William Mills Agency and Beyond the Arc will be live blogging at FinovateSpring. Check back for new updates throughout the day.

William Mills III, Chief Executive Officer of William Mills Agency is live blogging today at Finovate Fall 2016. He has more than 30 years of experience in financial technology and is a recognized leader in financial and technology marketing. He has personally advised more than 300 chief executives on marketing strategy, business development, mergers and acquisitions, company branding and public relations. You can contact him via email at william@williammills.com or on Twitter @williamemills .

William Mills III, Chief Executive Officer of William Mills Agency is live blogging today at Finovate Fall 2016. He has more than 30 years of experience in financial technology and is a recognized leader in financial and technology marketing. He has personally advised more than 300 chief executives on marketing strategy, business development, mergers and acquisitions, company branding and public relations. You can contact him via email at william@williammills.com or on Twitter @williamemills .

Steven J. Ramirez is CEO of Beyond the Arc, Inc. The company helps clients to strengthen customer experience and to deploy data science and Big Data analytics to make marketing and operations more effective. Their social media data mining helps clients improve customer experience across products, channels and touchpoints. For more information about Beyond the Arc visit beyondthearc.com, call 1-877-676-3743, or email web@beyondthearc.net. Insights on social media, financial services and more are shared on their blog, or follow them on Twitter at @beyondthearc or on Google+.

Best Practices for Marketing to Banks

11:38 pm

FinovateSpring 2015 Day 2 Afternoon Video Recap

William Mills, CEO of William Mills Agency and Steven Ramirez, CEO of Beyond the Arc wrap up Finovate with insights on the final presenters such as Malauzai and Trizic and discuss major themes such as wealth management technologies, authentication, text analytics and big data.

10:25 pm

FinovateSpring 2015 Day 2 Morning Video Recap

William Mills, CEO of William Mills Agency and Steven Ramirez, CEO of Beyond the Arc discuss the highlights of the morning and key presenters including Context Relevant, Vanguard, CBW Bank and Slice.

07:40 pm

Folks

It’s now reception/exhibit time and “Best In Show” winners. I’m sorry we’ve had so much tech trouble but these live Finovate Blogs are the highest web traffic days of the year for WMA.

This is not our last post for the day but I wanted to make sure I gave our special thanks to all of the Finovate folks; they did a great job over the past two days. As always my friend Steven Ramirez is a terriiic co-host and this year’s production is indebted to our lead Digital Marketing Consultant, Mrs. K.T. Mills. Thank you K.T.

William

03:04 pm

Malauzai Software

Full disclosure: William Mills Agency is the public relations agency for Maluzai Software.

Robb Gaynor: “Two messages today: big bank stranglehold on tech is gone. Today, we’ll show you watch banking. Second message, who we assembled to demonstrate the benefits.”

There are a whole bunch of folks on stage; more than any other I’ve seen at a Finvoate; perhaps 10 people. Now showing dynamic personalization based on consumer use. Showing Allied Networks PicturePay, Payveris and more.

Danny (co-founder) is now getting ready to show Apple Watch banking. “The estimate is that Apple sold more than 3 million Apple Watches in just a few weeks.” “It’s hard to develop an app for a device which we couldn’t have (just using specs).” I bet this WAS hard. “Same app as the IOS version of the app.” Their FI’s are live TODAY with Apple Watch support. Eight of ten FI’s that were live with Apple Watch were community FI’s live with Malauzai.

Robb Gaynor and Danny Piangerelli plus many more @MalauzaiMonkeys http://malauzai.com/

^WM william@williammills.com

Innovation is no longer the sole territory of the big banks, Malauzai hopes to level the playing field. Their presentation emphasizes the importance of an ecosystem to support community banks.

The demo focused on their new Apple Watch application. The technology builds on the same mobile banking platform currently in use by community banks. This watch application is live! ^SR

Malauzai provides mobile banking for community banks, and it is live in action. This is new for me – mobile banking makes its way to wearables. They are offering “watch banking” (e.g., Apple Watch). You can auto log into your account, see your transaction history, etc. from your watch. Amazing that a community bank can now offer this to customers, TODAY. This company, along with a few others, have some new “live” innovations linked to Apple Watch. Really exciting to see how fast an idea can be developed and then go into production. ^CJ

Persistent Systems

They started by asking the audience, “Have you ever received a gift you didn’t like?” I was the first to raise my hand…

They started by asking the audience, “Have you ever received a gift you didn’t like?” I was the first to raise my hand…

They are presenting Buddy Pay. A platform to text your buddy about buying things. Then you go to the Buddy Shopping App and put in a payment request to the buddy that is online. The buddy can Accept or Decline. It’s a good app for a younger generation (or anyone depending on someone for funds). I see how it’s different from just transferring money online, but I don’t know if it’s really needed?

The presentation went in a different direction than I thought it would. I’d be interested to see how their company grows in the future, but as of now not convinced that this is a useful product. ^CJ

Rakshit (Ray) Bharadwaj, Shriram Natarajan @Persistentsys http://www.persistent.com/

^WM william@williammills.com

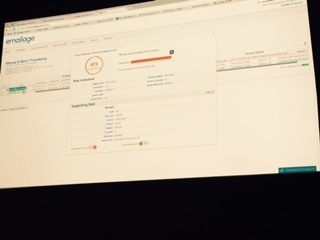

Emailage

The company uses email for risk assessment: based on the address, is this a viable customer, or is it a fraudster? The service provides a risk score and various data elements back to the financial institution. The data is available via a variety of methods including an API. While the technology is interesting, they have to invest in the UI. I know that start-ups are investing in the core technology, but the front end has to be in place! The bar is too high, potential bank buyers can’t get excited if the product doesn’t look like it is ready for market.

