04:51 pm

Well, we’ve wrapped up the demos for day one. Please check back tomorrow morning around 8:45am for the group of great demos from Finovate Fall NYC 2018.

William Mills Agency is North America’s largest PR and Marketing agency in the financial industry with more than 70 clients. If you would like to learn more contact Ms. Heather Sugg at heather@williammills.com or myself at william@williammills.com. We are both at the conference here in New York. We look forward to hearing from you.

William

04:46 pm

Crypterium

Crypterium

Crypterium’s mobile app solves the challenges of using cryptocurrencies for payments for the millions of people across the globe who recognize the advantages of cryptocurrencies over fiat money.

www.crypterium.com | @crypterium | Marc O’Brien, Austin Kimm

Crypto assets are going mainstream. Want to make crypto as easy to spend as cash anywhere in the world. Demo: Sending crypto through a phone number as opposed to that really long crypto identification number. Then the receiver gets a text message within seconds of crypto.

Also can send Kenya shillings via phone number. Also showing the ability to pay bills or send money to international bank accounts in Australia and in Europe. Actually sending bitcoin and not euros. But the receiver will receive it as euros. “I sent crypto and he received Euro.” ^KT

04:40 pm

Meniga

Meniga

Meniga targets lack of customer engagement and loyalty and uses internal and 3rd party data to drastically improve the digital banking user experience for bank and financial institution customers worldwide.

www.meniga.com | @meniga | Finnur Magnusson, Mark Nicholson, Isabel Moratiel

Customer on stage (Tangerine) with Meniga. That is a good call. To all other finovate presenters, bringing a customer on stage helps immensely. Meniga has been to 8 Finovates in Europe but first time in New York. Demoing 2 apps on same API.

Demo: within Tangerine’s app and introducing goals (long-term financial planning). Recommends the right goal for the right client at the right time. (Things like an emergency fund.)

Co-innovation with their customers. Go beyond traditional banking. Called “Recipes”, things like, if sports team wins, transfer or 0 to savings. Or every time you that you complete a bike ride, save up for that bike you want. Cute concept. ^KT

04:32 pm

ITSCREDIT

ITSCREDIT

ITSCREDIT’s Instant Credit Express solution creates new payment methods with better conditions for both customers and non-customers of financial institutions.

www.itscredit.com | @ITSCREDIT_SA | Sara Martins, Cristovao Morgado

Credit Calculator to take out a loan for a trip to India for ,200. Then sign into bank that will provide information within app. Then loan was approved and trip booked.

I’m a little distracted by the loan itself. Do people really take out loans for 2 years for a vacation?

Basically customer is their own loan manager and doesn’t have to call in to renegotiate their loans. ^KT

04:25 pm

Orion

Orion

Orion’s proprietary data validation tool solves systemic obstacles within the fintech ecosystem by handling dual functionalities across both data integration and validation requirements in one fell swoop.

www.orioninc.com | @orionsiofficial | Sachin Sinha

Demoing a data validation tool. Fintegrate is an intelligent gatekeeper for all your integrations.

In Fintech we have so many integrations there is now a portal for all of your integrations. SMH. Probably necessary to validate your data, but still. No wonder banks feel overwhelmed. ^KT

04:18 pm

Prisma Campaigns

Prisma Campaigns

Prisma Campaigns’ omnichannel marketing campaigns orchestrator uses machine learning to deliver real time segmented and personalized offers and solve cross-selling challenges on digital and non digital channels for financial institutions of all types and sizes.

www.prismacampaigns.com | @PrismaCampaigns | Felipe Gil, Ana Ines Echavarren

Orchestrate omni-channel campaigns.

Implementing Marketing Campaigns in a single platform. Can see what campaigns were shown the customers. Once a customer is interested or clicks a link, you can see the next assets that will be shown to them. Like a welcome page and form submissions, etc.

For the bank employee, the platform has drag and drop capability and easy to use and sleek interface for the backend. A lot of these fintech platforms look like HubSpot these days. Platform is integrated with CRMs and database and ID providers that also demo at Finovate. ^KT

Prisma Campaigns provides a platform for full-on integrated marketing with highly personalized offers. ^SR

BlueRush

BlueRush

BlueRush’s DigitalReach software creates and distributes interactive and personalized digital experiences to improve engagement and conversion rates for advisors (wealth, insurance, and mortgage).

www.bluerush.com | @bluerushdm | Larry Lubin, Len Smofsky

Demonstrating IndiVideo. Okay so video has entered the show now.

Live on TDs website with mortgage affordability calculator – Form is live on website. Like most calculators it has limited features on conversion. On the results page, it is up to the customer to figure what the results mean.

