, yet we’ve seen very little of this tech shows up at Finovate. This cloud platform enables you to configure a full system from databases, connectors to a financial core, and more. This can be used to develop and deploy banking solutions. This is a very dense demo, they probably should have gone a little less deep and focus on value prop. Interesting, but not sure what they wanted me to take away from this. ^SR

.jpg?width=521&name=ebankit%20(2).jpg)

02:27 pm

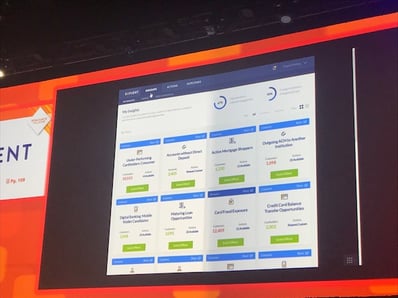

Envestnet Yodlee

Envestnet Yodlee’s Business Intelligence Solution allows financial institutions, wealth management firms and fintech companies to understand and sell new products and services to customers at the right time using breadth and depth of financial data coupled with AI-driven consumer apps and robust and easy to understand data analytics.

www.yodlee.com | @yodlee | Frank Coates, Dave Lieberman

Announcing Envestnet Intelligence for FIs. Allows any business professional to ask a question and get an immediate response. They gather data, natural language processing and AI. One to one questions available like “how many customers did I add this month?”. Can also ask multiple questions and put together a quick report. I have seen this type of technology demoed on the marketing side via HubSpot a year or so ago as well. Yodlee takes it a step further by generating visual reports based on chat instructions and intelligence gathering or “playlist”. ^KT

Envestment Intelligence is a multimodal business Alexa skill. It looks like they took the old school financial analyst report but turned it into an aLexa skill. It appears gimmick. It is first gen. The smartphone app is voice enabled. Voice is the new business UI. They are leading the way. If your bank has its data in order this would be a nice to have but if your data is in order, you probably already have easy access to this data not just voice enabled. They need to learn about Speech Synthesis Markup Language (SSML). It would make the voice interaction even better. ^DG

Envestnet/Yodlee is a veteran of Finovate and past Best of Show winner. Great company, and an early pioneer in fintech. Today’s demo shows off their Alexa skill, Investment Intelligence. This skill includes voice-enabled business intelligence/reporting of key metrics. They also have conversational search; just speak your search request. Powered by natural language processing and AI. Very strong offering, but I have to admit i’m not sure I fully understand the use case. It’s all here, Yodlee. Just need to make it clear who would use this, and for what specific purposes? ^SR

02:19 pm

DualAuth.jpg?width=300&name=DualAuth%20(1).jpg)

DualAuth secures payments through the use of mutual authentication via mobile and beacons.

www.dualauth.com | Jeri Suh, Heejun Shin

I believe that have demoed at Finovate before in 2016. Another password and authentication solution. Randomly generated auto password and use their fingerprint to verify the service and the service verifies the user. Concept of mutual authentication. From what I gather based on all the demos today, banks must use multiple types of authentication. A single layer of security will not cut it. Voice, face, password, key, mobile, beacon, fingerprint, etc. banks needs to have a second, third, fourth and fifth layer of security to verify the access. ^KT

A clever way to reimagine password entry. The website shows you a password code. A second factor, your mobile device also shows the password code. Like an authenticator app. If both codes are the same, you use your biometrics to confirm and you are logged in. ^DG

This technology combines password management and simultaneous biometric authentication. This also concludes a human-in-the-middle component for added security. They also offer a payment method that incorporates their authentication. They partner with IBM. ^SR

.jpg?width=411&name=dualauth%20(2).jpg)

02:11 pm

Banzai -2.jpg?width=300&name=Banzai%20(1)-2.jpg)

Banzai’s financial literacy solution uses a choose-your-own-adventure simulation allowing people to make decisions and experience consequences in a fun, safe environment.

www.teachbanzai.com | @teachbanzai | Landon Glenn

Real life simulation software for kids to see what it would look like when they graduated and see what it was like to pay bills. Bonzai is now in 50% of U.S. high schools. Successful because of Banzai teen, where the teens play a game and make different decisions on earnings and taxes. Now have banzai junior for elementary school. Also a game where the kid wants to purchase “mineshaft” and they work out a spending/savings plan with their parents to purchase the game. Cute AI and I can see how this would be really great for kids and teens.