The company uses email for risk assessment: based on the address, is this a viable customer, or is it a fraudster? The service provides a risk score and various data elements back to the financial institution. The data is available via a variety of methods including an API. While the technology is interesting, they have to invest in the UI. I know that start-ups are investing in the core technology, but the front end has to be in place! The bar is too high, potential bank buyers can’t get excited if the product doesn’t look like it is ready for market.

This demo needs to start with a basic question: what does email offer for fraud detection,, that other sources of data do not? ^SR

Amador Testa, Jennifer Coughenour

@Emailage https://www.emailage.com/

^WM william@williammills.com

Knox Payments

Are you ever not able to finish a payment because the online application is too complicated? A lot of us have. They mention successful companies like Apple Pay and Venmo, but notes that those apps still depend on a credit cards. Knox Payments presents the idea of making a payment by using your online banking username and password. The same username and password we use everyday to check our balances online. It’s really quick. You pick the account you want to pay with, and that’s it! This is really cool. It’s really fast and it’s safe because “nobody on Earth knows my username or password.” Where can I sign-up? ^CJ

Are you ever not able to finish a payment because the online application is too complicated? A lot of us have. They mention successful companies like Apple Pay and Venmo, but notes that those apps still depend on a credit cards. Knox Payments presents the idea of making a payment by using your online banking username and password. The same username and password we use everyday to check our balances online. It’s really quick. You pick the account you want to pay with, and that’s it! This is really cool. It’s really fast and it’s safe because “nobody on Earth knows my username or password.” Where can I sign-up? ^CJ

“Secure. Easy. Payments.” Process cross-platform payments for less. Pretty slick. I’ll stop by their stand.

Thomas Eide and Julius Gartner

https://knoxpayments.com/

^WM william@williammills.com

NAMU Systems

“I used to be a banker, came to Finovate, quit the bank , started a company and am here today.” Very cool.

“I used to be a banker, came to Finovate, quit the bank , started a company and am here today.” Very cool.

NAMU “Joyful Banking” – Very visual. I would guess this is a mobile app that is complete FI services – banking, payments, bill pay and more. It looks like they are NYC-based. The app is REALLY visual; picture-based. Sort of like buzz feed-type UI. Man, the UI’s here keep getting better and better. Showing live video conferencing with a banker (i.e. FaceTime.) Very cool.

Thomas Ko and Piotr Budzinski @NAMUAPP http://www.namuapp.com/

^WM william@williammills.com

You can pay or transfer money for all of your bills, in just two clicks. You can also use this app to get a quick loan from your bank (e.g., up to at a 4% interest rate). Choose the loan you’re interested in, and the app will call the bank for a live video call. There seem to be a lot of consumer deals incorporated into the product (e.g., 10% off Swedish meatballs at Ikea). I wonder if the deals are just with their app, or if the app is able to search all over the web for deals? They ran out of time, but I am really interested in learning more! ^CJ

Trizic

Trizic is showing a typical bank website. They are playing out what it would be like to open an IRA online. Trizic helps banks keep digital savvy customers. Showing code that they are entering into the site that automatically creates a button. This goes to an investment plan tailored to consumers needs and customer is allowed to open account and invest immediately. How does Trizic handle scale? Trizic Accelerator developed to streamline and automate up to 80% of portfolio management. Set up takes a couple of minutes and manages thousands of accounts. If you want to execute thousands of trades it is a 3-step process. Execute trades as a block and then they are done. Ultimately flexibility is the benefit here.

The company is addressing the need for robo-advisor technology for banks and other financial firms. Each firm can customize the investment offerings to reflect the firm’s unique investment philosophy. An advisor can rebalance risk in the portfolio, with a simple online tool, and apply it to thousands of accounts. For the firm using Trizic’s tool, this platform offers the opportunity to create and actively manage potentially thousands of accounts. They are integrated with TD and other institutional custodians, providing access to a multitude of investments. This could be a way to offer a scalable investment product to a large client base. ^SR

They provide financial advice to their clients. I’ve seen a lot of “robo-advisor” services in the past few years. Looks user-friendly, but not sure how they differ from others offering the same services. ^CJ

CUneXus Solutions

Unveiling point of sale lending solution- can compete with retail. Lender can be present with customer at the point of sale. Generates better customer experience. Demo – Buying a refrigerator. Credit Union sent push notification to customer, saying already pre-approved for 5,000. Customer can then click the notification and goes to Credit Union website. Pre-approved offers on the screen. Demo is selecting instant cash and can adjust price and adjust monthly payment. Integrated in app document and fully compliant e-signature. Quick and easy lending.

Outski

Claim helping customers reach personal financial goals around travel will help them interact with your products like never before – 401 Play – Prioritizing play as an important part of customer’s busy lives. Okay, I am interested. All right, cross-selling angle. Aim to earn back trust of public. 401 play has many features such as saving money, generate trip documents, invite people and a chat that enables engagement, etc.

Customers have busy lives, and they need to play more! So says Finivate presenter Outski. Their product helps consumers reach their personal financial goals for travel. Thier “401 play” offering helps people save, to go on the cool trips they dream about. ^SR

This helps customers meet their travel goals. Something I am always interested in!

The presenter mentions that the millennials don’t trust the financial industry. Is that correct? I’m a millennial and don’t feel that way… I thought that was GenY? Either way I can see millennials going for this. You receive a credit card.

