William Mills Agency and Beyond the Arc will be live blogging at FinovateFall 2015. Check back for new updates throughout the day.

William Mills III, Chief Executive Officer of William Mills Agency is live blogging today at Finovate Fall 2013 in New York City. William has more than 30 years of experience in financial technology and is a recognized leader in financial and technology marketing. William has personally advised more than 300 chief executives on marketing strategy, business development, mergers and acquisitions, company branding and public relations. You can contact him via email at william@williammills.com or by twitter @williamemills.

William Mills III, Chief Executive Officer of William Mills Agency is live blogging today at Finovate Fall 2013 in New York City. William has more than 30 years of experience in financial technology and is a recognized leader in financial and technology marketing. William has personally advised more than 300 chief executives on marketing strategy, business development, mergers and acquisitions, company branding and public relations. You can contact him via email at william@williammills.com or by twitter @williamemills.

Want Brand Awareness for your new FinTech Innovation? Click Below.

Steven J. Ramirez is CEO of Beyond the Arc, Inc. Harnessing data science and deep marketing expertise, he and his team deliver analytics-driven Customer Experience solutions. Their work includes strategic initiatives at a Top 5 US bank where they directly improved Customer Experience through communications. Helping financial service clients create rapid wins through intensive data strategy and improved customer engagement is their specialty. For more information about Beyond the Arc visit beyondthearc.com, call 1-877-676-3743, or email web@beyondthearc.net. Insights on social media, financial services and more are shared on their blog, or follow them on Twitter at @beyondthearc or on Google+ ^SR

Steven J. Ramirez is CEO of Beyond the Arc, Inc. Harnessing data science and deep marketing expertise, he and his team deliver analytics-driven Customer Experience solutions. Their work includes strategic initiatives at a Top 5 US bank where they directly improved Customer Experience through communications. Helping financial service clients create rapid wins through intensive data strategy and improved customer engagement is their specialty. For more information about Beyond the Arc visit beyondthearc.com, call 1-877-676-3743, or email web@beyondthearc.net. Insights on social media, financial services and more are shared on their blog, or follow them on Twitter at @beyondthearc or on Google+ ^SR

Twitter: @beyondthearc

K.T. Mills-Grimes is the Digital Marketing Consultant at William Mills Agency. She manages all digital and social media efforts on behalf of agency clients. K.T. also conducts the planning and day–to–day management of all related marketing activities.

K.T. Mills-Grimes is the Digital Marketing Consultant at William Mills Agency. She manages all digital and social media efforts on behalf of agency clients. K.T. also conducts the planning and day–to–day management of all related marketing activities.

As a HubSpot certified specialist, K.T. oversees all online communications including SEO, website developments and content marketing campaigns. You can reach her via email at kt@williammills.com or on Twitter @wmakt.

Download: Content Marketing White Paper

04:39 pm

William Mills, CEO of William Mills Agency and Paul Schaus, President and CEO of CCG Catalyst, reflect on presenters, demos and events from Day 1 of FinovateFall 2015.

04:32 pm

William mills, CEO of William Mills Agency and Stephen Ramirez, CEO of Beyond the Arc, discuss Finovate’s morning recap highlighting Blockstack.io and Yodlee.

08:43 am

Folks, be sure to go to www.williammills.com/blog/finovatefall-2015-live-blog-day-2 / for our live blog from today (Thursday). Thanks!

WM

04:11 pm

Trulioo

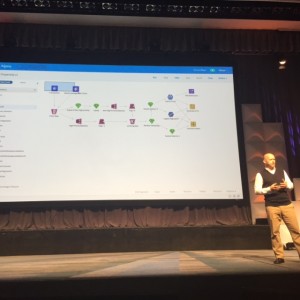

They can provide data on 4 billion people, in 40 countries. What, me worry? Trulioo, (pronounced “truly you”) sees themselves as the marketplace for consumer data, but they do not own any of the data. They don’t store any of the data, they just report on “match” versus “no match.” Know Your Customer (KYC) is one of the hottest topics in banks. This data would clearly make that verification process simpler. You can also see how it might be helpful for Anti-Money Laundering (AML) efforts as well. ^SR

@trulioo http://www.trulioo.com/

Trulioo’s GlobalGateway helps fintech companies with the electronic identity verification process by using its AML/KYC compliant ID verification and normalized API.

Starts off by comparing themselves to the likes of Uber because Trulioo owns no consumer data, they are just the marketplace facilitating. Never store any of the data. Able to verify 4 billion people today.

^K.T.

04:07 pm

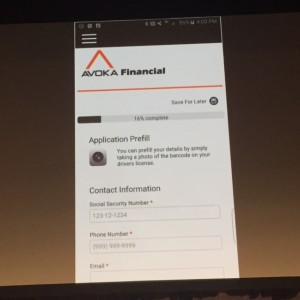

AVOKA

AVOKA

@avokatech http://www.avoka.com/

There has been a lot of discussion about customer experience at Finovate this year. Avoka emphasizes how their product can be used to simplify the delivery of digital products and services. They assist with cross-sell, as well as opportunities to improve customer support. ^SR

Avoka has created a digital sales enablement platform to create frictionless sales & service transactions.

Enabling better cross-selling for banks. Demo: User signs up for a checking account and fills out some demographic information that takes about 90 seconds. Basically, 3 product applications completed in 3 minutes including adding checking account, credit card and retirement.

^K.T.

03:59 pm

Auvenir

Auvenir

http://auvenir.com/

Auvenir utilizes advanced technology to transform how financial audits are performed, empowering auditors, enhancing quality/efficiency and raising the trust and confidence in our financial markets.

Multiple Boxes on stage represent the average amount of paperwork in a small company audit. Things need to change. Auvenir improves financial audit.