Then came Banzai Plus – for adults/teachers that simulates the home buying process. To win the game, you have to save up enough money for the down payment and a good enough credit rating to purchase the home. Then banks demanded more content for their customers to place on their own website and use for content marketing. Banzai then provided a content library that you can interact with. This is also very interesting, I’d like to use this type of content for WMA’s clients as well. Track leads and usage as well with analytics. ^KT

A financial literacy game for kids. A brilliant solution for teaching young people about managing finances. They have built an experience based learning program. Now it is a platform for any industry vertical like a bank or credit union. The platform can even be used as a lead generation system and as a community development tool. ^DG

As an industry we talk a lot about consumer financial education, and financial literacy. But why is so much of the content so mediocre? Banzai has taken up the challenge with content geared to kids. They are using experienced based learning and gamification. They’ve expanded past the focus on kids with content for the whole family. Banzai also provides banking content to community partners. ^SR

02:05 pm

Onfido.jpg?width=300&name=Onfido%20(1).jpg)

Onfido’s AI-enabled technology uses facial biometrics and document checks to help global financial services businesses with digital identity verification.

www.onfido.com/gb | @onfido | Rob Connors, Joel Sacmar

“Identity is the new currency. Your identity is how you transact.” Business need to verify who their customers are. ID and a smartform is how you onboard users. First thing you do is take a picture of the ID. To make sure that the ID was submitted by the correct person, you do a biometric test. Face biometrics- A number challenge and a physical challenge to verify the user. So many demos today on authentication. ^KT

With every new data breach, it is clear that the legacy approach to passwords and authentication is inadequate. The fraudsters are just too good. Digital ID technologies are the wave of the future. Onfido covers hundred of countries, and you can use documents from around the world. Machine learning and human experts review the docs that are uploaded. There is an SDK that allows you to customize what you’ll use to verify identity. On top of this documentation, there are additional means to ensure you’ve got a real human on the other end of the device. This looks to be a very robust solution for digital onboarding. ^SR

Identity solutions provider. Processes identity cards with AI and advanced human agents. In addition to legacy ID collection, they use facial/audio video recording biometrics to further the ID verification process. ^DG

01:59 pm

RightCapital .jpg?width=300&name=RightCapital%20(1).jpg)

RightCapital’s financial planning API linked to its financial planning software allows financial advisory firms to provide planning advice for prospects and clients throughout their relationship.

www.rightcapital.com | @RightCapitalHQ | Shuang Chen, Dain Runestad

Announcing the launch of their new product – Financial Product API. Designed for financial advisors. Demo: financial advisor adds a new client and you can put in family and income information. 5-10 minutes for client to complete process. Then can see financial planning in action with assets, debt management, etc. ^KT

Launching an API for FIs. ^DG

.jpg?width=457&name=rightcapital%20(2).jpg)

01:52 pm

LoanScorecard.jpg?width=300&name=Loanscorecard%20(1).jpg)

LoanScorecard’s non-agency automated underwriting technology solves portfolio and non-QM lending challenges for financial institutions.

www.loanscorecard.com | @loanscorecard | Raj Parekh, Keegan Rodrigues

Showing their portfolio underwriter solution. Can access it form Loan Origination Software and analyzes it under your underwriting guidelines. Can embedded in back end systems. Demo: take any loan you want to originate or sell and run an analysis on it. Also created a new product – bank statement loan. Analyze 12 months of the statement data to give a true income calculation. ^KT

The platform can be used for loans that you originate, buy or sell. New product, income calculator, is for what is essentially a bank statement loan. It analyzes 12 months of bank data to make a lending decision. ^DG

Underwriting is still complicated, slow, and often aggravating (for everyone involved!) There is still opportunity for automated processes and enhanced digital functionality. This platform is an attempt to simplify this process. Well, process isn’t really simple, but at least simpler to execute. They also have a new product offering, Income Calculator, that assesses self-employment income. The platform’s strength is that it greatly improves documentation management. ^SR.jpg?width=426&name=loanscorecard%20(2).jpg)

01:45 pm

01:45 pm

Modelshop

Modelshop’s automation platform enables great agility for financial service firms creating intelligent business applications.

www.modelshop.com | @modelshopinc | Tom Tobin, James Marsh

Low code automation platform. Replace offline spreadsheets. Vendors been claiming to alternative to spreadsheets for years, how does Modelshop actually deliver? Ironically starting the demo with a spreadsheet. Risk spreadsheet with hundreds of calculations. Jumps over to modelshop for an online application. Dark UI, that’s unusual for finovate presenters. Tracks every calculation and every dependency. Traceability analysis and in credit report can view original source of data. Entire module is online. Business analysts plugged into digital transformation. ^KT

A spreadsheet-less model platform for building models. Can import data from spreadsheets or via JSON/XML formats. The tool shows the data a way that spreadsheets can not. The models can be researched/vetted by bank auditors. The models can be turned into RESTful APIs. That’s impressive. ^DG

Many banks and other FIs run their business based on a multitude of spreadsheets. Modelshop has a “low code” alternative that integrates data from many types of sources. They create the data model on-the-fly as it is imported. Using the data model and an auto-complete function, the relationships in the data are easier to document. The model lives online, and is accessible via REST API. So, this can power other internal and external systems. They try to reduce the time from Data >> Insight >> Action. ^SR

.jpg?width=436&name=modelshop%20(1).jpg)

01:38 pm

Lomsy.jpg?width=248&name=Lomsy%20(1).jpg)

Lomsy looks beyond credit scores to promote financial inclusion in underserved communities and among individuals with little credit history.