It’s also a social media platform that features a “Trip Feed.” Not sure how this differs from any other travel card, like a Southwest card.

Not totally convinced this is really needed. But they are making it really user-friendly and giving it a fresh face that’s different from just a typical card. But overall, still seems like a typical credit card to me…^CJ

02:40 pm

Corezoid

FOR ENGINEERS

FOR ENGINEERS

Using the theory of finite-state automaton in the operation system corezoid, allows developers to spend more time on what they like to do – CREATION of code.

For this, the cloud corezoid takes all the routine tasks: the code visualization and business-logic collection of statistical data on every status of the automaton removal of the support function through granting access to the process to business-analysts.

More details

FOR MANAGERS

Automate your processes on your own with the help of corezoid.com.

Do you need to compare data in different software packages and then make changes by the results of comparison in the third one?

Do you want to automate the routine processes, but your developers are workloaded and cannot take care of your tasks?

Egor Avetisov and Kristina Chaykovskaya https://www.corezoid.com/

^WM william@williammills.com

Corezoid is helping companies to move business processes to the cloud. Their demo includes hand-drawn pictures of algorithms. I’m thinking that means they are pretty early stage?

The company is partnering with Privat Bank (themselves a Best in Show winner from a previous Finovate.)

The product helps you to map (visualize) business processes, and to some extent, the customer’s journey. There is some functionality to integrate business processes to create a “digital core system.” This company needs to work on simplifying their value proposition. I don’t think I’m following (baffling). ^SR

Partnered with Privat Bank (one of the largest in Europe), their product makes it easy to move processes to the cloud. Their use of dashboards seems to be very user-friendly. It’s an opportunity to have a faster operation, with fewer in-house developers. ^CJ

01:47 pm

PsychSignal

www. Squawkrbox.com Monitor stock trading “chatter” perhaps through social media.

www. Squawkrbox.com Monitor stock trading “chatter” perhaps through social media.

From the company: We set out to quantify real world crowd psychology and in doing so we assembled leading experts in the fields of psychology, engineering and data science. Other sentiment products are generally built upon pre-existing technology or hastily built based on flawed theories. At PsychSignal we have the confidence to compare our live results to real world sentiment surveys and measurements.

They have a an interesting concept but I think they need more VC to really get going as they only have $two-hundred and thirty thousand to date (according to Crunchbase)

James Crane-Baker and Bjorn Simundson @psychsignal https://psychsignal.com/

^WM william@williammills.com

This company uses machine learning to analyze text data from public and private chat rooms. The analyze is fed into a dashboard that tracks the public sentiment (“bullish” or “bearish”) of your portfolio. Sentiment alerts can be sent via email or SMS text. Theoretically, this stream of data (with sentiment analysis) can give professional traders an edge. ^SR

Introducing their product Squawkr-Box. A robot that connects multiple social media platforms for investing purposes (includes public and private chatrooms). It’s able to filter anything you need to know about stocks. Their dashboard looks just like Twitter – which is my way of saying it looks user-friendly and it’s easy-to-understand. I’ve seen some similar products from last year’s Finovate. ^CJ

01:17 pm

Mistral Mobile

“Mistral Mobile was founded by former Nokia Mobile Financial Services leaders who believe in the power of combining financial services and mobility to alter the economics of retail banking and payments while having socio-economic benefits to societies and individuals around the world.”

“Mistral Mobile was founded by former Nokia Mobile Financial Services leaders who believe in the power of combining financial services and mobility to alter the economics of retail banking and payments while having socio-economic benefits to societies and individuals around the world.”

Mistral Mobile’s market-tested mobile front-end solutions are used by retail, issuing and acquiring banks and other financial service providers to offer secure and flexible solutions to rapidly introduce in mobile payments, mobile banking and mobile integrity services to all your their customers, independent of mobile operators and from smart to simple phones.

Remember when the mobile phone carriers controlled the payment/banking infrastructure? Whether it was mFoundry or FireThorn the carries used to control this environment. These folks are ex Nokia folks so I suspect they really know what they are talking about. Nokia used to be the gold standard for phone hardware. I’m looking forward to learning more.

Ludwig Schulze and Paul Yoo @MistralMobile http://mistralmobile.com/

^WM william@williammills.com

They come from Nokia’s mobile payments group. Today they are presenting on mobile security. As a result, the initial disclaimer is that they don’t have a pretty UI. I get it, but I would say that interface is also important for banker-facing, internal, software applications.

The demo is presenting the internal, server-side, technology that is operating behind the scene. There is a rules engine that enables banks to create automated responses. On the front end, the consumer takes an action with their device, on the back end the institution responds. ^SR

Mobile security protecting everything from the hardware, to the software, to the communication channel that passes financial information. They are presenting Maegis, a risk factor analysis. They send possible risk alerts to the customer for them to determine if it’s fraud, and if so, ask them what they want to do. ^CJ

12:48 pm

Bento for Business

Bento is providing a “prepaid MasterCard exclusively for small business.” This gives business owners more complete control over what their employees are spending. This sounds great. It also skips the reimbursement process (e.g., saving receipts and waiting a week) and let’s employees use prepaid cards for gas, travel, etc.

Bento is providing a “prepaid MasterCard exclusively for small business.” This gives business owners more complete control over what their employees are spending. This sounds great. It also skips the reimbursement process (e.g., saving receipts and waiting a week) and let’s employees use prepaid cards for gas, travel, etc.