In system you can begin the audit and profile information in pre-populated. You can select different auditors if you do not already have an auditor. In the next section, connect accounting software to upload a lot of information and basic business information. You can manually edit the data as well. Software replaces snail mail with electronic confirmations with lawyer, accountant, etc. In this demo, the user can also drop in all their bank statements. You can also drag and drop in the legal contracts which pulls in all the required evidence by the auditor and extrapolating important data and highlight clauses and risks that it has identified from the contracts.

Platform looks pretty easy to use and would definitely make the audit process a lot easier.

^K.T.

Auvenir. Big data and machine learning comes to bank auditing. Wow. Even the bank’s audit team can benefit from innovation and technology. They have a smartwatch application, so some functions can be performed on the go. Bank’s can save weeks of time in preparing for and executing audits. This company is partnered with Deloitte. ^SR

03:51 pm

Dealflow.com

Dealflow.com

@dealflow http://www.dealflow.com/

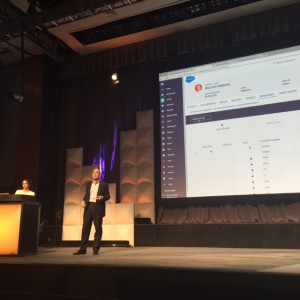

Deal Flow. The company provides online deal marketing, to address the changed ways that companies raise capital. This is targeted for institutional investors. Users can set their personal preferences. You can track and manage deals with a standardized workflow. They are now offering a “Facebook-style” wall, with updates and info on potential deals (or investors) of interest. ^SR

Dealflow.com develops software based on the collaborative collection of actively-marketed deal information. This offers insight into public and private financial deals including investment fund interests, real estate opportunities, mergers and acquisitions, and other types of deals being marketed on the Internet.

Dealflow.com demo. Calling out “Signal” concept in dashboard. This is how they personalize their experience. Involves the preferences the user gave when signed up and how they have used the platform.

Dealflow 2.0 with a new Dashboard that is visually appealing that shows companies and deals that would be of interest to the user.

^K.T.

03:44 pm

Fern Software

Fern Software

@fernsoftware http://www.fernsoftware.com/

Fern Software. Fern helps FIs engage with audiences that they wouldn’t typically reach. They work with FIs in 30 different countries. The product is a CRM-style platform with social networking. ^SR

Fern Software is a leading provider of banking software for inclusive financial institutions (microfinance institutions, credit unions, SME lenders and development banks).

Created BayTree, which is a financial, CRM aimed at Credit Advisors. Can use third party aps on top of their API. Organization with Events and tasks and social aspect with connections in a Facebook like feel. Some of the existing aps include DropBox, Twitter, Skype, Gmail, etc.

^K.T.

03:37 pm

HelloWallet

HelloWallet

@hellowallet http://www.hellowallet.com/

Hello Wallet. The company was acquired by Morningstar last year. Today, they are providing info on their financial wellness application. The focus is on retirement, with a focus on 4 key questions for planning. They are taking the emphasis off of the question, “when am I gonna die?” What would happen if… I changed the year when I retire? … I saved more? … Reduced expenses to make my money last longer? ^SR

HelloWallet partners with employers to provide independent, personalized financial guidance to employees through web and mobile-based software applications.

Financial Wellness Software now available to Banks. Suite of applications, score is at core of application. Wellness Score helps users improve those scores and improve financial wellness.

Financial Wellness ladder, helps users pay down debts and optimize benefits and save for retirement. Focusing in Retirement now, key feature is Retirement Explorer. This is tied into 4 key questions that lays out all the information in an easy to read graph. Then users can engage and change their retirement while in the back end takes into all complications and the user sees nothing. The user just sees their graph. They have partnered with banks and once the user clicks submit, the platform makes the changes for the user automatically in real life.

^K.T.

03:28 pm

EURONOVATE

@Euronovate http://www.euronovate.com/en/index.php

EuroNovate. What bank doesn’t want to go paperless? The only problem… it might take years and teams of IT and business leads. Euronovate helps FIs to make that transition to electronic document processing. 1.5 million customers are using their solutions in Europe. ^SR

Euronovate SA is an innovative company with an international vocation, based in Lugano (CH) and operating branch in Milan (IT) and Shanghai focused on native paperless and applying an unique end-to-end industrial model, with different partners covering all the phases of the paperless program.

Demo, New user registration for EnCreditCard – pulls up camera where user has to provide ID which automatically pulls photo and signature. Video pulls up and takes a live picture of the user, then the customer signs online. The solution compares the two authentication methods to verify.

From here, user can sign up for the credit card. While signing, video pulls up so they can be sure the contract is signed by a live person.

^K.T.

03:21 pm

Accept Email

Accept Email

@AcceptEmail http://www.acceptemail.com/us

AcceptEmail is the market leader for consumer remittances in Western Europe developing Smart Billing Solutions as SaaS from the perspective of the recipient.

AcceptEmail works with any email client. Ability to pay bills via email. Loads the status of the bill with all of the details for the user to be sure it is the correct bill. User can pay through a secure channel. Making life simple by paying all bills via email.

Baseball skit with inflatable balls fly into the audience. Went straight for my head! But all is okay.

Back to the software, shows reporting for bills opened/clicked/paid, etc. Customers pay 15% quicker with their solution.

^K.T.

AcceptEmail. Making it simpler for small companies to organize their AP function and pay vendor bills. Customer-centric bill payment platform that does not require the user to register for an account. Real-time reporting and tracking. Currently working with over 600 customers. ^SR

03:13 pm

DAVO Technologies

DAVO Technologies

@Davo_Tech http://www.davotechnologies.com/

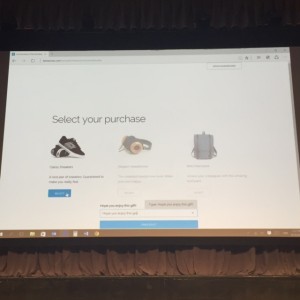

DAVO was created to solve the pain points in the payor/payee relationship; optimizing any recurring payment cycle, compressing time.