Lomsy.me | Enrique Huesca, Jose Ramon Pardinas, Enrique Castro

Necessity of understanding a different type of client. The platform is for Hispanic, 1st generation and 2nd generation Americans. To help Spanish-speaking clients in the U.S. ^KT

A financial inclusion based lending platform. This type of product is needed. the UI is very clean and focused. ^DG

They work with Spanish-speaking clients, particularly in the Southwest U.S. The sweet spot is people who prefer to transact business in Spanish, often from Mexico, El Salvador, and Central America more broadly. They use data from some of these countries of origin. This customer segment may not have a credit history in the US. This 2-year old company has decided to go deep to understand a key audience. ^SR

12:13 pm

Well, it’s time for a networking lunch break. Be sure to come back at 1:20pm EST today. WM

12:12 pm

LENDindex

LENDindex provides innovative lending and credit scoring solutions for small businesses and investors.

www.lendindex.com | @lendindex | Milla Bakhareva Artem Nabirkin Andrey Verbitsky

Backed by BDA Ventures.It looks like they are very early stage with their Internet-based platform for business credit scoring. Are any banks using it? From their VC: Lendindex – Big Data Algorithms and automated processes to score small businesses worldwide. I can’t find where they are located or much information about them. ^WM

An open business score. A credit score for business. Blockchain based lending. When onboarding a company, it does both a business and consumer KYC check. It seems efficient. ^DG

There have been very few mentions of crypto at this year’s Finovate. The LENDIndex platform incorporates both blockchain and crypto. The dashboard allows the lender to view the entire portfolio, and to approve individual loans.

12:07 pm

CashDirector

CashDirector

CashDirector’s Virtual CFO application uses an automated accounting platform integrated with online banking to improve SME lending & cash management.

www.cashdirector.com | Based in Poland| Patrycja Strzelecka, Geoffrey Nicholson, Rafal Strzelecki

“Help banks make more money, reduce risk and increase customer satisfaction for the SMB customers revoluting small business banking.” Free virtual CFO from the bank to the SMB’s. Showing the platform demo and how it feels like from a SMB view. Same look and feel as online banking platform. Accounting software integration such as QuckBooks. It sounds pretty cool and I think a couple of banks in Europe are using it but I’d like to know how many banks and SMB’s are using it and if so, are any U.S. banks using it. From their web site: 50,000 small businesses are using it. They should have started with that data; it sounds big in Poland if not other EU countries. ^WM

Banks can now offer a differentiated solution for their small business customers. Having this on the banks product suite allows a bank to help their small business customers run their business from a financial standpoint while assisting in improving their clients efficiency. Additionally it helps with the efficiency around cross-selling and upselling. They called it a Robo CFO. ^DG

This is a service that banks can offer to their SMB customers. It is an accounting system for small business. This can be an incentive for small business customers to make the bank its primary FI. The platform can be used to manage cashflow, including easy application for business loan products. This is a product that can be integrated into online banking. They call it a “digital CFO.” They say they can get a bank on the platform within 3 months. ^SR

11:59 am

Biometric Signature ID

Biometric Signature ID uses biometric passwords drawn with a finger or mouse to help financial institutions prevent imposters from stealing passwords and committing fraud.

www.biosig-id.com | @biosigid | Jeff Maynard, Chad Steen, Rich Madison

Based in Dallas and in business since 1995 with .3 million in funding. Draw your password, don’t type it. This sound pretty cool as I bet everyone has a different way they sign stuff, whether on their phone or their computer. “Gesture biometric” no hardware or software to download and 13 million users across the world. Pretty cool sounding so far. Brought Nationwide Mortgage (a client) which is always a good idea. Good job. ^WM

A password replacement vendor. No mention of the FIDO alliance (The specifications and certifications from the FIDO Alliance enable an interoperable ecosystem of hardware-, mobile- and biometrics-based authenticators that can be used with many apps and websites. This ecosystem enables enterprises and service providers to deploy strong authentication solutions that reduce reliance on passwords and protect against phishing, man-in-the-middle and replay attacks using stolen passwords.). They also use SMS as part of their process. SMS is not secure and easily hackable. Is this a smart solution for a world where passwords are going away? ^DG