It appears to be very easy to set up. You can manage the accounts, set a limit per month, week, etc. You can turn a card on and off with the switch of a button. Wow, I’m seeing a lot of potential. This is great for employees as well. Instead of waiting for their employer to reimburse them for the .00 parking lot ticket, they’ll be able to immediately use the funds on their prepaid card. ^CJ

12:46 pm

RAGE Frameworks

Nice demo. From the company.

Nice demo. From the company.

We provide enterprise mission critical Business Process Automation and Big Data solutions and products as a managed service, based on our pioneering and patented technology

Business Process Automation. We are the market leading provider of Business Process Automation solutions; we are successfully delivering on the promise of such technology against the general dissatisfaction with the BPM tools in the market today

Semantic Intelligence. We are pioneering context sensitive semantic intelligence applications for real time interpretation of unstructured [and structured] data, e.g., investment/industry research, enterprise risk management, competitive intelligence, life sciences, publishing, litigation and others

Our solutions are delivering unmatched value to global corporations and helping them with time to market, real time insight and improved efficiencies

Our channel and delivery partner network comprises some of the leading global BPO companies and consulting firms

Aashish Mehta and Nick Adams @RAGE_Frameworks http://www.rageframeworks.com/

^WM

Focused on Big Data Analytics. Talking about a lot of their capabilities (e.g., risk management and investing). Seems like a 7 minute presentation is not quite long enough for them. ^CJ

12:45 pm

CBW Bank

Full disclosure: William Mills Agency is the public relations agency for CBW Bank and Yantra Financial Technologies.

Full disclosure: William Mills Agency is the public relations agency for CBW Bank and Yantra Financial Technologies.

I first was introduced to Suresh about six months ago and without a doubt, whether I worked with Suresh or not I will tell you he is a technology visionary.

“Our journey started six years ago with a small bank in Kansas. Just like rebuilding a classic car, we re-built the bank from scratch. We have the bank account of the future today. Added, speed, intelligence and context. We can do many things, but let’s start with speed.”

Showing browser-based landing page for OneCard which looks fast and easy and can send money worldwide. Now getting ready to show an instant payment to a recipient in India.Now showing intelligent bill payment: your bills are paid automatically IF they are correct. Now showing “context” showing how a bank account can be linked to the “Internet of Things” and in this case connecting to a car. I THINK using this technology a customer can make decisions who can buy fuel for a particular automobile, truck or other vehicle. I’ve NEVER seen anything like this, especially for consumers and SMB’s.

Check on this profile on Suresh in a December issues of THE NEW YORK TIMES.

http://dealbook.nytimes.com/2014/12/13/small-bank-in-kansas-is-a-financial-testing-ground/?_r=0

Suresh Ramamurthi and Randy San Nicolas https://secure.cbwbank.com/Pages/Default.html

You can use this app to send money to an account of your choice (e.g., OneCard account, debit card). The amount is available immediately AND can be transferred from one country to another.

It also provides a real-time risk scoring and risk prevention platform. Use it as a safety-net for fraud, and pay your bills automatically. Provides a piece of mind for all users. ^CJ

12:04 pm

Alpha Payments Cloud

I’m sorry; due to tech issues we were not able to post information on Alpha Payments Cloud. Please check out their web site and we will provide additional information as we can.

I’m sorry; due to tech issues we were not able to post information on Alpha Payments Cloud. Please check out their web site and we will provide additional information as we can.

Oliver Rajic @AlphaPayments http://www.alphapaymentscloud.com/ ^WM

This is a solution for financial institutions to be able to add “plug-and-play” solutions from a number of technology providers . From their website:

The AlphaHub consolidates the payments world onto one platform enabling Banks, Merchants, MSPs and ISOs to access any payment type, any solution provider, anywhere in the World. The AlphaHub covers every payment and transaction related solution stream, simplifying vendor management and introducing a host of new cost and operational optimization tools. ^CJ

11:39 am

LoanNow

Another crowdfunding solution. Like I said, it’s hot. Showing a new group function: GroupSign on computer browser (not a mobile app, yet.)

Another crowdfunding solution. Like I said, it’s hot. Showing a new group function: GroupSign on computer browser (not a mobile app, yet.)

From the company:

LoanNow is proud to set a new standard for the lending industry. We look at the entire person, not just their credit score, with loans tailored to every credit situation.

And we are the only team that allows individuals to take control of their own loan. By meeting a number of achievable goals, you can earn credits that reduce the cost of your loan while you pay it back. Every LoanNow loan features fair and straight-forward terms and support with world-class customer service, including easy-to-use online tools and resources.

Harry Langenberg and Miron Lulic @loannow https://www.loannow.com/

^WM william@williammills.com

Social networks are one of the sources of innovation in consumer lending. LoanNow is essentially a “social credit platform”. Today, LoanNow is presenting their new product, Group-Sign. This is a platform for consumers seeking loans, but they have poor credit and not likely to qualify for traditional lenders. Using this platform they request a “pledge”, instead of a loan. So instead of co-signing, you can ask a friend to pledge an amount of their choice (e.g., 0).

There have been other social credit presenters at Finovate this year. It’s an interesting trend. ^CJ

11:28 am

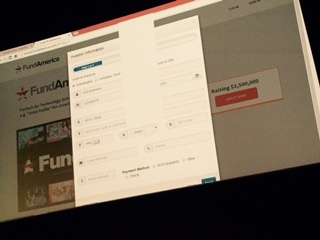

FundAmerica

“Simple, SEC-compliant tools for technology-driven finance” ANOTHER crowd funding/capital raising/SMB (?) and more. This is great; it means folks are investing in new businesses and people have money to invest. Showing demo of sample company raising A round of million.