They added a personalized a video to understand the results. Ohhh. personalized video. I like it! That is slick. Those who viewed this video converted at a 40% increase compared to those who did not. IndiVideo can also be applied to Chat where ask the consumer a variety of questions. Based on their responses, a video is created. Adds a visual experience to the chat medium. Interactive, personalized and visually appealing. Best in show vote for me. ^KT

Personalized information translated into a personalized video. Can be used in website or incorporated into the leadgen process. Video is a high-impact way to engage customers. To me, the personalization is good, but still very static. With technology today, I’d like to have that personal content actually spoken, not just appearing on screen. But don’t get me wrong, this is a strong solution for adding a personal touch, at scale. The chatbot demo does show full interactive content, this is excellent! ^SR

4:03 pm

ID R&D

ID R&D’s biometric authentication solutions use scientific breakthroughs, proprietary research and frictionless UX.

www.idrnd.net | @ID_RnD | Alexey Khitrov

Voice has entered the show. Using voice authorization in authentication of the bank bot to ask when the consumer would like to know their bank balance. Can’t spoof the system with recording of the voice. Brings an extra layer of security to mobile and web login while simplifying the user experience. ^KT

You may have been a customer for years, but your bank is still likely to ask you very detailed questions to confirm it is really you. These processes are cumbersome and invasive, and in many cases, still not all that secure. Biometrics have a lot of potential in this area. This company allows you to use biometrics for chatbots, voice systems, and virtual assistants. It makes these solutions more secure, without all of the invasive questions. The company has voice biometrics, as well as other means. ^SR

3:51 pm

ecosystem.Ai

ecosystem.Ai

ecosystem.Ai’s Computational Social Science Platform uses a Client Pulse Responder to solve financial behavior analytics for transaction clients.

www.ecosystem.ai | Jay van Zyl, Roger Milligan

Customer behavior: it’s tough to predict, but oh so critical. This is really the promise of AI as it applies to banking. The company is applying machine learning best practices in their workbench. This is one of the first companies to talk about how to actually work with the data. The workbench allows users to choose from a number of algorithms. It is something that a smart data analyst could use, and you don’t need to be a PhD data scientist. Under the hood, it looks cleans and simple, but still very robust. ^SR

Platform supports all the major machine learning tools but they simplified the use of it by taking away the complexity. Bring all of these technologies together. Build predictions to get a spatial view and engage with your clients in different ways. In Workbench can eyeball the results to see if predictions were accurate or not with visualizations of client spend and accuracy. Also have geospatial view of transactions. ^KT

03:45 pm

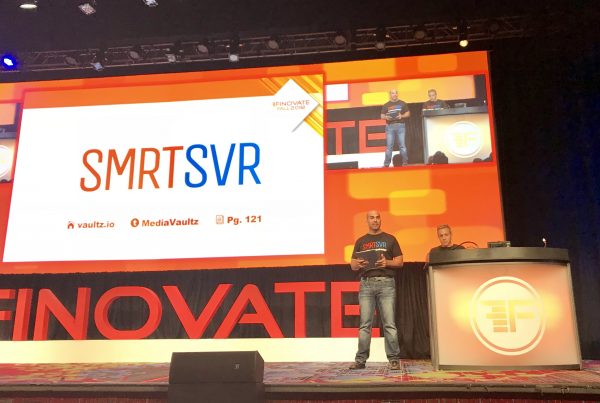

VAULTZ

VAULTZ

Vaultz is helping the gig economy worker with a mobile application for accurate real time estimation and savings of taxes.

www.vaultz.io | @mediavaultz | Rick Gonzalez, Taylor Gonzalez, Matt Armstead

SMRTSVR

Gives self employed workers the same experience with taxes that W2 users have always enjoyed. Saving for taxes based on projected income based on a variety of employers paying user. Monitors income and provides recommendations for taxes and amount to put away. Also takes a look at expenses. Uses Digital Banking Infrasturture to connect to his core and smrtsvr tax savings account. ^KT

Seems like almost everyone in San Francisco is in the Gig Economy; everybody’s got a side hussle. That’s a nightmare for managing taxes. SMRTSVR provides the kinds of services that W-2 employees take for granted. They need to save for the taxes based on projected, and very volatile, income. Everytime you receive a payment, your projections are updated. The system tracks federal and state projections, including estimated payments. Users can actually pay the IRS from the app. This is great! There is a linked savings account to litterally put money aside for taxes. ^SR

Spreedly

Spreedly

Spreedly’s single API connects into a complete, flexible payments infrastructure that supports new business models and new markets.

www.spreedly.com | @spreedly | Justin Benson, Daniel Wideman, Peter Mollins

Pitch: Online Payments – Last Payments API that you will ever need. Superior Consumer Experience and frictionless payments. Our goal is to interject flexibility into payments structure. Based in North Carolina.

Demoing of Supreme Golf Application where customers can look at available tee times. (For hundreds of courses) If you are making a purchase, you can do so without leaving the screen. Each of the courses have different payment processors but the system can do it all on screen and directly from their website. ^KT

This is a payments API, and the company is based in North Carolina. Their product is geared to companies that need flexible, dynamic, payment infrastructure. They are an alternative to the PayPal or Square’s of the world. Merchants get more flexibility to connect to a range of payment gateways owned by corporate partners in the ecosystem. ^SR

02:39 pm

We are taking a short break. If you would like to visit with me, KT or we are on the front row for the next two days. Heather Sugg from WMA is also at Finovate. Feel free to shoot me an email at william@williammills.com.

See you at 3:25pm EST

02:37 pm

ETFLogic

ETFLogic’s “Quant-in-a-Box” Software Solution solves questions around the liquidity and risk of ETFs using Quant Tools and Analytics that traditionally have been difficult to understand or calculate.