11:51 am

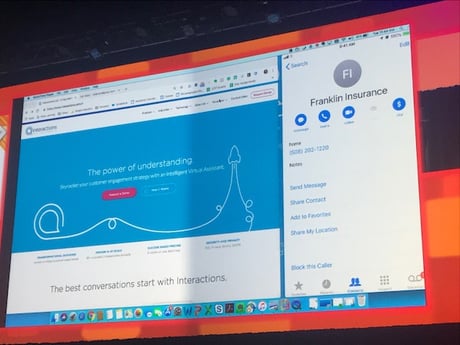

Interactions

Interactions’ omnichannel Intelligent Virtual Assistant (IVA) uses a blend of AI and human understanding to solve frustrating customer experiences with banks.

www.interactions.com | @interactionsco | Dan Fox Priyanka Tiwari

Large independent AI company – this is a BIG company. “ Interactions develops award-winning intelligent virtual assistant solutions used by Fortune 500 companies worldwide.” They have raised over 2 million in VC. “The power of understanding” Showing fictional Franklin Insurance demo. Showing a customer calling that has lost their insurance ID card and how they can retrieve it via email using voice/AI. Nice interaction, probably faster than a real CSR. ^WM

AI powered intelligent assistant. Showcased very little friction on several channels. Alexa portion of demo failed due to no internet connection. Questions for me revolve around security and initial customer onboarding to get everything initially configured. ^DG

11:43 am

AI Foundry

AI Foundry’s end-to-end mortgage origination solution uses AI and machine learning to extract relevant data and classify documents to improve data sharing and comparing for banks and mortgage origination companies.

www.aifoundry.com | @AIFoundry | Stephen Butler Alla Eizenberg Adam Lombardo

Based in Boston – this company is owned by Kodak Alaris

“New robot technology debuting today.” I’m sure I’ve seen these folks before and they seem like they have cool stuff. They have a REAL CUSTOMER – a lender – on stage which is always a great idea. Showing an example of a new home loan using an existing Encompass LOS and getting the underwriting information. The lender is talking about how it used to take three weeks to go through the underwriting issues. “Digital Mortgage Agent Robot” will cut the time for the tasks to process to make underwriting faster than three weeks. I’m interested in seeing how fast this will take with the AI. It sounds like they have been able to cut parts of the approval process down to less than a minute. It’s not ALL the issues but it’s really faster. Great stuff. ^WM

Brought a live client on stage. They are showing AI driven Robotic Process Automation solution for mortgage origination. The platform identifies the gaps to loan documentation and uses AI to extract the information needed from the supplied digital copy of paper documents. THe AI both extracts data and makes decisions to ^DG

AI Foundry has a platform to help automate loan underwriting, in this case for mortgage. There is a huge upside in reducing the cumbersome, manual, processes that are a hallmark of home lending. ^SR

11:35 am

unblu

unblu helps the world’s leading banks to increase revenue and reduce costs by delivering an in-person experience online that helps them provide a better user experience to their prospects and customers.

www.unblu.com | @unblu | Luc Haldimann Jens Rabe

It looks like that have several big International banks as clients. Showing a simulator (I’d prefer to see it on a phone and not a simulator) of their app. It looks like they are based in Switzerland and have been in business about 10 years. Now showing how the platform looks to CSR at the bank showing a video interaction co-browsing with the borrower. It’s a pretty cool technology. ^WM

Secure messaging solution for banks. Both desktop and mobile. Showed both text, video and co-browsing. It even has a collaboration space. ^DG

Secure messenger for the banking industry, with call browsing and chat. Recreate the in-person experience with digital channels. I like the co-browsing functionality, very surprised that this isn’t even more common. ^SR

11:28 am

Golden

Golden’s financial assistant app helps the 75 million baby-boomer adults managing the finances of 50 million senior parents.

www.joingolden.com | Evin Ollinger Drew Gorham

Interesting start. They brought their “Mom” with them. Good idea to standout in your demo. “Financial Care for Your Parents”. Man, this is a big and growing problem for a lot of people I know. “Family Collaboration Plaform starts with a Life Score, like a credit score that shows a parent’s financial wellness.” Now showing Mom’s accounts and their balances. This is going really well. Now showing Mom bringing out a bill and Golden scans the bill with the phone and it’s loaded on the system and now can pay from Mom’s account, his account or a credit card. Great use of humor. It looks like it can help cuts bill costs through analysis. Now showing income and what Mom might receive in additional government benefits. Now showing fraud alerts. This is unique, I don’t think I’ve seen a solution like this at Finovate. Great job! ^WM

An AARP Winner – Judges Choice Financial Innovation. Think account aggregation/PFM for children (legal caregivers) of seniors. Can also help reduce recurring expenses. It also helps review whether the seniors qualifies for government assistance. Helps fight senior fraud too. Benefits advisory or bank, reduced ^DG