“Simple, SEC-compliant tools for technology-driven finance” ANOTHER crowd funding/capital raising/SMB (?) and more. This is great; it means folks are investing in new businesses and people have money to invest. Showing demo of sample company raising A round of million.

From the company: Our mission: The enormous opportunity created by the JOBS Act is leading to an explosion of firms emerging to operate funding portals, aka “platforms. “FundAmerica’s mission is to provide FinTech to the crowdfunding industry and deliver the highest value to our customers. Additionally, we plan to expand into other areas of service to the industry.

Have 150 platforms signed up.

Scott Purcell, Scott Anderson and Jonathan Self

@FundAmerica http://www.fundamerica.com/ ^WM william@williammills.com

This is a newer company and they are a crowdfunding platform for large transactions (e.g., twenty thousand). Most crowdfunding platforms tend to be smaller-dollar transactions. Interested to see more from them in the future! ^CJ

11:22 am

Finaeos

“Funding America’s SMBs” “Three steps to Fund Your Business” This is at least the third platform in two days to support SMB funding. Clearly, this is a HUGE sector and I’m not even counting the “instant” funding companies like OnDeck. Based in Victor, BC, Canada – one of my favorite places to visit. Keep an eye on these folks.

“Funding America’s SMBs” “Three steps to Fund Your Business” This is at least the third platform in two days to support SMB funding. Clearly, this is a HUGE sector and I’m not even counting the “instant” funding companies like OnDeck. Based in Victor, BC, Canada – one of my favorite places to visit. Keep an eye on these folks.

Tim Vasko @Finaeos ^WM william@williammills.com

Making things easier for small business has been a theme of Finovate Spring 2015. This offering provides small business solutions to fund a business – focused on small business growth. One interesting feature: a quick and easy way to get incorporated. Customers can build their campaigns, and they can even contact Finaeos partners for a bridge loan. ^CJ

11:15 am

Aurora Financial Systems

Use cell phone to control cards. They are an issuing processor. Interesting; I need to stop by their stand.

Use cell phone to control cards. They are an issuing processor. Interesting; I need to stop by their stand.

From the company:

NOTE

Less complexity,more clarity.

Let’s face it, managing your money can be tough, all the spreadsheets and paperwork can be daunting at best, and suffocating in some cases, but it doesn’t have to be.

Managing your money is straight forward — start by separating your money into three accounts:

Checking

Fixed Costs

These costs are predictable and typically occur on the same day each month — utilities, car payment, rent or mortgage payment, etc.

You can keep using your current checking account to pay these bills. Hopefully you already have bill pay available. If not, you can use the MoneyGram Bill Pay Service.3

NOTE

Day-to-Day Spending

Day-to-day expenses that can fluctuate a bit month-to-month — eating out, groceries, shopping, hobbies, entertainment, gas, etc.

This is where the NOTE Card was born to shine. NOTE has been carefully tuned to deliver the convenience and security you need anywhere – in the store and online.

Scott Stagg and Chris Melendez http://note.cash/

^WM william@williammills.com

This company provides a card processor and program manager in real-time. You can charge a purchase to your card and a message will be sent to your phone asking for you to authorize it. They’ve also created a mobile friendly app called Note. This application turns the authorization app into a decision app. So instead of text asking, “Do you want to authorize this,” it asks the consumer, “5 charged to Gap, which is over budget. Do you want to authorize this transaction?” ^CJ

11:11 am

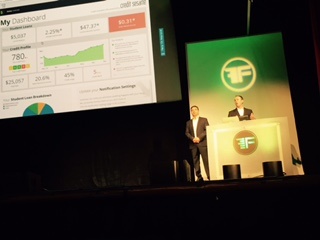

Credit Sesame

Adrian fourth startup. I’ve seen Credit Sesame before and I was impressed last time. Showing SIRI solution. One of the things no one has discussed today which is how much money there is in the credit space. I believe Credit Karma has a valuation more than billion. What I’m trying to ascertain is what’s new this year over past demos.

Adrian fourth startup. I’ve seen Credit Sesame before and I was impressed last time. Showing SIRI solution. One of the things no one has discussed today which is how much money there is in the credit space. I believe Credit Karma has a valuation more than billion. What I’m trying to ascertain is what’s new this year over past demos.

From the company: Our Mission – It’s our mission to be the consumer’s credit and loan expert—finding the best options tailored to you, so you can save money and live richly.

CrunchBase reports that they have raised .4 in VC in four rounds with the most recent being million in Series D in May. NOW SHOWING APPLE WATCH CREDIT REPORT APP. This is a first; I’ve never seen this and it’s only the second Apple Watch (I’ve seen) at Finovate.

Good job.

Adrian Nazari and Jesse Levey @creditsesame http://www.creditsesame.com/

^WM william@williammills.com

They’ve been here before and have grown tremendously since last year. A very cool credit score application. They started by asking Siri, “Siri, what is my credit score?” And Credit Sesame popped up immediately with their credit score, and the last time it was updated.

The platform helps consumers manage credit and loans. After a quick sign-up process, the app shows you not only your credit score, but gives you more information broken down into five different factors. You can also see all of your loans (e.g., mortgages, credit cards). And it even gives you an analysis to help you determine where you’re doing well.

The also have a goal list, which the app monitors and will give you advice to better achieve the goal. Furthermore, it has identity protection.