@ETFLogic | www.etflogic.io | Emil Tarazi

Co-founder Emil and Lindsey from sales doing the demo. Exchange Traded Funds are booming. Passive investing is expected to exceed active investors. This seems to be a very niche platform; it seems to help the ETF providers to better diversify ETF’s. It seems like a good, functional, working platform. At the same time, this “appears” to be a VERY small company. I would have liked to hear the presenters speak of their experiences and why they are uniquely qualified to create, market and sell their platform and speak about real life uses and clients using it today. They have 12 clients at this time. ^WM

02:29 pm

Enova Decisions

Enova Decisions has solved the “cold start” problem in algorithmic decision making for businesses entering new markets with digital decisioning technology, machine learning, big data, business rules management and optimization.

@EnovaDecisions | www.enovadecisions.com

I haven’t found any VC info on this Chicago-based organization. I believe their offering leverages AI and big data tools to help FI’s build better rules to enable loans that might not have been normally been possible. Showing sample loan origination process/workflow. I like their positioning statement: “Data to Analytics to Action.” It seems to me many of business processes used at FI’s are done because “that’s the way we’ve always done it.” These folks have a good approach. ^WM

02:23 pm

Averon

Averon

Averon’s login solution solves the lengthy, difficult (and oftentimes frustrating) login process for the financial community (all areas).

www.averon.com | Tom Green, Christian Kendall

“SMS Codes are broken!” Instagram was hacked through SMS. “We are here to prevent these type of data breaches for FI’s and FinTechs. This seems like it’s going to be a new approach. “Magic Login” is their demo. Showing right side – traditional username and password. On left side of screen is a QR login (though agreements with mobile carrier networks). Will use camera app to capture QR code and it works. It works on native camera apps on phone. It looks REALLY cool but do you have to use a mobile phone AND a computer or tablet? I’ll have to learn more. Great idea. ^WM

02:18 pm

Tolerisk

Tolerisk

Tolerisk’s SaaS tool solves the problem of weak, one-dimensional risk tolerance assessments for investment advisors.

@Tolerisk | www.tolerisk.com | Mark Friedenthal, Ryan Wheeler

Digital Onboarding

Digital Onboarding’s SaaS platform uses guided digital journeys, SMS reminders, and machine learning algorithms to remedy poor customer/member activation rates for banks and credit unions.

@digionboarding www.digitalonboarding.com | Ted Brown, Jonathan Crossman

I believe I saw this Boston-based company present last year and liked what they had to say. I checked on what they have been up to and while still a small company seem to be adding bank clients. Here is part of some news about a new client: Mariner’s Bank, a US-based independent community bank, has selected Digital Onboarding, a Software-as-Service (SaaS) technology company, for its account activation platform, to simplify the onboarding process for new customers through its process automation. “Earn Without Effort” A.I. Marketing Assistant E.W.E. – showing how a AI can use recommendations to better improve account and new product sales. ^WM

Ocrolus

Ocrolus

Ocrolus’ underwriting AI uses human empowered automation to help alternative lenders solve issues of human variation and inefficiency.

www.ocrolus.com | Sam Bobley, Kevin Bailey

This New York-based company has raised almost million in VC. From Crunchbase: Ocrolus is a venture-backed FinTech company that uses Artificial Intelligence and crowdsourcing to automate financial review processes. The Company transforms e-statements, scans, and cell phone images, regardless of quality, into 99+% accurate digital data.

This is a new kind of approach. There have been a number loan origination platforms here, document scanning/OCR and more. This is seems to integrate greater intelligence in the lending documents for speed and quality. Good job! ^WM

01:56 pm

Salemove

Salemove improves customer engagement and experience using instant live video chat and guided browsing with no downloads and no installations required.

www.salemove.com | @salemove | Dan Michaeli, Justin DiPietro

I’ve seen these folks at Finovate several times before and have always been impressed. NY-based Salemove has raised at least million in VC. 1) Human, 2) Human and AI and 3) Just AI interaction demos. Showing mobile app looking in Safari with live video and cobrowsing. Can be integrated with any mobile app. Very cool as always. Now showing AI with IBM Watson. “How much insurance should I buy?” Now showing the creation of the bot with AWS. VERY easy to create two micro bots. Now attaching these bots to customer communications.

2) Human + AI – the insurance agent is receiving the chat communication. The bot gives the right answer before the agent has to do anything 3) Pure AI example – direct question from customer to bot.

If most questions can be answered better and faster with AI this seems the way to go. I like how it’s human AND AI – not just one or another. ^WM

01:47 pm

Paper.id

Paper.id

Paper.id’s automated invoice financing system helps SMEs get access to credit when they have a limited number of tangible assets that can be used as collateral.

www.paper.id | Jeremy Limman, Yosia Sugialam

4 out of 5 SME’s are using paper/manual processes for invoices in Indonesia. Showing invoicing/FI platform for SME’s and their FI’s. This makes it hard for SME’s in that country to have good documentation to get a loan. From their web site: Up to now, Paper.id has thousands of users who have sent more than 30,000 invoices digitally.

This has a nice UI and seems like it works pretty good. They haven’t shown it yet but I would hope they would have interfaces with accounting systems like QuickBooks. ^WM

01:41 pm

ING Bank

ING Bank’s Invoice Financing solves the challenge of irregular liquidity gaps for entrepreneurs and SMEs using a quick and self-explanatory online platform.