LOL, presenter admits he is a “recovering small merchant.” Davos works behind the scenes. They begin to demonstrate davos sales tax from merchant perspective.

Merchant finds data in marketplace, where they can click on an icon and fill out the information, which is mostly pre-populated. Once the merchant fills out the information, Davos can track sales and sales tax on a daily basis. The even send a daily email to the merchant for what they have debited their account for. Simplicity on front end, complexity on the back end.

^K.T.

Davo. This is a platform for managing and paying sales tax. Can someone take care of my sales tax, like ADP handles my payroll? Great question. Sales tax can be really complex for small and medium-sized businesses that do business in multiple jurisdictions. ^SR

03:06 pm

Alfa -Bank

Alfa -Bank

@alfabank_ru http://alfabank.com/

Alfa-Bank is a universal bank and is present in every key sector of the financial services industry, including corporate banking, retail banking, investment banking, trade finance, insurance and asset management

Their app is “Sense.” Behavioral analytics prioritize app for user such utility expenses, phone statements, fines, credit statements. All about the user. “Swiping” out non-relevant information is pretty good for user experience. App provides a Financial Messenger where friends can transfer money between each other. I use this type of stuff all the time. It is very useful.

Smart cross-sell system, design based UI.

^K.T.

Alfabank. This is an innovative bank that got it’s start in Russia. They have a full set of offerings that they now offer as separate products. ^SR

02:19 pm

CreditHQ @OrmsbyStreet https://ormsbystreet.com/

CreditHQ @OrmsbyStreet https://ormsbystreet.com/

CreditHQ provides financial insights to ensure your business is trading with the best customers & suppliers and get paid on time!

Very nice UI but I’m having trouble making sure I understand their offering; I’ll have to visit their stand. From their web site: Our aim is to help small businesses make big decisions through data and insight, and we’ve put together a team of product innovators and software engineers who have as their focus, the need to take sophisticated financial information and turn it into a next-generation digital tool to help businesses make good decisions about customers, suppliers and themselves. We believe that knowledge is power, so we look to provide businesses with the knowledge they need, in a language they understand, in order for them to make practical decisions within their business.

It sounds like they are strong in the EU but don’t yet have a large presence in the United States.

^William

Ormsbystreet. Their product is Credit HQ. They leverage data on small business to improve credit risk assessment. The industry is realizing that underwriting still relies on fairly antiquated methods for judging how risky a small business is. Many banks have moved slowly to expand small business lending. This means that very viable businesses do not have adequate access to capital. Credit HQ addresses some real needs in the financial services marketplace. ^SR

02:16 pm

MX @MXenabledhttp://www.mx.com/

MX (formerly MoneyDesktop) was scheduled to present but did not . I understand they are here and in the exhibithall; I don’t know why there won’t be a demo from MX today; they’ve won Best of Show many times so this is strange. Usually when a company doesn’t present they won’t be in the exhibit hall, I hope everything is ok.

^William

02:11 pm

Authy @Authy https://www.twilio.com/authy

Authy @Authy https://www.twilio.com/authy

Authy provides two-factor authentication to strenghten the login for websites, SaaS products, and mobile apps. Made easy for developers, businesses, and users.

“CoinBase, Knox Payments and other companies have been using our technology to present at Finovate in the past.” “Only 30-something percent of finch apps are using two-factor authentification which is 1/2 of usage on dating sites.” I actually didn’t realize the percentage was that high.

Showing the BitWay site to demonstrate the two factor authentification. Showing a PC screen for the transaction and an iPhone for authentication. I’m hoping they will show how it is used on a mobile device, not just a computer and a mobile device. Showing their app which enables a user to delete an authorized device which might have been lost. OK, I think I get it; the app uses unique data on the mobile phone or tablet to authentificate a device. Good job.

^William

Authy. 2-factor authentication to make transactions more secure. You sign up for a new account, then they text you a unique 1-time code to verify that it is you. But what if you lose your device? Authy helps you manage all of your devices. Deactivate the device, and it can’t receive that all-important push notification. ^SR

02:02 pm

Crowdability @Crowdability http://www.crowdability.com/

Crowdability @Crowdability http://www.crowdability.com/

Crowdability provides individual investors with education, information and insight into opportunities in the crowdfunding market. Our free website and email newsletter aggregate and organize deals from an ever-expanding universe of crowdfunding platforms.

Mathew and Wayne leading the presentation (Co-CEO’s). “Because of a change in the law everyone in the U.S. will be able to invest in high risk investments.” First stock screener for a private company. This is new, I’ve never seen a company like this, it makes sense. I’m assuming it will help consumers from investing in risky startups, or if they do, better know and understand the risks. They are now showing a screen that looks like Crunchable on steroids. Good job.

^William

Crowdfunding is growing in popularity, but yet there is little information to aid investors, particularly small investors. Crowdability provides research and information to level the playing field. Their platform also provides information on how major investors are investing in small start-up deals. ^SR

Here’s what industry analyst Jim Bruene notes on Twitter: “Interesting to see startups building tools for an industry (crowdfunding) that didn’t even exist 5 yrs ago eg @ Crowdability #finovate ”

01:54 pm

Alpine Data Labs @AlpineDataLabs http://alpinenow.com/

Alpine Data Labs @AlpineDataLabs http://alpinenow.com/

Alpine Data Labs embeds predictive analytics into every business function, enabling you to run your organization based on the insights that really matter .