The company reports many engaged users right now. And they now provide an Apple Watch App! All of the above functionality will send an alert to your watch immediately.

A new tool for millennials to help them monitor their loans etc. They show them their current loans, and provide a “robust planning tool.” Take control of your loans!

This app sounds like it’s combining in a lot of tools some other presenters have demonstrated, all at once. ^CJ

10:40 am

FinovateSpring 2015 Video Interview with Beyond the Arc & CCG Catalyst

Steven Ramirez, CEO of Beyond the Arc and Paul Schaus, President & CEO of CCG Catalyst discuss Finovate day one.

beyondthearc.com/blog/ www.ccg-catalyst.com

10:20 am

break

10:15 am

Slice

Getting ready to show IOS app. I believe Harpinder presented in the past with a previous company. “We have level 3 data” which I assume comes form card data. Showing app call “citi scape” which I’m not sure if they created for CitiBank or are just showing as an example. Showing images, dates, costs and photos of purchases on the phone for a variety of merchants.

Getting ready to show IOS app. I believe Harpinder presented in the past with a previous company. “We have level 3 data” which I assume comes form card data. Showing app call “citi scape” which I’m not sure if they created for CitiBank or are just showing as an example. Showing images, dates, costs and photos of purchases on the phone for a variety of merchants.

Harpinder Singh @HelloSlice https://www.slice.com/ ^WM william@williammills.com

They provide information on the items you purchase, not just the transaction that appears on your statement. Slice uses email to obtain that item-level transaction information. They extract info from receipts in email, and then categorize it.

Slice is a competitor of Shoe Boxed, but Slice has made it clearer why this is a valuable service. Banks are more likely to monetize the customer data they have, with this as a data-enrichment. ^SR

They are asking questions like ,”What did I spend 0.00 on at Target the other day?” They have what they call “level three information.” This information shows exactly what you bought. Also gives you fraud alerts, shows you in what categories you spend money (e.g., travel). You can also give yourself a budget, and the app will send you an alert when you overspend or are close to your goal (e.g., .00 left in the electronics category).

They seem similar to a few other Finovate presenters. ^CJ

10:14 am

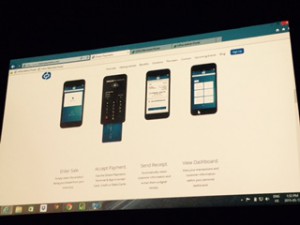

Dream Payments

The offering presented today focuses on payment services for banks and merchants. They’re focused on making things simple. You can tap a card to the smartphone, and the information is entered into the application. For merchants who use the service, they see how their business is going by tracking their sales. The product is transitioning from the magnetic stripe to more sophisticated technology (important for security, usability, and reporting purposes.) ^CJ

10:13 am

Kofax

California-based Kofax has a very good reputation in the industry. Lexmark just bought the company.

California-based Kofax has a very good reputation in the industry. Lexmark just bought the company.

The have not YET gotten to their demo. I think they are having tech issues are we are not seeing anything but hearing about a new authentication process. Now it’s online. Showing pre-qual for pre-paid card. I believe it’s HTML5-based. Showing a mismatch which would streamline consumer experience but still be in compliance with KYC regulations. Geolocation of mobile phone integrated. Showing Kofax Process Designer.

Diane Morgan and Dimitri Snowden @Kofax http://www.kofax.com/

^WM william@williammills.com

An interactive platform for determining risk. This is a way for banks/lenders to provide a quick and easy customer experience when, for example, applying for a new credit card. ^CJ

Kofax is an impressive company, and I’ve enjoyed all of their presentations over the years. Today’s demo is about real-time risk decisioning. They have built on their leading-edge technology for image capture, and expanded into new use cases for onboarding and account opening. I consider them to be a leader in fintech. ^SR

10:03 am

Context Relevant

“We are here to show you what happens when the cost of data science is free.” Decision makers need technology to make the right decisions.”

“We are here to show you what happens when the cost of data science is free.” Decision makers need technology to make the right decisions.”

Folks, I apologize, we are having tech issues as the live blog may be overloaded. Please check out their web site at your convenience. @ContextRelevant http://www.contextrelevant.com/

Divanny Lamas and Konstantin Getmanchuk

^WM william@williammills.com

A machine learning platform to solve challenging use cases such as insider threat protection. All-in-all a fraud prevention platform. A little blown away by their technology. You can monitor fraud all around the world and you’ll receive alerts. The alert shows you how many transactions (e.g., 50), how high the probability of fraud is (e.g., 97%), and the expected losses (e.g., ,349). You could “Take Action,” or, “No action.” You can also look at the database and see if, for example, a person travels often in a certain area and can determine from that if it truly is fraud. ^CJ

Data science is valuable, but can be expensive to execute and scale (all those pesky data scientists!). They provide highly automated machine learning use cases: fraud, insider threats, and more. They are providing a view into their working prototype. The demo discusses tens of millions of transactions per day, monitored in real time. The UI is very nice, but hard to tell what is really happening under the hood. Would definitely like to know more about the actual technology at work here. ^SR

10:03 am

LendKey

Student, Auto and personal loan platform. I think I’ve seen these folks before. Announcing today the “Lendkey Network” which sounds a little bit like LendingTree but with more products. I’m interested in seeing what makes them unique. They are now showing the student loan sample where folks can determine how they can reduce their student loan amount.

Student, Auto and personal loan platform. I think I’ve seen these folks before. Announcing today the “Lendkey Network” which sounds a little bit like LendingTree but with more products. I’m interested in seeing what makes them unique. They are now showing the student loan sample where folks can determine how they can reduce their student loan amount.