En.ingbank.pl | Ewa Szerszen, Maciej Bukowiec

ING Bank from Poland has had a good reputation especially related to innovation. ING INVOICE FINANCING seems to be the focus of their demo today; is this a personal factoring-type service? It may be for SMB’s. We are about to find out. Showing OCR capture of an invoice for ,000. It LOOKS like a quick and easy way for SMB’s to get advances on invoices. The platform looks cool but I think they should have been more clear on who their target audience is.

^WM

The demo team is from ING in Poland. This is a small business product that helps growth companies get financing for their invoices. With your smartphone, you snap a pic of your invoice and it is entered into the system and pre-populates. They are willing to advance up to 100% of invoice, and you see upfront the cost of the short term financing. With a minimal amount of information, ING has made this transaction simple for the small business. You don’t have to be an ING customer, and cash can be funded within 24 hours.^SR

01:35 pm

iGTB

iGTB’s “Contextual Banking Experience” targets customer dissatisfaction with the current, traditional corporate banking experience using APIs, AI, machine learning, “best-next action” recommendations and “best next offer” point-of-need bank product offerings

www.igtb.com | @i_GTB | Herber de Ruijter, Mike Rayfield

This looks to be a UK-tech Fintech provider successful in a number in a number of countries. I believe CIBC is a client as well as Banco Santander. Looks like an emphasis on corporate banking. Showing nice demo that is seems device agnostic; I can’t tell if it’s on a computer or tablet. Nice UI. Showing connection with Quickbooks. Since INFORMA acquired Finovate we’ve seen a greater number of organizations based outside the United States. I don’t think I’ve seen this company before and they seem like they have a pretty cool platform. Good job. ^WM

Corporate banking hasn’t fully been able to take advantage of technology innovation. iGTB is poised to change that. Corporate users can access new data and analytics to improve their operating budgets and cashflow forecasts. With API’s, they can integrate with platforms like Quickbooks. The contextual banking program can make recommendations to corporate treasury managers. They can use invoices to scrape data and import if for a number of different use cases. This is a white label service that can be offered by banks to their corporate clients. They believe this can enable self-service offerings for corporate customers. ^SR

12:11 pm

Well, it’s time for a lunch break. Please come back at 1:20pm for our next round of demos today!

WM

So we’re back for the afternoon session at Day 1 of Finovate. So what were the most important keywords so far?

- data

- machine learning

- customer experience

- customer

We’ll see if any additional trends emerge for the upcoming demos! ^SR

12:09 pm

Tala Security

Tala Security

Tala Security targets advanced security attacks against web apps as well as PC and mobile web users.

www.talasecurity.io Aanand Krishnan, Siddhesh Yawalkar

I don’t know these folks but I”m sure their service will be popular. Targeted attacks are such as hassle now it’s unbelievable. “We are focused on the good guys – your customers.” (As opposed to keeping out the bad guys. Showing cool demo that shows how a site can have fake ads inserted in the web browsing. Showing how a bit coining mining script is using up bandwidth. Interesting approach. Good job! ^WM

Digital banking has done a good job of keeping the bad guys out. But, it has often come at the cost of customers and their experience. One thing that impacts digital customers is pop-ups (and malicious code). Compromised javascript is often a culprit. Data theft and client-side malware happens on the customer’s device. How do you protect them? Tala creates a security policy and is installed on the server. ^SR

12:03 pm

![]() Ninth Wave

Ninth Wave

![]() Ninth Wave has developed the next generation of data aggregation to solve the security, ownership, transparency and data management challenges of open banking.

Ninth Wave has developed the next generation of data aggregation to solve the security, ownership, transparency and data management challenges of open banking.

@wave_ninth | www.ninth-wave.com | George Anserson, Jack Cassaro, Paul Allen

Founder/CEO of Ninth Wave speaking – sponsor of WIFI – thank you. “Put security, privacy and control in the hands of the customer and their FI.” Good use of humor, nice job. “Why would you give your credentials to some unknown Fintech company?” Browser-based app, platform, list of certified Fintech – which have to be sponsored by FI’s.

These folks were part of EEI and were launched today here at Finovate. From their press release: EEI will be launching a new software company, named Ninth Wave, and its advanced financial data platform that delivers the only universal data supply chain for financial institutions and Fintech breakthroughs. Built from the ground up for the world’s largest Financial Institutions, the Ninth Wave Platform delivers unparalleled data delivery, integration, and aggregation to meet and exceed compliance and security standards while enabling developers to deliver astonishing innovation.

^WM

As customers, why do we give our credentials to 3rd parties when we don’t know if we can fully trust their ability to protect our data? There’s a need for secure data sharing between users, fintech, and FIs. Ninth Wave maintains a platform of about 100 fintech companies, eliminating the need for ad-hoc point-to-point connections. As the bank or credit union, you can restrict which accounts are available to aggregation.

We’re seeing an emerging trend here at Finovate with a focus on APIs. Lot of discussion about integrating data and systems. The long awaited promise of “open banking” and “banking as a platform” seems to really be taking shape. ^SR

11:55 am

SecuredTouch

SecuredTouch

SecuredTouch balances security and user experience by using behavior biometrics for authentication and fraud detection.

www.securedtouch.com | @Secured_Touch Mark | Freeman, Tal Cohen

Very interesting authentication solution. The demo is going well. Can tell the difference between a user and bot by knowing the difference between the behavior between a user and a bot. “Fight Fraudsters. Not Customers.” Very cool.