San Francisco-based analytics company used by a wide variety of large organizations. Leveraging “big data”. “How do you get big data to EVERYONE in an organization?” Launching “Touchpoints” which enable business-people to ask questions/get data in a natural data language. Showing their data table. “Interact with vast quantities of data with very simple, graphic workflows.” Pretty cool to me. I’m interested in hearing what my friend Steven Ramirez thinks about it.

^William

Alpine Data Labs. They are a San Francisco-based big data firm. The new product is called Touchpoints, business apps that are tailored to specific use cases. They are trying to empower the business user, like the wealth advisor. The analytics engine has a visual interface to work with the data. The software can integrate with Salesforce, to make existing dashboards and reports more valuable. Beyond the Arc has a great deal of expertise in predictive analytics. I can say that I like what I see here. Very practical application of predictive analytics to wealth management. ^SR

01:48 pm

Capriza @capriza http://www.capriza.com/

Capriza @capriza http://www.capriza.com/

Capriza’s award-winning, end-to-end enterprise mobility platform enables IT and lines of business to mobile-enable critical business workflows in a matter of days without the need to access source code, APIs, or integration.

“We help modernize your business. We take your workflows and simplify them and enable use to use your work flow on any device any time.” Getting ready to show how an Oracle app might be enhanced with Capriza. In SOME ways it reminds me a little of the Adobe presentation: using new API and platforms to enable FI’s to offer all their business processes while continuing to use their existing technology infrastructures.

^William

Capriza. We all work in environments with complicated business processes. What if you could simply that workflow, and scale it across your entire department, or perhaps the whole company? ^SR

01:41 pm

BehaviorSec @BehavioSec http://www.behaviosec.com/

BehavioSec offers Behavioral biometric solutions to create a multi layered approach for authentication & verification purposes.

We monitor how you type on a computer to determine a “digital fingerprint” and hope to have 20 million users this year. I saw a presentation on this approach to authentication last year and it’s really cutting edge. I’m assuming these folks can measure someone’s “gait”, how they walk, hold their phone, type on their computer to authentify that I’m who I say I am. Now showing what the user is doing in real time with confidence scores which I THINK is how they make it work. This is really cool stuff. I can think about all kinds of use cases. For now, you could confirm that someone who is using a username and password is the real person based on how they use a computer/phone/tablet. Later, or even now there may not be a need for passwords based on this technology. Very cool.

^William

BehavioSec. This is one of the first companies today discussing biometrics at Finovate. Very interesting, compared to the number of presenters last year. It is generally acknowledged that passwords are a poor way to protect accounts. Now, we can tell who is behind the computer. They did not go deep into their technology, so interested in seeing what is under the hood. One thing that is nice is that their technology is provided as an API, to fuel various security offerings. ^SR

01:33 pm

Advisor Software

Advisor Software

@AdvisorSoftwarehttp://advisorsoftware.com/

Advisor Software, Inc (ASI) provides cloud platforms to empower today’s advisor and wealth management companies.

Custom software for the largest FI’s for wealth management. Talking today about a new product launch, their API for wealth management – from financial planning, analysis and much more. “I want to show you two apps we built on top of our platforms.” First is a SALESFORCE app; portfolio rebalancing engine.

Up until the last few years Salesforce really didn’t have a good base of FI business EXCEPT for in wealth management and perhaps private banking. Now there are more and more great Salesforce application companies (including the very successful WMA client nCino) that are making gigantic changes in how FI’s operate.

Now showing a white label platform called “digital advisor” – rules based, risk-based or other. Looking like a PFM/wealth management dashboard; it looks clean and easy to use with good data.

^William

They provide APIs for robo-advisor services. For the demo, they’ve presented apps that they have created based on those APIs. They’ve been selected by Salesforce to provide investment management functionality for Salesforce’s new financial cloud. (Dreamforce is taking place this week in San Francisco. Be sure to search for financial services news coming out from that event as well.) Very nice UI for managing a client portfolio. This can be a goals-based robo-advisor system. As an investor, you can see progress toward your goals, and also adjust sliders to create what-if scenarios. ^SR

01:26 pm

WALLETRON http://www.walletron.com/

Walletron’s moBills mobile wallet, data integration and push notifications help any biller deal with today’s underwhelming mobile bill presentment and payment options.

Founder Walletron is speaking. He’s making a great point about having to need to have in hand, paper bills even when you want to do electronic bill pay or mobile bill pay. “Today, launching moBILLS” Changing company name to Wallet after Apple’s new IOS update later this month. He’s showing a PDF of a bill in Apple’s Passbook (I think) or IOS Safari. He said they are going to have an Android Pay version native to the device. Now showing the ability to add a bill to Apple’s Passbook in order to integrate the bills and the payments, paid when the consumer wants to pay the bill. This is really cool. I’ve done a ton of work in remittance processing/lockbox and this looks like the next logical step to the integration of off-line billing to mobile payments.

This is new, I don’t recall seeing anyone else doing anything like this. I like it. Great job.

^William

Walletron. Pay offline bills with ease, online, using your mobile phone. Account notifications are integrated into a mobile wallet. ^SR

01:18 pm

Adobe @Adobe http://www.adobe.com/

Adobe @Adobe http://www.adobe.com/

Adobe is the global leader in digital marketing and digital media solutions. Our tools and services allow our customers to create groundbreaking digital content, deploy it across media and devices, measure and optimize it over time and achieve greater business success.

It’s pretty cool to see Adobe here at FinovateFall. Everyone uses Adobe products every day (whether they know it or not) and it’s great that they have made a serious effort to offer specific products for the financial industry. Showing and example on a Chrome web browser with a lot of cool data that FI’s can use via the Adobe Marketing Cloud. Good job.

^William

Adobe. Adobe has a great suite of applications for managing marketing and digital customer experience. Great to see them at Finovate. They are looking at how to build deeper customer engagement for digital banking products and services. They’ve applied their technology for the connected customer experience. Great UI and visuals. Demo didn’t cover much of the technology. ^SR

01:01 pm

Folks, it’s almost show time again here at Finovate Fall 2015 in New York. Please email me at william@williammills.com if I may provide additional information or be of service in any way.