Vince Passione and Strati Papageorge @LendKey http://www.lendkey.com/

^WM william@williammills.com

A new service for student loan refinancing. The student can put their information in and see what local lenders can offer. The offers update in real-time, which they say is “critically important.” Seems like this product shines during the application process. Only a few pieces of information is needed making it a quick and easy process. “Shop, customize, and fulfill all from a single site.” ^CJ

10:00 am

Vanguard

Now this is kind of interesting. I don’t recall Vanguard or similar organization presenting at Finovate San Jose, they might have presented in New York. Showing portfolio dashboard using funds visualized in “cubes”. Again, another great use of graphics to demonstrate complex data.

John Buhl and Mike Padilla @Vanguard_Group https://investor.vanguard.com/corporate-portal/

^WM

Their goal is to help investors become more successful, by making better use of available market information. The product emphasizes data visualization, for example, to show how various funds cover different investing strategies. This is a good way to “see” if a particualr fund will enable you to diversify your portfolio. In some cases, adding a fund might actually reduce your diversification, but that wouldn’t be obvious without visualizing the data. ^SR

They help investors make smart funding decisions by providing a diverse portfolio in a easy-to-understand diagram or “cube.” Add funds to your portfolio to see how your portfolio diversifies. Get a close look at what’s really inside your funds. ^CJ

09:51 am

Token

Token

Very successful at past companies. We haven’t seen the demo yet; getting ready to show four things you can do with the technology. Mobile and other services.

“Steve Kirsch and Yobie Benjamin”

^WM william@williammills.com

They are experts in secure funds transfer. Token uses smartphone and other mobile devices for customer authentication and bill pay. Their technology prevents fraudulent transactions if the device is not in the hands of the rightful owner (it uses biometrics as part of the authentication process, the demo used a Fitbit to recognize the user). The technology is based on digital signatures and real-time APIs. ^SR

Fraud prevention and identity authentication software provided to big banks for iPhone and Bill Pay. You have to wear a FitBit to be able to make transactions. So if someone steals your device, they wouldn’t be able to make payments. ^CJ

09:48 am

FinovateSpring 2015 Day 1 Afternoon Recap

William Mills, CEO of William Mills Agency and Steven Ramirez, CEO of Beyond the Arc recap Finovate Spring day one including the advancements of presenting companies Dwolla and Kabbage.

09:36 am

Shoeboxed

I don’t know much about these folks but I like what I see so far. It’s a platform for integrating receipt capture. Man, I’ve tried EVERYTHING to help me with this. Now using Dropbox and Evernote but I need a better automated system. Showing IOS app version.

I think I’ll sign up for this and they are only 3 minutes into their demo.

OK I’ve signed up for their free version. I’ll let you know how it goes. Good presentation.

Tobi Walter and Alex Anderson @Shoeboxed https://www.shoeboxed.com/

^WM william@williammills.com

The company provides functionality for receipt capture. You can sync your bank account and email, and your email populates the data for receipts (like an Amazon purchase). This expense is also automatically categorized. For a bank, you can get the receipts into your banking environment (presumably to obtain more data for analytics). The app also allows user to snap a picture of a receipt to add it. The service reconciles purchases and receipts, which may have some value for fraud protection. The technology is appealing, but I’m not getting the real use cases. Why does a consumer need this feature? Why does a bank need to provide it? ^SR

Financial application, email and mobile receipt management. Receipt capture. Finovate Bank app. Syncs to your email account. You can see a “world of data.” The original receipt etc. Furthermore, the app provides you with alerts such as when that product drops in price. You can take a picture of your receipts, add a note, and can give it a tag such as “reimburse,” and ShoeBoxed will record the receipt by capturing the picture and even uploads the information.

This app also provides fraud prevention. Example, you left your waiter a three tip, but he gave himself a four tip. ShoeBoxed will notify you of this fraud. ^CJ

09:33 am

DriveWealth

DriveWealth

What they do: “U.S. Stock Market, Now for Everyone. Our full-stack platform empowers retail investors worldwide.” Launching new product on partner program; FI’s, tech firms, mobile apps, etc. Offering API’s to their platform. They have raised more than million in Series A funding which I believe came in last week.

Now showing their HTML code so a partner can drop it in to their web site for white label use as I understand. Using BitCoin, SafetyPay from Miami among other providers/platforms for funding mechanisms. Available in four languages. Now showing Chinese version of mobile app.

Michael Fitzgerald and Aric Rosenbaum @DriveWealth https://drivewealth.com/

^WM william@williammills.com

Growth in wealth is coming from emerging markets. They are providing brokerage as a service, targeted at international investors, providing access to U.S. equities. The platform accepts a number of global payment options to fund the account, which can be opened online. They have apps on Apple iOS and Android platforms. The platform is white labeled, so the name of the institution appears on the site and the apps. This offering opens up investing in US stocks to retail investors around the world. ^SR

An full-stack retail investing platform that provides the typical app for orders, trades, and more. They create the widgets that can be embedded in their partners websites: open, fund and trading. I’m interested in learning more. ^CJ