^WM

Fraudsters are getting more sophisticated. Biometrics is one way to up your game in fraud prevention. Bots are used to commit fraud, acquiring compromised from the dark web. With credential stuffing, an automated bot tries lots of sites and passwords. But these bots don’t “look” like a human in terms of inputting data. SecuredTouch looks at over 100 factors to identify these fake devices. ^SR

11:51 am

Systelos

Systelos

Systelos’ discovery and collaboration platform eases the friction in exchanging value between financial advisors and their clients.

www.mysystelos.com | Jad Chehlawi, Arsene Toumani

Here in New York (vs. California) we see more capital market solutions than in other Finovate cities. Partner came from wealth management background. Showing investing platform – web based – with nice graphics that shows the investor’s portfolio. ^WM

Wealth management is rooted in history and tradition. That’s fine, up to a point. But it does not equip the sector to compete with the next generation of clients. Technology has the potential to help move this business into the modern era. Systelos is a technology that helps increase the value of human advice. It provides context about clients: client behavior and a holistic view of their financial situation. This has been built to address today’s wealth management marketplace: changing client expectations, shrinking margins, and high bar of compliance. ^SR

11:42 am

Cloud Lending Solutions

Cloud Lending Solutions

Cloud Lending Solutions’ configurable digital engagement platform allows financial institutions to provide online experiences to their borrowers without writing any code.

www.cloudlendinginc.com | @cloudlending | Taylor Adkins

I’m interested in this one. Cloud. Lending. Solutions. I think that’s where it’s going. It appears they were bought by Q2 in the past month or so. Q2 started out as an online banking tech company, then mobile and since they have gone public have acquired several companies to round out their offerings. Showing demo of the borrower experience through the loan origination process. Showing loan amount, term, rate, APR and what it looks like on the back end. ^WM

FI can accelerate loan origination with 3rd-party data. For example, you can import data from an aggregator. ^SR

11:35 am

![]() Bumped

Bumped

Bumped gives easy access to the stock market for over half the population who doesn’t traditionally invest by allowing them to own the brands they love.

Bumped gives easy access to the stock market for over half the population who doesn’t traditionally invest by allowing them to own the brands they love.

www.bumped.com | @bumped | David Nelsen, Dave Merriwether

“We are making shoppers into shareholders.” Invest in companies based on the companies and products that people buy on their mobile/online spending. This is a pretty cool idea. If these folks find out how much I spend on Apple products and I had used their app I’d probably own millions of Apple stock shares. Link debit or credit cards you use and choose the brands you would like to invest in and what percent of your new investments to go to each brand. It’s TINY investments in each copmany. I.e. .67 investment in Delta based on purchasing patterns. .01216 shares of SPOT – Spotify at .16 total. Now showing sale of these shares. VERY cool idea and demo. Great job. ^WM

Bumped is creating customer loyalty by turning buyers into shareholders. If I think about what I have spent on Apple products, there’s some personal appeal to me! There is an opportunity for deepening the relationship with customers. I am curious about the underlying SEC considerations (yeah, that compliance question rears its ugly head. They’ve created their own broker-dealer. So that leads to a whole set of disclosures. Not sure how those get delivered… ^SR

11:28 am

![]() Adobe

Adobe

Adobe’s integrated solution leverages AI and facial recognition to remove friction from accessing money while improving security for retail banking channel executives.

www.adobe.com | @adobe | Christopher Young, Fernando Takahashi

Did you read Adobe bought MARKETO this week? This is really a game-changer for Adobe. Adobe has been pretty big in Fintech for years and years but most folks don’t think of them as integral for FI’s. This demo is focusing on using their technology using a PIN and facial recognition. Showing how session was denied. Very nice job. ^WM

Adobe has invested heavily in technology to improve customer experience. This latest innovation incorporates image recognition and AI. The system can identify emotion and facial expressions. They have partnered with Microsoft for the latest in AI. ^SR

11:23 am

11:23 am

FI.SPAN

FI.SPAN

FI.SPAN’s cloud-based services management platform uses APIs to connect customers and fintechs to financial institutions in the US and Canada with over bn in assets and significant commercial and business banking.

www.fispan.com | @FI_SPAN | Lisa Shields, Clayton Weir

I’ve met these folks and have been very impressed with them and their technologies. They are now showing the FI.SPAN Wizard. Showing Bank and Quickbooks Connector integration because they have integrations with a wide variety of platforms. Now showing data sharing token creation. Now showing API development portal. “Experts in connecting legacy platforms.” Great job. ^WM

There is often a huge disconnect between banking systems and enterprise ERP and accounting systems. This leads to a lot of re-work and extra effort. This is a platform for data and system integration. The API developer portal is available to banks and external developers. ^SR

11:17 am

Relay

Relay

Relay’s CX Builder leverages the automated creation and delivery of proactive, prescribed digital solutions to solve crucial moments in the customer lifecycle for digital and CX focused leaders in banking and financial services.

www.relaynetwork.com | @relayit | Matt Gillin, Brie Tascione

Customer Experience – CX – is something a lot of FI’s talk about but don’t actually make significant investments in our industry. “We invented the customer feed.” The a custom, private secure feed for a consumer is provided. 50 clients today. “Showing my feed from my bank.” – Full history of every interaction since he opened his bank account. Why a new tool? Adoption and Engagement. Getting ready to show how easy it is to set up. It looks like it’s not a mobile app, but an online experience that looks like a mobile app. Pretty cool. Good job with demo.