As the sandwich generation takes care of elderly parents, getting a handle on finances can be a challenge. This offers very robust functions on both the expense management and income sides. With account aggregation, caregivers can get a fuller view of balances and transactions. Automated alerts push important information, so you don’t have to rely on charts and graphs. This is the right solution! Go take a deeper look. ^SR

11:21 am

Sezzle

Sezzle’s payment platform solves the lack of credit available to young consumers using gamification and progressive credit profiling to give them purchasing power when they need it.

www.sezzle.com

Charlie Youakim

Launched product 12 months ago and and have 2,000 merchants on their platform. It enables consumers to divide their payments of purchases over installments. “First time checkouts take only minutes.” Continue to grow week to week. Works for low order value items; like 0. It’s free for the customers. This sounds like 21st Century “layaway”. It sounds like they are really growing. I’m assuming the merchant pays them a percent of the transaction in order to keep the financing cost to $CONTENT for the consumer.

These folks are based in Minneapolis and have raised about million in VC. From Crunchbase: Sezzle allows shoppers to “Shop Now & Pay Later”. Shoppers checkout with Sezzle to pay their orders off in 4 interest-free installments, payable every 2 weeks. Our payment system enables higher average order values and conversion rates at our merchant partner sites.

They had some nice coverage in their local newspaper earlier this year: http://www.startribune.com/sezzle-online-installment-plans-appeal-to-millennials-without-credit-cards/482341142/

Very interesting. Good job! ^WM

Realtime installment payment option for those without a consumer credit line (credit card, personal, etc.) Showcased a 0 item paid via 4 payments of . Solution is credit for those without a credit profile. Has a positive impact at the merchants using the solution. Simple first time user onboarding. Subsequent uses very simple. Focuses on simple merchant integration and consumer onboarding. ^DG

Credit scores are pretty inadequate when you want to assess younger consumers. There have been some interesting developments in using alternative data. Sezzle is targeting this space. The app enables consumers to obtain credit at point-of-sale (POS). They have hooks into several ecommerce platforms including Shopify and Salesforce.

11:13 am

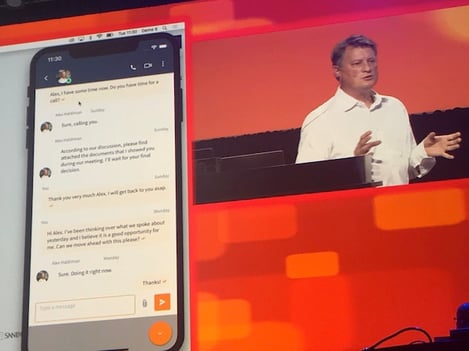

Bond.ai

Bond.ai’s ’empathy engine’ — a human-centered AI platform — closes the gap and disconnect between banks & consumers.

www.bond.ai | Uday Akkaraju Jared Landrum

I found this article from 2017 on Bond.ai: FinTech Grad Bond.ai Moving to Little Rock

by Arkansas Business Staff on Friday, Sep. 1, 2017 3:24 pm

The Venture Center of Little Rock announced Friday that Bond.ai, a graduate of the center’s 2017 VC FinTech Accelerator, will relocate its headquarters to Little Rock from New York City.

https://www.arkansasbusiness.com/article/118586/fintech-grad-bondai-moving-to-little-rock

It looks like they are based in Arkansas now. “Power your Internet, mobile, back office and more through voice.” Showing demo with Alexa on account balance and providing an insight into the account. It seems to be a AI overlay for voice for banking. Showing really nice UI on a mobile banking app – although this MIGHT be a slide-type demo as opposed to a real app in use.

The Alexa demo is going well and really interactive. These have folks have done some good work to make Alexa a real interactive experience provided it is integrated with Bond.ai and the banks legacy technologies. They say they are integrated with several cores and mobile providers and used in some banks in Europe.

^WM

Trying to help solve the bank AI gap as compared to Google, Amazon, etc. Showing an Alexa solution that mimics what Moven does today as it relates to balance and category spending. It has an empathy engine. The Alexa skill demoed showed advanced voice tweaking via , and multi-session data gathering. ^DG

We’ve all seen it… it’s never easy to promote innovation within an organization. And most efforts fail to reach objectives. This often happens because the company doesn’t have an end-to-end methodology. This platform helps you to form a hypothesis, validate it, and plan for scale. The platform is about making innovative ideas real, and helping you be more systematic. ^SR

11:02 am

Getting ready to start, standby…….