@williamemills

12:04 pm

Folks, it’s time for a lunch break which means Steven, KT and I will be working on some video now. See you back at 1:00pm EST. Thanks!

William Mills, CEO

William Mills Agency

12:02 pm

ebanKit

@e_bank_it http://www.ebankit.com/en

ebankit offers you the most innovative multichannel banking products: internet banking, tv banking, mobile banking, branch front office, facebook banking, account manager, contact center, kiosks, google glass banking.

Banks must be Omnichannel and be able to see what the customer is doing on all of their channels. Consumer wants to be able to choose what channel depending on location and preference. Ebankit provides that tech and is showing social, product subscription, etc.

Mobile Solution – social – transact with friends – can pay a friend via the app based on phone contacts, Facebook, etc.

Augmented reality- Wow. That is cool. Will need to check that out later.

Beacons- Example, bank has placed beacons near branches, if customer walks by, then their phone will let you know about interesting offers.

Account Opening online – All docs generated digitally, with signing easily.

Smart Watch Demo – App on watch where user can check balance and payments.

Voice enabled as well.

^K.T.

11:55 am

Soundpays

@soundpays http://www.soundpays.com/

Soundpays‘ universal mobile wallet enables users to pay online, in-store and on TV with a single app that uses sound waves to initiate a transaction.

Uni-directional payment solution. POS for small business example.

They destroy their network and rebuilds every 30 seconds to protect security.

Example: YouTube video- client had a video. Soundpays uploaded video to their servers and Soundpays adds watermark. Client didn’t know how to monetize video. Well, Soundpays put call to action on right hand side that allows the visitor to buy from youtube video with a click. So user can purchase on phone easily.

White-label solution. Looks like the tech can be applied in a number of ways. Work in video, TV, any phone, any smart devise.

^K.T.

Soundpays. They have a point of sale system for small businesses, using their soundwave technology. Very cool ways to include audio and sound recognition into a number of different products and use cases. You just need an internet connection, speaker, and microphone. One application is adding audio to mobile wallets. ^SR

11:48 am

Buzz Points

@BuzzPoints http://www.buzzpoints.com/

Buzz Points is an innovative rewards program that rewards consumers for choosing local businesses over national chains, and for banking with a local community bank or credit union. The localized rewards program is a win-win-win for customers, community financial institutions and locally owned businesses.

Partners with FIs to increase transactions, expand loyalty across card holder base. Locally focused rewards program. Which means users will earn 2x time points at local shops as opposed to national brands. Aimed at millennials’ who want to keep money at local coffee shops and pizza places. Yes, that is true. I can testify to that as a millennial.

Instant rewards sent to device. Partners can put targeted offers that users can use such as coupons.

App looks at category preferences and types of merchant the user typically uses and pushes those shops up to the top of the user feeds.

Automate concept of loyalty card. Makes loyalty hands free.

7 different styles of directories. Sorted by closeness and how many times more points you will get by visiting that shop.

Broken rewards directory into 3 different sections. Local, National and Charity.

^K.T.

buzz Points A locally-focused card-linked rewards program. Consumers earn more points with local merchants, versus big national retailers. Rewards are presented as Local, National, and Charity options to redeem points. The aim is to keep the financial activity in the local community. Buzz Points also uses the data to help FIs drive incremental card acquisition. ^SR

11:40 am

Urban FT

http://www.urbanft.com/

Urban FT’s white-label, digital banking solution helps smaller and regional banks and credit unions to compete with larger FIs by enabling them to create, customize, and edit digital solutions for each card program via its Platform Management Portal.

Reengineered banking experience, white label banking solution. Brings together financial tools, social and discovery. App enables social connect.

3 main sections of app: Money, Discovery, and Social section

Money Section: access any financial info across the platform. First thing you see is account aggregation and view account balance across all accounts.

Current banking experience is fragmented and wants it to be holistic. By clicking on the transaction, you can see the venue and sort of like a “yelp” page for that venue such as a restaurant with reviews and pictures.

Extra features: Spending alerts, cash position, top merchants, etc.

Social Feature: “feed” for other users as well as capability for partner to advertise on feed.

Admin Portal: Example: New Partners -Sprint.

Partner can customize branding, etc.

^K.T.

Urban FT. A product that enables consumers to manage card accounts, with lifestyle features added on top. There is also an aspect of personal financial management (PFM) tools as well. Urban FT announced a new partnership with Sprint. ^SR

11:33 am

Id Analytics

@ID_Analytics http://www.idanalytics.com/

ID Analytics is a leader in consumer risk management with patented analytics, proven expertise and real-time behavioral insight. By combining proprietary data from the ID Network®with advanced science, ID Analytics provides in-depth visibility into identity risk and creditworthiness.

Name and last 4 digits of SS – all the information that ID Connect needs to authenticate user with Financial Institution.

No need for long authentication forms. “Yay” says the consumer!

On Mobile, conversion rates are so low since they have to put in so much information. That is no surprise. ID Connect helps increase conversion rate on Mobile.

Back End- pulls all info from their network on user and then provides a comprehensive risk assessment on Tim. Also checks Iphone that user used to verify and assess.

Looks pretty good from a customer experience perspective.

^K.T.

Id Analytics. Wants to make it easy to transact, in a secure way. By identifying the customer behind the scenes, customers don’t need to enter much information to obtain a new account on a mobile device. For example, all a customer may need is Name and Last 4 of social security number. The backend database enables them to match and ID millions of customers. They also conduct a behind the scenes risk assessment to identify fraudsters. This can be tailored for the look and feel of any financial institution. “Take the pain out of the new account open process.” ^SR

11:27 am

TRADEIT

@TradeItStock https://www.trade.it/

Trade IT allows customers to trade quickly and securely from any partner site or app, with the broker of your choice.