It looks like they are Philadelphia-based, have raised .7 million in VC through Series B with 11 to 50 employees (Crunchbase). From their web site: Relay is a technology company that connects businesses and people through a unique private messaging application. Our mission is to create more valuable and lasting customer relationships by changing the way businesses communicate. Millions of people use Relay every month to connect and communicate with businesses within healthcare, financial services, insurance, cable, energy, travel and hospitality, and more.

Headquartered in greater Philadelphia, PA, Relay is backed by NewSpring Capital and First Round Capital.

^WM

Feeds power social media, and news. Relay delivers the customer feed. A private, secure, 1:1 feed for the individual. Why? This helps promote customer lifetime value and customer satisfaction. On a practical level, they hope to keep people from falling out of the application funnel. ^SR

11:02 am

It’s almost time for session two of day one here at Finovate Fall New York. There are a ton of people here today; a well-attended event. WMIII

10:07 am

exagens

exagens

exagens Personal Banker: autonomous digital banking assistant with proven results increasing conversion rates & retention while lowering costs.

www.exagens.com | Michael Stojda + Jorge Campos

Exagens provides individualization within Banking mobile app for the consumer by combining behavioral sciences and technology. Can show recommendations on things that would help the consumer. If you ignore the recommendation the system will identify the behavioral and adjust to suit the preferences of the consumer. With machine learning you can optimize for conversion based on behavioral preferences of your customers. For example, users that recently paid extra fees are less receptive, so you can set the system to limit the messages and customize the message to the customer. ^KT

Relationships are a key part of banking, and always have been. But as we make the transition to digital, how do you maintain that personal touch? Welcome to the idea of a digital personal banking assistant. This agent provides personalized information and advice. Based on analysis of all the customer interactions, the tool can find insights with machine learning. The focus is on improving engagement and conversion over time. ^SR

09:59 am

PasswordPing

PasswordPing

PasswordPing’s compromised credential screening solution uses secure APIs tied to a salted and strongly hashed backend database of billions of compromised credentials from the dark web to stop authorized authentication by cybercriminals.

PasswordPing’s compromised credential screening solution uses secure APIs tied to a salted and strongly hashed backend database of billions of compromised credentials from the dark web to stop authorized authentication by cybercriminals.

www.passwordping.com | @PasswordPing | Michael Greene, Josh Horwitz

Security company. How does someone else’s data breach impact my organization’s security? Password ping – can determine if your username and password has been exposed on the dark web. Once this happens, you can either step up authentication or force password reset. In this implementation they do a shared secret to authenticate the user and reset their password. This seems very interesting. I want to know if my password has ever been exposed to the dark web. ^KT

Seems like we hear about a password compromise almost every week. (Or is it now every day?) With automated tools, even novice hackers can gain access to multiple sites because people reuse their passwords. Password ping turns these tools into a defensive tool. The technology is available to banks as part of their systems and processes to prevent account takeover. ^SR

09:52 am

Billshark

Billshark’s API powers a white-label bill reduction solution for consumers and small businesses.

Billshark’s API powers a white-label bill reduction solution for consumers and small businesses.

www.billshark.com | @realbillshark | Steven McKean, Ivo Parashkevov

Bill reduction platform. Goal is to lower consumer and small business bills. Billshark is a low touch cancelation service. Partner – HiCharlie showing demonstration. App to manage personal finance via text message. For savings, app recommends billshark to find savings via Verizon Wireless bills. Billshark can re-negotiate a reduced fee and billshark will keep you updated on progress of negotiation. Consumer can see all the bills, rent, car payment, hulu. Can cancel hulu outright via billshark. These seems very helpful for the consumer on reducing their bills. Easy to use too. ^KT

Do you have subscriptions that you *meant* to cancel, but never did? The ability to easily cancel subscriptions is a very cool feature. (And yes, if this works, I’ll be a customer!) In the world of SaaS and subscriptions, all of these costs really add up over time. They have an interface in Messaging (via SMS/Text and a partner, Charlie ), so it prompts you to review your existing bills. ^SR

09:45 am

aixigo

aixigo

aixigo’s digital wealth management technology provides high-performance front-office functionality for retail banks, financial advisors, wealth and asset managers via a modular, predefined API-first high performance platform.

www.aixigo.de/en | @aixigo | Mario Alves, Marcus Gründler

Digital wealth platform with an emphasis on high-performance and speed. Reporting and analysis at high velocity. This enables firms to provide portfolio management in an automated way, and at scale. They seek to construct and manage complex algorithm-based investment portfolios. The rebalancing of portfolios, and then executing the orders, is a very difficult computing challenge. The demo illustrated an Alexa integration, likely to be the first of several today! ^ ^SR