10:15 am

Time for a short break. See you at 11am EST. William Mills

10:13 am

Round Pegs

Round Pegs’ platform channels the agility of startups for businesses undertaking digital transformation.

www.roundpegsinc.com

@roundpegsinc

Pedro Donati, Bruno Falabella

A way of building a business focusing on collaboration and key assets to move from ideation to research to building the business module to experiment and finally to building the innovation plan. A way to find product market fit before writing a single line of code. Understanding your audience and cost. Good for pitching a new idea in your company, can use this to formulate your plan and innovate. ^KT

A platform to help legacy style companies build services the startup way. The platform acts as a guide. ^DG

We’ve all seen it… it’s never easy to promote innovation within an organization. And most efforts fail to reach objectives. This often happens because the company doesn’t have an end-to-end methodology. This platform helps you to form a hypothesis, validate it, and plan for scale. The platform is about making innovative ideas real, and helping you be more systematic. ^SR

10:06 am

Horizn’s Knowledge Platform.png?width=300&name=Horizn%20(1).png)

Horizn’s Knowledge Platform solves digital adoption and digital transformation for financial service employees and their customers using proprietary micro-learning and engagement methodology.

www.horizn.com | @horiznplatform | Janice Diner, Steve Frook

FinTech company to help FI’s drive digital adoption from employees to customers and across bank silos. On average increase digital adoption rates by 25% for their clients. Showing 5 ways they are increasing digital adoption. Now showing employee platform where you can get your employees to be digital fluent and trained fast (6-8 weeks). Platform readies them for digital conversations within the branch. Also can use the tool in branch to walk customers through digital related questions. Using SEO and adwords to answer user’s question via their training modules. ^KT

Digitally fluency service. Platform trains customer facing employees to be digitally fluent so that they can do their part to get customers digitally fluent. All this training has a goal increased digital adoption for their client banks. Also has training modules for customers. Can be in-app or online. It can even be SEO optimized. They shared measurable positive results. ^DG

This is an interactive learning platform to support digital banking. This can work on any screen anywhere. This training can also be customer-facing. Customers can get answers without having to call or go into a branch. The learning resources can be incorporated directly into a bank’s mobile app. The focus is on increasing digital adoption. ^SR

09:58 am

Arcanum Technology

Arcanum Technology’s authentication solution uses a patented dynamic virtual interface leveraging proprietary DARC Cipher to combat password/data breach/hacks and password fatigue for financial institutions and services.

www.arcanumtechnology.net | Brian Finnan, Brooks Brown

Average cost of a data breach today is .8 million. Arcanum is trying to solve for this. Shoulder surfing and key logging no longer a threat. Showing a N-kod where you have a virtual interface where you select your code. Can use numbers, symbols, emoticons, cartoon characters, etc. Each character has a set number in the back end that is different across all companies. So one hack does not cause a breach across all logins. This can do away with phishing completely because of dynamic attributes that you as a bank can change on the back end but the user can enter the same thing. For example “a white star” for BofA is 63 but for American express it could be 14. You can change the values on the back end but the user can still click “a white star.” ^KT

The technology is a password replacement. What is unique about this solution? You create one code but that code is stored differently at every partner site. That is one password the user needs to remember but every partner site stores that differently. When one is breached it only impacts that one site. ^DG

Wow, 3 billion passwords stolen every year! With N-Cod, they have an end user interface that helps to mask a user’s actual password. This is not about password hashing, they have a unique on-screen presentation of the passcode. So this is a backend system for maintaining passwords. This is accomplished on a specialized keypad that only appears onscreen. I’m not doing full justice to this solution, so you’ll need to go check out their site. This is worth a closer look! ^SR

09:52 am

Simpler Trading

Simpler Trading’s charting software gives both early and expert traders insights into investments.

www.simplertrading.com | @simpleroptions | Mandy Ditmire, Raghee Horner, Danielle Shay Gum

Educational and retail space for traders and investors. “From 0 to Trading” Evolution of retail training education. Demo: Users can login to their site and view the options or futures or training. User can view the chat room where you see all of simpler trading charts and trades. Clients can see my watchlist and alerts that user set for them. ^KT

Educational platform. Similar look to other online educational platforms. What is is training with their live trading charts. Their charting platform is designed for interactive training in real time. ^DG

Being a trader is a tough job, and it burns people out. So with that ever-present turnover, getting new traders up to speed fast is really important. This is a set of digital tools for training. I don’t think I’ve seen a product like this at Finovate before. ^SR

09:43 am

Ak Bars (Face2Pay)

Ak Bars Digital Technologies’ video validation system allows retail businesses to accept payments by leveraging highly accurate recognition models.