TradeIt – 12 apps integrating it including StockTracker. Example: Stocktracker can link all your accounts and make trades. Showing how easy it is to buy, fingerprint identification for security, and place order for NFLX.

Broker Exchange – Distributed brokers exchange that they can set on any network. Little designed so it is easily integrated. Inputting ID picture for info and SS Number. Sign into all your accounts such as Bank of America Account which you can use to fund the account.

^K.T.

TradeIt. They help financial institutions to offer brokerage services, in a simple-to-implement manner. ^SR

11:20 am

Blockstack.io

Blockstack.io

@blockstackio http://blockstack.io/

Blockstack is a licensed enterprise software stack for financial services to create blockchain 2.0 applications quickly and easily.

Provides Infrastructure to build applications quickly and easily on blockchains, also private hosted development platforms.

Demo: Web app built on private Blockchain. Account Dashboard with balance info and transaction history and way to send assets.

Example. Send corporate notes. Sending asset and move from one account to another. Account balances updated instantly.. Keeps info in sync between multiple parties.

Personal Examples: Salary paid twice a month. Why not paid more often or daily? Reason because technology is not advanced enough – until today. Which is what they are offering.

^K.T.

Blockstack.io “Blockchain as a service.” Blockchain — what is it, and what is it good for? As you may know, a blockchain is the backbone for currencies like bitcoin. But, the blockchain is what helps people verify who they are, and helps parties to track their assets. Parties can share information, without an intermediary (they don’t need escrow or a trust company). Secure information, secure transactions. With a provider like Blockstack.io, you can create your own private blockchain. Take note, you’ll be hearing much more about this technology in financial services. Here’s some background blockchain information. ^SR

11:12 am

Additiv @_additiv_ http://www.additiv.ch/

Additiv @_additiv_ http://www.additiv.ch/

Additiv develops and implements digital innovations and business models for financial services – tailored and turnkey.

“Digitization gives us the opportunity to create and innovate”

Demo Screen in German.

Following Risk Profile

User can go into portfolio and change, individualize and optimize, such as adding 5% Gold and Oil.

Then platform compares existing portfolio and new one visually.

^K.T.

Additiv. This is a robo-advisor platform, based in Europe. We’re seeing a lot of strong technology to build, manage, and optimize investment portfolios. This is starting to become a crowded field. While robo-advising represents the future of investment management, how do these companies differentiate? Additiv has a full set of functionality, you can check the box there. But, not seeing much in terms of user interface or client experience. ^SR

11:05 am

CELLTRUST

CELLTRUST

@CellTrust http://www.celltrust.com/

CellTrust SecureLine™ Mobile Collaboration Suite offers traceable and secure SMS/messaging, voice and a mobile business number for mobile collaborative workflows.

CellTrust provides a separate mobile voice number on the celltrust app that allows for secure internal and ability to talk outside your network.

Skit- Broker and Customer.

IOS devise – split screen for personal and work. From the work side, can send a text message that is sent via celltrust server so it is secure. Response is sent back to original person’s app.

Ability for calls to come into celltrust app.

Back End Server archives everything. Including an email journal report sent at the end of the business day. Can also track the emails in CRM.

^K.T.

CellTrust. The company provides secure messaging, and the infrastructure to manage messaging within full compliance requirements. There’s a back-end server that enables review and reporting. On Twitter, Ben Brown notes that, “CellTrust provides a secure gateway for SMS and voice @ FirstAnnapolis .” ^SR

10:58 am

TransferTo

TransferTo

@TransferTo https://www.transfer-to.com/

TransferTo’s Mobile Money Hub offers money transfer operators a solution that enables developing markets to send money remittances via mobile.

“Over the 2 and half billion people worldwide do not have access to financial services.” To help, there is Mobile Money. Estimating, one billion Mobile Money users by 2020. This is opportunity for Financial Intuitions and their challenge is to connect to that. TransferTo connects FIs to mobile money markets worldwide.

Demo-Phone call. Interesting skit, where caller needs 0 for an emergency. So one person logs in into MoneyTrans to send to mobile phone number in “kenya.”

^K.T.

TransferTo. Half of the world’s population is unbanked. Mobile money is one way to address this issue. How do banks tap into this opportunity? Transfer money using mobile carriers, you send to the recipient’s mobile phone. You can send money in real-time to people around the world. TransferTo is linked into hundreds of carriers across the world. While the focus is on international, I see no reason why this wouldn’t work in the U.S. ^SR

10:50 am

Getting started for the next group of 10…

10:12 am

Time for a short break. See you in 30 minutes…. ^William

10:11 am

Jack Henry & Associates @JackHenryAssoc http://www.jackhenry.com/

Jack Henry & Associates @JackHenryAssoc http://www.jackhenry.com/

JHA provides more than 300 products and services that enable our customers to process financial transactions, automate their businesses, and succeed in an increasingly competitive marketplace.

Full disclosure: Jack Henry & Associates is a WMA client.

I’ve known Wade Arnold for years; he’s a REALLY smart guy. “We are announcing the Banno platform: exception technology, beautiful and designed to serve your FI’s customers.” Showing a FI web site that utilizes the new Banno platform to re-engineer the customer experience. “Showing tablet-based customer experience. “Search today is different – it has to be more like Google or Twitter – the user experience needs to keep up with what users are accustomed to.” “Beautiful experience on both Android or IOS.

“Do the right thing, do whatever it takes, have fun!” on their T-Shirts. I have to agree with that. Showing how the new Banno platform can be utilized without totally changing an existing FI’s infrastructure. Showing how it looks on a browser. Very cool.