Being fast in investments – Analyze, engage and efficient. Aixigo is pushing wealth digitization. Portfolios rebalanced and deliverable to the market 845 portfolios per second. High performance portfolio management. ^KT

09:38 am

Bucket Technologies

Bucket Technologies

Bucket Technologies‘ digitization of coins at the point of sale aims to eliminate the wasteful cycle of physical coins for retailers & cash-paying consumers.

www.buckettechnologies.com | @bucketthechange | Daniel Kam, Daniel Ross

“Your Digital Piggy Bank”

Cash is not dead. The demand for cash has actually increased. Blockchain deployable technology that digitizes coin change. ^WM

Demo: Buying coffee with cash for a .49 cup of coffee. Cashier gives back but have bucketed the change in the POS system. Receipt prints with a QR code with the change. Consumer opens the app on your phone and scans the QR code on the receipt. This is interesting but seems very difficult to get consumer adoption. All adds up and can cash out to gift card, prepaid card or can donate to a charity. Free for both retailer and consumer. ^KT

Your digital piggy bank. This is an app that helps you to easily save your pennies, nickels, and dimes. You scan your purchase receipt, accumulate a bucket balance, and can even cash it out when you hit certain thresholds. It is not a payment platform, more of an incentive program. It is free to both the retailer and the consumer. They are bridging the physical and digital worlds. This one is worth a closer look. ^SR

09:31 am

Launchfire

Launchfire

Launchfire’s game-based platforms motivate and change customer & employee behavior to drive adoption of digital banking products.

Launchfire’s game-based platforms motivate and change customer & employee behavior to drive adoption of digital banking products.

www.launchfire.com | @Launchfire | Romeo Maione

Brining Games to the Banking Office

Discussing Digital Adoption. FI’s struggling to get their tech. Fintech is convenient but change isn’t. Change needs to come from the front line of your bank. ^WM

Centerpiece of their platform – Narrative game where you can get points. Focus on system is learning and can reward users by reading any great content. Make sure bank employees read and interact with all the content. There are quizzes and game based rounds to ensure interaction with content. Used by product owners and business lines within banks. ^KT

LaunchFire is focused on digital adoption, and they are bringing gamification to frontline training. “Game-based learning is the future.” Having worked on many bank training programs, I can tell you it is time for a change! Most bank training is rooted in traditional approaches, and not really aligned to the needs of millennials and GenZ. So, LaunchFire could be on to something here. However, most LMS systems have a huge quantity of existing content. Not sure if you can import content into the platform, as opposed to cut/paste. They say they don’t work with L&D teams, they usually work with product owners. Wonder if that is a strategic mistake? Would really limit the ability of a bank to scale this approach. Launchfire seems like a good fit for quick, one-off, projects. ^SR

09:24 am

NestReady

NestReady

Description: NestReady’s machine learning predictive analytics model gives visibility into the homebuying customer lifecycle for mortgage lenders so that they can analyze their portfolio and take action in a timely manner.

www.nestready.co | @NestReady | Frederick Townes, Marcos Carvalho

Basically bringing Zillow to a Lenders own website so lenders can monitor data. Buyer can search for homes directly on Lender’s website without hopping off to Zillow. Machine Learning throughout to understand what homes borrower is looking at and favoriting. Borrower can connect with lender and realtor at any time with call to actions throughout.

Showing HubSpot Integration! Integrated into Major CRMs. So loan officer can view borrowers data, pages viewed and preferences. ^KT

NestReady is bringing machine learning to the home lending process. They incorporate web browsing, psychographics, and data from lender’s CRM. For example, they have an integration with HubSpot. NestReady provides more info into the customer’s journey. They try to predict intent to close. Can also identify which prospects can be nurtured over time. ^SR

09:16 am

Access Softek

Access Softek

Description: Access Softek uses AI and machine learning to enable financial institutions to combat the growing and evolving risk of fraud.

www.accesssoftek.com | @AccessSoftek | William Raymer

Pitch: First Robo advisor to be seamlessly integrated with any online and mobile banking application. (Not limited to their products) Demo: Easy for the end-user to work with and manage. Demo – moving money from checking to investments. Same logic as moving money from checking to savings so very easy to manage.

On the back end: can target contacts who do not have investment accounts. Easy to make a group and target ads to that group and review analytics on increasing investment accounts. Banner ads are visible in the online portal for contacts within that group. ^KT

Access Softek speaks to the “four pillars of a bank’s digital future.” They have turned their attention to the robo-advisor market. They want to seamlessly integrate their robo into “any online banking platform.” This could be an interesting plug-and-play option for banks and credit unions. However, many of those FIs do not control their core or online bank platform. Access Softek says they have 5 million current customers. ^SR