Akbars.digital Ilya Velder, Damir Galiev, Yaroslav Shuvaev

Discussing face recognition. Looks like back-to-back voice authentication vs. face authentication on the finovate state. Who will win? Ak Bars discussing Face to Pay product. Demo starts by adding your face to the app. Link your face to your payment card and then you can go to someplace like Finovate.com and purchase tickets for the conference. The app would then scan your face and purchase the tickets. (White-label available) ^KT

#Face2Pay. Demoed showing paying for a cup of coffee with face. Then demoed buying Finovate 2019 event tickets with Pace2Pay. They focused on making it friendly for both consumers and merchants. A white label solution. ^DG

Is it too cliche to reference Minority Report when discussing super cool techy stuff? You setup an account in seconds on your phone. And with facial ID, you authorize the payment. Certainly makes that fingerprint scanner seem quaint. The way they describe the value prop: safe, quick, and simple. And I believe it. They have an SDK to incorporate this tech into your application. ^SR

09:40 am

Fortr3ss-1.jpg?width=239&name=Fortr3ss%20(1)-1.jpg)

Fortr3ss’ Oracle service to Corda and Ethereum blockchains uses intelligent voice biometrics and artificial intelligence to solve the identity of node players in smart contracts for financial and healthcare institutions adopting blockchain.

www.fortr3ss.com @Fortr3ssinc Alessandro Chiarini

3 second demo – combination of two methods for password – key/password and voice. Voice reads key and then can access the dashboard manager where you can then log into a variety of apps like Credit Karma, Amex, Bank, etc. without having to enter your password every time. You can also store your IDs and secure notes. Demoing from BofA chatbot that could not tell the user’s identity. Fortr3ss is working in financial, healthcare and comcast industry sectors. ^KT

#VoiceBiometrics, Password Manager, voice driven payments, digitizes ID’s, (not a digital ID), They are an identity provider. ^DG

Intelligent biometrics company. It combines passive biometric (monitors the way you use your device), and then voice verification. Fortress ID is a password manager. They also offer a payment option, and a digital ID solution. With all of these components, the offering has become more of a dashboard. They see themselves as a platform for managing digital identity, secure by biometrics. However, they see their main value as helping to improve customer experience. ^SR

09:34 am

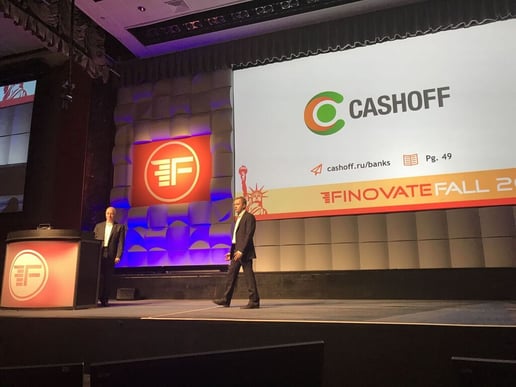

Cashoff.jpg?width=222&name=Cashoff%20(1).jpg)

Cashoff enhances customer engagement with its loyalty program offering cash back by big-name brands. www.coff.uk/banks @cashoff_uk Lina Perez, Billy Leung

Pretending it is a husband and wife demo. Funny and unusual for a Finovate demo. Demoing mobile banking app which has smart capability. For example, it reminded them that it was time to purchase food for their dog. The app realized they were traveling (for finovate) and needed to purchase the dog food before traveling. Second part of the demo rewards based/loyalty. User goes to Walgreens and registers the retail store in app. Then you can view items available for cash back. Cashoff integrated with global brands. Starting off the morning with lots of demos expanding the ability of the mobile banking app. ^KT

This banking app provides functions that include cashback and tailored smart advice. Very interesting to see what is coming to the mobile banking app. Mobile, not just for checking your balances any more? There are behavioral cues buried deep in the transactional data. If your bank can surface the insights, you can capture new opportunities. A key pillar of this offering is cashback, which does have an impact on consumers. This is a white-label service available to any bank. ^SR

09:23 am

Namaste Credit

Namaste Credit’s automated credit assessment memo tool improves SME application review time and accuracy using image enhancement, OCR and advanced analytics.

www.namastecredit.com Lucas Bianchi, Gaurav Anand

Namaste Credit sources borrowers and they also have a large numbers of lenders (40) on application. They provide the information to the lenders in the format preferred. Synthesise and perform efficiency on documents. Uses AI to identify correct images to create the credit assessment memo. Takes a picture of documents and can get 99% accuracy in the data. Developed an APK that can be used on any modern mobile in India. Once run the OCR, it will clean up the minor issues and the data is very clean. Showing reporting/analytics in excel. ^KT

SME Lending for the Indian marketplace. Showing a document collection service via a mobile app. Uses video to capture a bank statement via AI processing to improve results. This image helps drive OCR accuracy in the 90%+ accuracy rate. The OCR processed file gets analyzed in Microsoft Excel. Some data gets categorized via the tool. Efficiency gains in getting and processing paper records that are used in the lending review process. ^DG