^William

^William

This is the introduction of Banno, as an integrated offering under the Jack Henry banner after the recent acquisition . They are discussing “an account as a service”. This gives a bank the opportunity to enter a new market quickly and seamlessly.

^SR

10:03 am

IDmission @IDmissionLLC http://www.idmission.com/

IDmission @IDmissionLLC http://www.idmission.com/

IDmission offers all the tools necessary for banks to enable their correspondent banking channels serve local populations by offering them access to traditional and new financial services products – for example Account Opening, Loans, Microfinance, Group Loans, Insurance, Prepaid cards.

Now showing a tablet-based app with a fingerprint scanner to what looks like a receipt printer. Now showing on a PC that the fingerprint has been scanned, now scanning ID card from tablet, data is validated. From their web site: THE WORLD’S BEST CLOUD for CUSTOMER ENGAGEMENT. Use INFORM to Leapfrog the Market in 3 dimensions. KYC – On-boarding – Payments

I think it’s a pretty good solution but might be a bit complex for the demo in 7 minutes.

^William

From a customer perspective, the onboarding process can be long and sometimes painful. ID Mission wants to streamline onboarding with their solutions for Financial Institutions.

You can follow Beyond the Arc on Twitter at @beyondthearc or on Google+

They’ve taken a very complicated paper-based enrollment process and made it digital. Even if the process is complex, it is still great that it can be implemented digitally. ^SR

09:56 am

GRO Solutions @grobanking http://www.grobanking.com/

GRO Solutions @grobanking http://www.grobanking.com/

Gro Solutions exists to enhance the customer acquisition process for banks and credit unions. Our goal is to increase the number of customers.

Full disclosure: GRO Solutions is a WMA client.

David Eads, CEO: “We are here to show you how easy it is to sign up new clients – anywhere. We are focused are making it easy to sign up new customers for banks and FI’s.” Showing IOS mobile app. “New account openings in less than 4 minutes.” It can tell whether the phone is from Verizon or other carrier and pre-populates the data. This will save a TON of time and effort. Frictionless is key and now showing validation (patent pending) and disclosures. Now showing funding from mobile app using camera with a credit card. “We want profitable, engaged customers that make the FI the customer’s primary financial institution.” “It’s that easy. Our customers are growing faster and more profitable and engaged.”

Very slick. Congrats!

^William

“Mobile customers are your future”, and now they are easy to sign them up. They are focused on customer acquisition using mobile. They have an image capture technology, smoothly integrated into mobile apps. ^SR

09:50 am

Xignite @xignite http://www.xignite.com/

Xignite @xignite http://www.xignite.com/

Xignite’s cloud-based market data APIs help financial services, media, software and corporate developers simplify the complexity of sourcing and integrating market data.

“Easiest, largest suite of FI data API’s” The leading finch companies use us, Yodlee, and more.” Showing “cloud streaming” which enables API’s in minutes w/o infrastructure. “We have the biggest bad ass data streaming.”

Showing a wire frame Android simulator – it’s starting to look REALLY complicated but I’m sure there are plenty of folks here that have a better grasp of Android coding than me. Speaking to a new initiative with a “ Che ” Guevara logo with a group of 16 other other Finch companies.

I’m a little uncomfortable with “Che” Guevara being a part of their image.

^William

With a cloud-based solution, they provide data streaming and API infrastructure. The company is an enabler of fintech APIs.

^SR

09:42 am

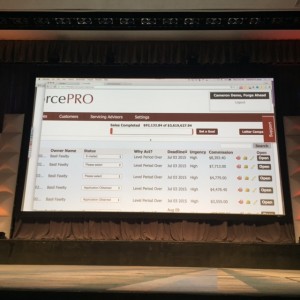

InforcePRO @InforcePro http://inforcepro.com/

InforcePRO @InforcePro http://inforcepro.com/

InforcePRO™ is a web-based software platform backed by private equity and engaged by over 1,000 agencies in Canada and the United States.

Founders of InforcePRO on the stage. “Most life insurance policies have not been evaluated on a regular basis.” .6 trillion in life insurance globally. We help your bank help your clients with their life insurance needs while creating new revenue for your FI. Showing a PDF of a report of death benefits and a funding review. Showing four life insurance carrier quotes for a particular client.

This reminds me, I need to review MY life insurance coverage. I think I’m good but they have a good point; most folks don’t think about it as often as they should.

^William

The company provides a platform for managing insurance products. This looks like a robo-advisor for personal lines of insurance. It provides personal advice for insurance. It helps banks to manage the compliance and risk considerations of offering insurance.

^SR

09:35 am

yseop @yseopai www.yseop.com

yseop @yseopai www.yseop.com

Pronounced “Easy Op” From their web site: Yseop is an enterprise software company that provides an Artificial Intelligence platform which allows customers to develop AI applications autonomously.Yseop’s software automates reasoning, intelligent dialoging, and writing through two product lines: Yseop Smart BI and Yseop Smart Machine. Both products boost revenue, reduce costs, and increase productivity. Yseop is a global leader trusted by companies across the Fortune Global 500.

Now showing how it is used from getting data from an Excel spreadsheet. I’m sure this is a powerful platform but I’m having a hard time grasping their USP – what makes them different or better than existing products and services.

^William

The company name is pronounced “Easy Op.” They help companies make the most from their data by moving past the traditional dashboard. This is a self-service business intelligence tool. The software helps to generate narrative text descriptions of the data.

^SR

09:27 am

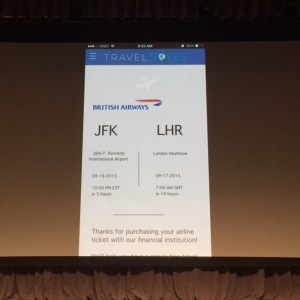

Travel Notes @TravelNotenow http://www.travelnotenow.com/

Travel Notes @TravelNotenow http://www.travelnotenow.com/

TravelNotes is a service that seamlessly coordinates your travel plans with your bank so that your credit or debit card does not get declined.