09:14 am

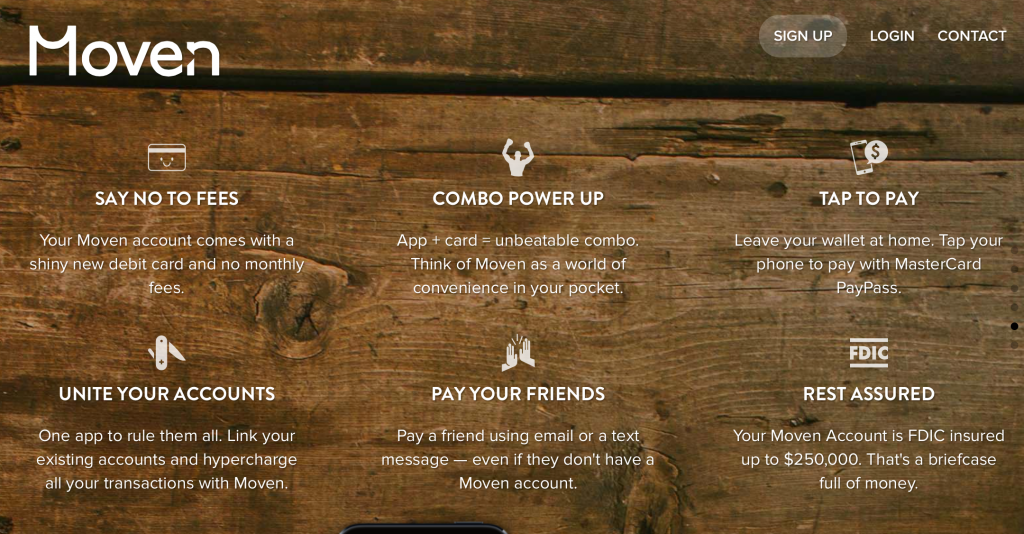

Moven

Who does NOT know Brett King? “We are putting to the end of budgeting and PFM”. Showing IOS app, very clean UI, looks easy to use. I like their slogan: “The debit account that tracks your money for you, instantly” now showing Apple Watch app but it did not work. That’s ok, the Apple Watch is so new I’m not surprised of a challenge. I THINK this was the first time an Apple Watch was shown at Finovate.

Brett King and Alexander Sion @getMoven https://www.moven.com/

Brett King and Alexander Sion @getMoven https://www.moven.com/

^WM william@williammills.com

Moven is a leader in the next generation of digital banking. They are presenting their new app features, with saving and budgeting for consumers. They don’t believe in “goals”, but rather, an evolving “wish list” of things you want to save for. This is the first demo of the day that shows live integration with the Apple Watch. The app show’s consumers the pattern of their spending and saving. Asks consumers: do you really want to spend that money? The idea is based on gamification of saving. They include predictive analytics and geo-location to provide proactive notice to users. “You’re in Trader Joes, you usually spend 0, but you get an app warning: you only have in your account.” ^SR

An app for budgeting. They provide customers with a spending meter to determine your “financial health.” Helps users identify where their spending most of their money. They describe it as a game to save: you create goals and a wish list. The wish list connects to sites such as Pinterest. Now they’ve got my attention! It’s more than just a “saving” platform. You can also payback friends – which you can put on your wish list. That’s the savings part of it. It’s not so much about budgeting anymore, it’s just about saying in the “green.”

They are rolling out to multiple countries and are hoping to have 25 million users soon. ^CJ

09:07 am

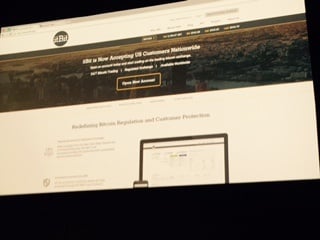

itBit

Launched last week; lots of press; “itBit is a global exchange offering institutional and retail investors a powerful platform to buy and sell bitcoin.”

Launched last week; lots of press; “itBit is a global exchange offering institutional and retail investors a powerful platform to buy and sell bitcoin.”

From their web site: itBit is a global bitcoin exchange offering institutional and retail investors a powerful platform to buy and sell bitcoin.

itBit has taken a uniquely rigorous approach to regulatory compliance by establishing the itBit Trust Company, overseen by the New York State Department of Financial Services. With the trust, itBit is the first and only regulated bitcoin exchange able to accept customers across the United States.

Showing live platform; browser-based. Showing QR code for sending currency. They raised a fair amount of VC; .3 million according to CrunchBase. They said they have raised more than million in VC.

“Modeled on traditional exchanges.” Interesting play; I need to learn more about them. What’s kind of interesting as they are at Finovate Spring; I tend to see these type, NYC-based companies present at Finovate Fall.

@itBit https://www.itbit.com/

^WM william@williammills.com

The company provides a multi-currency platform for bitcoin trading. The company provides a platform for retail and institutional clients. Their vision is bigger than bitcoin, they believe they have a platform for the future of value exchange. ^SR

They had their big U.S. launch last week and they are now open to all U.S. customers. Offer services from global trading desk to tax reporting. Clients can buy small amounts of bitcoin, they can view the total market, and they will receive monthly and quarterly statements. ^CJ

08:43 am

Good morning! We are getting ready to start day two of Finovate Spring 2015.

Good morning! We are getting ready to start day two of Finovate Spring 2015.

If you are here please stop by the front row and say “Hi”.

William Mills

william@williammills.com

The Finovate Spring 2015 team gave a brief update on the funding received by presenting companies. The funding from last year’s 2014 presenters has been strong: 6Million raised, with over 0million raised by the Top 6. The entire alumni base is .4Billion raised for past presenters.^SR

Today we’re joined by Corina Jordan from the Beyond the Arc content team. As some of you may know, Beyond the Arc helps financial institutions and fintech companies develop content marketing strategies, including social media management.