With small business, there is a tremendous need for access to capital. And of course, SMB lending has been a huge focus for fintech. But, out in the field, it can be difficult to gather the documentation a lender needs to evaluate the application. While this is true everywhere, this is a particular challenge in a market like India. Namaste Credit is focused on this documentation challenge, as a way to remove friction from the lending process using image recognition and OCR. ^SR

09:15 am

MuniRisk

MuniRisk solves information fragmentation for municipal market participants.

www.munirisk.com @MuniRiskLTD James Frischling, Joshua Noble

www.munirisk.com @MuniRiskLTD James Frischling, Joshua Noble

The municipal bond market has always been pretty low on the radar for most firms. Unsung heroes? Cash cow? Craving attention? Now matter how you describe it, this asset class don’t get no respect. MuniRisk is exclusive to the Bloomberg terminal, so that gives you an idea of the target audience. This is a platform for due diligence and research about muni issuers. The product is addressing the time-intensive process of gathering background data on muni bonds. ^SR

Trying to be a big-data source for the Muni market. ^DG

This is not your parent’s Muni Market. Currently lots of losses because of failure in the Muni Market. Showing application on bloomberg terminal. Can view your portfolio by state or via heatmap features. Basically its an efficiency tool for your employees to focus on high value work. ^KT

09:08 am

Tinkoff Bank

Tinkoff Bank’s “Stories” feature delivers best targeted offers and increases transactional activity and financial awareness for customers.

www.tinkoff.ru/eng @tinkoff_bank Maxim Yevdokimov, Darya Ermolina

Largest independent purely online bank in the world. Demo mainly showing lifestyle integration in the mobile banking app.

In app demo: reviewing weekly spending compared to previous week. Also has lifestyle where their are movie options and the user can purchase ticket to cinema in the app. It also has the ability to view the trailer and can purchase movie tickets in the banking app. Same mechanics work with concerts, sports, etc. Also have a fashion section where users can find clothing as well as charity options and set automatic donations. They have seen success with their lifestyle updates and stats across their implementation including movie booking volumes doubling every week. ^KT

This is a digital bank based in Russia and today they are demoing their mobile banking offering. The mobile app contains targeted offers, lifestyle guidance, financial education, and information on functions and services. The lifestyle info includes the latest movies opening that week. You can browse films and buy tickets via the app. This functionality includes restaurants, events, concerts, and more. Right in the app they also share fashion info & ecommerce. The app has 260 screens! So info on app functionality is also a part. This is much more than a typical mobile banking app. I really think this focus on lifestyle is the wave of the future, and it is very well executed here. ^SR

Would bank customers want lifestyle products and services inside their mobile banking app? Tinkoff’s data shows that they do and it drives engagement with the mobile banking app and the brand. ^DG

08:47 am

It’s 5 minutes to show time!

Stop by the front row on a break and say “Hello” if you are here and would like to meet.

William

William Mills III, Chief Executive Officer of William Mills Agency is live blogging today at FinovateSpring 2018. He has more than 34 years of experience in financial technology and is a recognized leader in financial and technology marketing. He has personally advised more than 300 chief executives on marketing strategy, business development, mergers and acquisitions, company branding and public relations. You can contact him via email at william@williammills.com or on Twitter @williamemills.

K.T. Mills-Grimes, marketing director of William Mills Agency, is live blogging today at FinovateFall 2018. She is an experienced marketing manager with a demonstrated history of working in the public relations and communications industry. She is skilled in Search Engine Optimization (SEO), HubSpot, WordPress, Strategic Brand Development, and Lead Generation. You can contact her via email at kt@williammills.com or on Twitter @wmakt

Steven J. Ramirez is CEO of Beyond the Arc, Inc. Harnessing data science and deep marketing expertise, he and his team deliver analytics-driven Customer Experience solutions. Their work includes strategic initiatives at a Top 5 US bank where they directly improved Customer Experience through communications. Helping financial service clients create rapid wins through intensive data strategy and improved customer engagement is their specialty. For more information about Beyond the Arc visit beyondthearc.com, call 1-877-676-3743, or email web@beyondthearc.net. Insights on social media, financial services and more are shared on their blog, or follow them on Twitter at @beyondthearc. ^SR

Steven J. Ramirez is CEO of Beyond the Arc, Inc. Harnessing data science and deep marketing expertise, he and his team deliver analytics-driven Customer Experience solutions. Their work includes strategic initiatives at a Top 5 US bank where they directly improved Customer Experience through communications. Helping financial service clients create rapid wins through intensive data strategy and improved customer engagement is their specialty. For more information about Beyond the Arc visit beyondthearc.com, call 1-877-676-3743, or email web@beyondthearc.net. Insights on social media, financial services and more are shared on their blog, or follow them on Twitter at @beyondthearc. ^SR