Founder is showing a private label bank IOS mobile app now where the user might be flying JFK to London. THIS functionality shows the user that they are available for credit for a delayed flight. The BIG deal, for me, is that using this your bank knows you are traveling.

This is a BIG problem for me and probably millions of other folks in the U.S. Every time I travel domestically I get calls from my bank asking me if I’m really where I am. I can be in Cullman, Alabama buying in gasoline and an hour later I get a call from my bank. This is crazy. Think how much it costs the bank to call me, for me to call back and more just to confirm a simple charge one state next to Georgia.

^William

The technology makes it easier for customers to update their bank about their travel schedule. The product also provides a more complete set of travel-related services, like getting airline compensation for a seriously delayed flight. ^SR

09:18 am

NORTH SIDE http://northsideinc.com/ North Side offers a more natural, fun, and efficient natural language interface that enables banks to know their customers better and sell them credit, investment and cash management services.

NORTH SIDE http://northsideinc.com/ North Side offers a more natural, fun, and efficient natural language interface that enables banks to know their customers better and sell them credit, investment and cash management services.

Canadian-based company that creates apps that help computers better understand English language and empowers self-service. “Empowered Self-Service”. Man, I hope this works, I am so tired of getting IVR’s that don’t understand what callers are saying. They are having some tech issues but I think it’s going to work. Their IVR voice sounds is interesting. Still some tech issues but perhaps I can stop by their stand and check it out later.

I’ve been testing/using speech recognition technology for more than a decade – from PC’s to Mac’s to iPhones using all kinds of applications/speech engines. I don’t think as a whole the industry is where it needs to be, yet, but will be soon.

^William

North Side. Would you like to talk to your computer? North Side believes that you do. It will make customers more comfortable. Hal, when is my credit card payment due? A Siri-like assistant provides customers with account information. ^SR

09:11 am

Empyr http://www.empyr.com/#onlinetooffline

Empyr http://www.empyr.com/#onlinetooffline

Empyr empowers companies to track and monetize online to offline commerce

“Average number of users will spend 11 hours on the Internet today.” Man that’s a LOT but I believe it.

“We are building an off-line to on-line advertising platform.” Showing a living social example via web browser with an offer linked to a credit/debit card and activation. Shared $ model. Now getting ready to show San Diego County Credit Union’s home page which is working with Empyr. Consumers (CU members here) can get cash back by using their FI’s cards. 20% adoption by members at SDCU. Now showing a points-based program.

I think this is an interesting concept but I need to learn how it is different than so many other organizations that are integrating offers, rewards, mobile wallets and so much more.

^William

How do you connect online and offline commerce? They provide an online to offline ad platform. This is a straightforward way to implement card-linked offers for banks. They have a cash-back rewards offering. ^SR

09:05 am

Flybits @FlybitsInc http://www.flybits.com/

Flybits @FlybitsInc http://www.flybits.com/

Flybits enables the creation of highly-personalized mobile experiences that go beyond what is practical with traditional app development platforms and simple location-based services.

“Using Flybits you can customize the customer experience.” They are showing a web-based SaaS tool to help FI’s customize the mobile user experience based on context; location, historical, weather and more. When I populate our zones in the app the customer will see the appropriate UI that is relevant to the bank customer.” Showing example of mobile bank app being used at JFK Airport and how the app changes to the context.

I think this is pretty slick. There is SO MUCH that can be done with data with mobile apps for a better user experience for the customer. I guess the main thing I got out of their demo is that “one size doesn’t fit all” so your bank’s customer experience should create the most value to each customer.

^William

Context is king, and Flybits helps banks leverage it for their mobile apps. You can understand your user better, and adapt the mobile app on the fly. Oh, I guess that’s where the name comes from? This provides the opportunity to personalize the services that you deliver to users. Their Studio platform allows you to create customized “moments” that are relevant to the user. ^SR

08:55 am

It’s showtime! Here we go… ^WM

Twice a year technologists, bankers, regulators, press, innovation gurus, and more gather for what has been described as the “Disneyland of Fintech.” The Finovate Group convenes what has become the signature event addressing financial technology and innovation, Finovate. Think of it as technology speed dating. Over 40 companies will take to the stage to demonstrate their latest offering. No powerpoint allowed– just live demos, and all in rapid-fire progression. Each company gets 7 minutes to show us what they’ve got. From a Beyond the Arc perspective, we’re interested in the impact that this technology has on customers. While the technology is cool, what difference does it make on the customer experience? Over the next two days we’ll be live blogging and will cover the conference from gavel-to-gavel. ^SR

Twice a year technologists, bankers, regulators, press, innovation gurus, and more gather for what has been described as the “Disneyland of Fintech.” The Finovate Group convenes what has become the signature event addressing financial technology and innovation, Finovate. Think of it as technology speed dating. Over 40 companies will take to the stage to demonstrate their latest offering. No powerpoint allowed– just live demos, and all in rapid-fire progression. Each company gets 7 minutes to show us what they’ve got. From a Beyond the Arc perspective, we’re interested in the impact that this technology has on customers. While the technology is cool, what difference does it make on the customer experience? Over the next two days we’ll be live blogging and will cover the conference from gavel-to-gavel. ^SR

08:27 am

Folks, it’s almost show time here at Finovate Fall 2015 in New York. It looks to be another terrific event. @williamemills

08:24 am

Getting ready for FinovateFall 2015 to begin! This is the largest Finovate ever, with more than 1,500 attendees. We are looking forward to a great show.

Getting ready for FinovateFall 2015 to begin! This is the largest Finovate ever, with more than 1,500 attendees. We are looking forward to a great show.

^K.T.