09:10 am

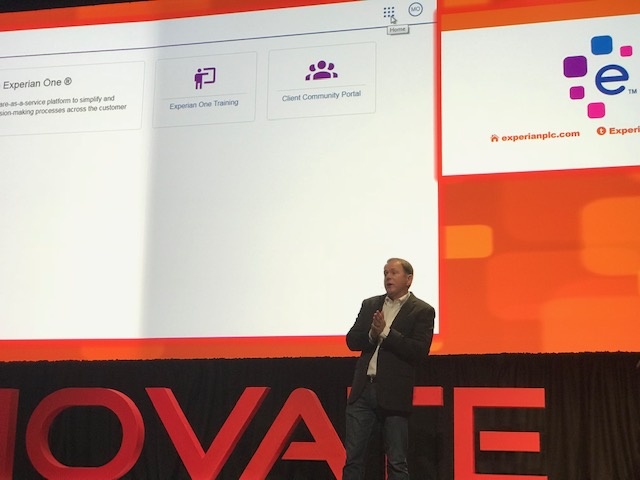

Experian

Description: Experian has developed an enterprise-grade SaaS platform to enable precise customer decisions across the life cycle using a unique blend of best in class data, analytics and decisions strategies.

www.experianplc.com | @Experian | Robert Boxberger, Nada Abubaker

Discussing Division of Decision Analytics. SaaS Based platform. Resides in the cloud. Enabling you to make decisions without a lot of IT resources. Demo – Community bank wanted to grow credit card portfolio. Begin by entering customer application information. Experian Data Quality tool which will auto fill a majority of the information. That’s helpful. Monitors operations and financials to get a good understanding of your approval rates and seasonality. Dashboards give you an overview of approval ratings, average credit line, etc. ^KT

Experian isn’t just a credit bureau anymore. Today’s demo focuses on Decision Analytics, a cloud-based solution for assessing customer applications. There is a business intelligence suite for tracking of metrics relating to your lending process. The service map shows you the status of your various backend systems. Cloud based and SaaS, means you can have sophisticated functionality with a small IT team. ^SR

09:04 am

Nordigen Solutions

Description: Nordigen is building the credit bureau of the future by empowering banks and alternative lenders to use bank account data in credit decisions.

https://nordigen.com/ | Rolands Mesters, Roberts Bernans

Nordigen wants to create the next innovation in the credit experience. Interesting to think about the credit process from a customer-centric perspective, with an “experience.” They work with APIs for aggregation and this enables a customer to complete an application and submit to multiple banks. Demo focused on the income side of the equation, asking if it is regular, what is the source, and if it is stable. The solution is deployable as a web application or as an API (for decision engines). The essence of the tool is to understand transaction data for credit decisioning. ^SR

Building the first global alternative to credit bureaus. Introducing Simple Finance Bank with their live demo. Nordigen reports – viewing income information in the report dashboard to verify income and expenses. Allows banks to get high quality data for automated decision engines. ^KT

08:46 am

Hello! Welcome to FinovateFall 2018. We’re here at the Marriott Marquis in Times Square.

K.T and I are looking forward to watching the future of fintech unfold live on stage. This is either my 21st or 22nd Finovate; I’m not sure. There are a number of great events in FinTech but this one I do my best to attend each year. If you are here at the conference feel free to stop by at the breaks–I’m on the front row. You can also email me at william@williammills.com or reach K.T. at kt@williammills.com. We look forward to speaking with you and sharing all the exciting happenings! ^William

Welcome to FinovateFall 2018! Demos begin in 5 minutes. William, Steven and I will be covering all the presenters today. Stay tuned! ^KT

Fintech has become a global phenomenon as we witness the technology-driven transformation of financial services including banking, payments, insurance, capital markets, and wealth management. Finovate is the place where nearly 1,500 people gather to experience the cutting edge of fintech innovation. We’ll be blogging live September 24 & 25. ^SR

William Mills III, Chief Executive Officer of William Mills Agency is live blogging today at FinovateFall 2017. He has more than 34 years of experience in financial technology and is a recognized leader in financial and technology marketing. He has personally advised more than 300 chief executives on marketing strategy, business development, mergers and acquisitions, company branding and public relations. You can contact him via email at william@williammills.com or on Twitter @williamemills.

Steven J. Ramirez is CEO of Beyond the Arc, Inc. Harnessing data science and deep marketing expertise, he and his team deliver analytics-driven Customer Experience solutions. Their work includes strategic initiatives at a Top 5 US bank where they directly improved Customer Experience through communications. Helping financial service clients create rapid wins through intensive data strategy and improved customer engagement is their specialty. For more information about Beyond the Arc visit beyondthearc.com, call 1-877-676-3743, or email web@beyondthearc.net. Insights on social media, financial services and more are shared on their blog, or follow them on Twitter at@beyondthearc or on Google+ ^SR

Steven J. Ramirez is CEO of Beyond the Arc, Inc. Harnessing data science and deep marketing expertise, he and his team deliver analytics-driven Customer Experience solutions. Their work includes strategic initiatives at a Top 5 US bank where they directly improved Customer Experience through communications. Helping financial service clients create rapid wins through intensive data strategy and improved customer engagement is their specialty. For more information about Beyond the Arc visit beyondthearc.com, call 1-877-676-3743, or email web@beyondthearc.net. Insights on social media, financial services and more are shared on their blog, or follow them on Twitter at@beyondthearc or on Google+ ^SR

K.T. Mills-Grimes is the marketing direcor at William Mills Agency. She manages all digital and social media efforts on behalf of agency clients. K.T. also conducts the planning and day–to–day management of all related marketing activities.

As a HubSpot certified specialist, K.T. oversees all online communications including SEO, website developments and content marketing campaigns. You can reach her via email at kt@williammills.com or on Twitter @wmakt.